/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

Brokerage D.A. Davidson has now traveled the gamut of emotions a broker could go through for a stock with the neocloud company, CoreWeave (CRWV). Analysts led by Gil Luria, in a note to clients, acknowledged as such, stating, “As a firm, Davidson has been to both extremes on CRWV, and we see this as a good time to be balanced. On one hand we are optimistic regarding the outlook for the category of providing compute and believe CoreWeave has made itself a key participant. On the other hand, we remain skeptical of CoreWeave’s ability to generate sufficient returns given its margin profile and high dependence on debt financing. We would also like to see less insider selling.”

Essentially, Luria and his team have landed where they started. The firm had initiated coverage on the stock with a"Neutral" rating and had downgraded it to “Underperform” in May 2025. Earlier this year, Luria and his team again assigned the rating of “Neutral” to CRWV stock, citing the $100 billion fundraising deal with OpenAI. Finally, a strong showing in Q4 and AI deals with players like Anthropic convinced the team to upgrade the stock to a “Buy.”

About CoreWeave

Founded in 2017, CoreWeave is an AI-native cloud provider built primarily around Nvidia Corporation (NVDA) GPUs and AI workloads. It provides GPU cloud infrastructure, AI compute services, and AI training and inference infrastructure. Unlike traditional cloud giants, CoreWeave was built specifically for AI compute and high-performance GPU workloads.

Valued at a market cap of $44.67 billion, CRWV stock is up 41.43% year-to-date (YTD).

So, is there substance behind the continuous flip-flops of D.A. Davidson for CoreWeave? Let's analyze.

Still Unprofitable

Since its listing in March 2025, shares of CoreWeave are up about 150%, quite the jump in just over a year. However, most of that is due to the promise of future growth, rather than what it offers on the table currently and especially, in terms of financials, as it continues to remain unprofitable.

The company had a mixed Q1, with earnings missing, but revenues surpassing estimates. For Q1 2026, CoreWeave reported revenues of $2.1 billion, up a healthy 111.6% from the previous year. However, the loss per share for the quarter stood at $1.40, narrower than $1.49 per share YOY, yet the operating loss margins doubled to 7% from 3% in the same period. Traditionally, that's not a good sign, as it means that the company is spending more to increase its revenues. Moreover, the loss was higher than the consensus estimate of a loss of $1.20 per share.

However, in a positive development, net cash from operating activities jumped to about $3 billion from a mere $61 million in the prior year. A decrease in accounts receivable of about a billion dollars helped here as the company collected cash from customers compared to not doing the same in the previous year. Overall, the company closed the quarter with a cash balance of $2.2 billion, too low compared to the short-term debt levels of $8.1 billion.

In terms of valuation, CRWV's signaling is mixed. Its forward price-to-sales of 4.30 times is above the sector median of 3.29 times, while its forward price-to-cash-flow of 6.06 times is below the sector median of 18.53 times.

CoreWeave Conundrum

Depends on who you ask, CoreWeave offers different value propositions. While some earmark it crudely as just a hoarder of Nvidia chips, others deem it to be a crucial player in the ongoing AI infrastructure capacity-building space.

The truth? Somewhere in between.

Yes, the company is closely linked with Nvidia. In fact, an AI deal between Alphabet (GOOG) (GOOGL) and asset manager Blackstone (BX) led to a sharp decline in CRWV shares in Tuesday's trading session. And yes, Nvidia owns about 11% of the company, but CoreWeave has undoubtedly more to offer.

Notably, the scale of CoreWeave's physical infrastructure commands attention on its own terms. A fleet of roughly 250,000 GPUs spread across 43 data centers makes it one of the largest non-hyperscaler GPU operators anywhere in the world. But the more consequential story begins at the hardware layer, where the company's approach diverges sharply from what others in the space have built. CoreWeave optimizes its architecture from the ground up, starting at the physical rack level using Nvidia NVLink 72 configurations, extending through the fabric via InfiniBand interconnects, and running all the way down to the orchestration layer. The net effect is that an entire cluster behaves as a single unified computing surface rather than a loose collection of individual machines.

For frontier model training, this is crucial. The limiting factor in those workloads is rarely raw GPU throughput in isolation. It is how efficiently computation can be distributed across thousands of chips working in concert. CoreWeave's architecture addresses that constraint directly. Where competing neoclouds present customers with an uncomfortable choice between the performance ceiling of virtual machines or the operational chaos of bare metal deployments, CoreWeave threads that needle through direct processing unit integration, delivering bare metal-level throughput within a managed cloud environment. The practical outcome is a lower effective cost per token for inference workloads, which is ultimately the metric that matters most to the customers running them.

Encouragingly, the commercial traction this has produced is reflected in a backlog that has grown to nearly $100 billion. Within that figure, the financial services segment alone is approaching $10 billion, driven by demand from quantitative trading firms including Jane Street and Hudson River Trading. Spatial computing and physical AI workloads have crossed the $1 billion backlog threshold as well, while robotics, autonomous systems, and scientific modeling have each matured into material sources of demand in their own right.

Moreover, a pleasant surprise has been the demand for older-generation hardware. Across CoreWeave's entire fleet of A100, H100, H200, and L40 GPUs, pricing actually moved higher during Q1, and the company's capacity across that installed base remains essentially fully committed. In an environment where concerns about oversupply of earlier-generation chips have circulated widely, that data point carries real significance.

Finally, the software layer is developing into an increasingly important part of the CoreWeave story as well. Already, 80% of the company's largest customers have adopted its storage solutions. Its cluster management platform, known as Slurm on Kubernetes or SUNK, has gained enough external credibility to be licensed by other operators.

Beyond that, CoreWeave offers two additional software products that speak to how deeply embedded it is becoming in the AI infrastructure stack. W&B Models functions as a dashboard and control system for monitoring and managing the training of AI models, while Mission Control serves as the operational nerve center for data center management. Notably, Nvidia itself has agreed to test Mission Control, a validation that carries meaningful weight given the company's central position across the entire AI compute ecosystem.

Analysts' Opinions

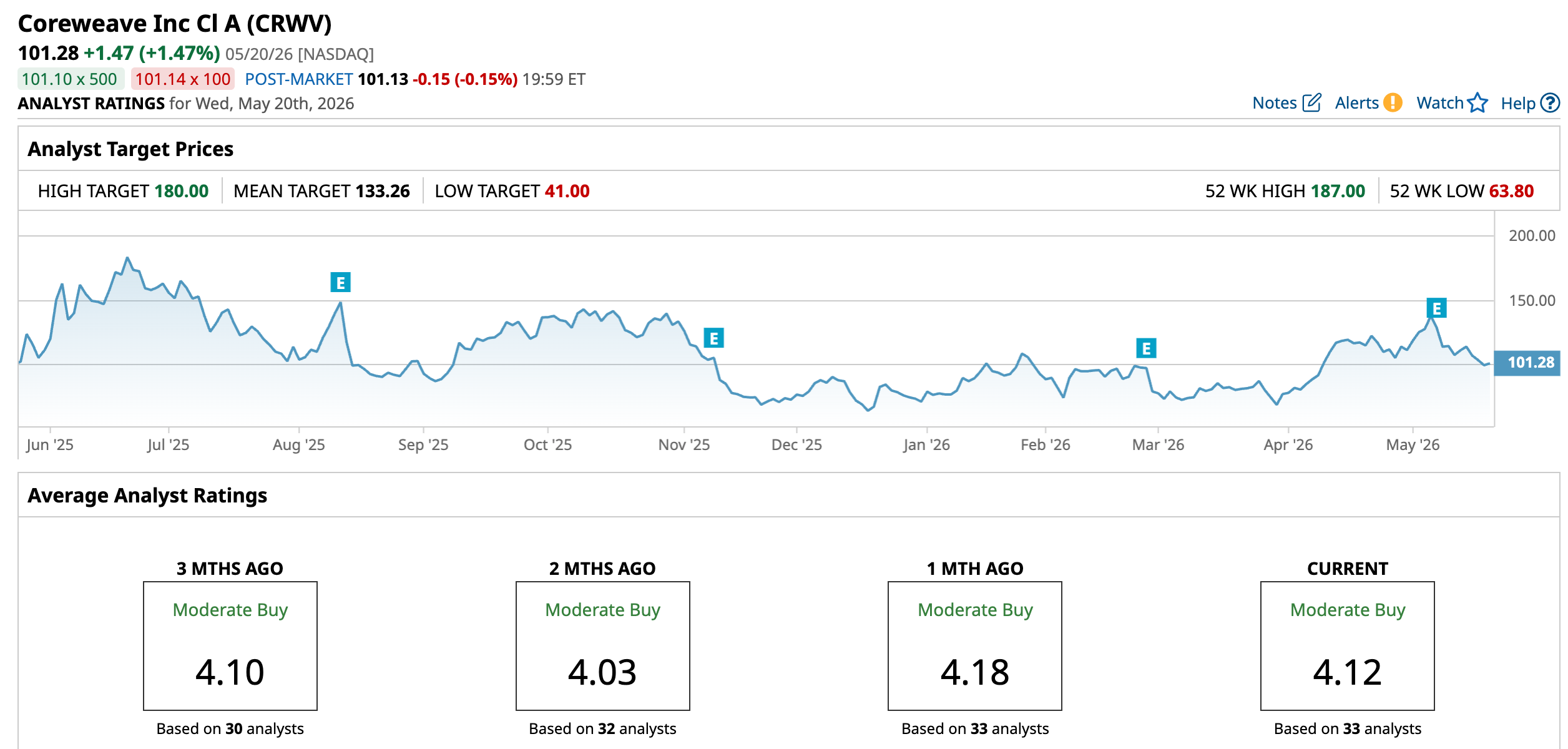

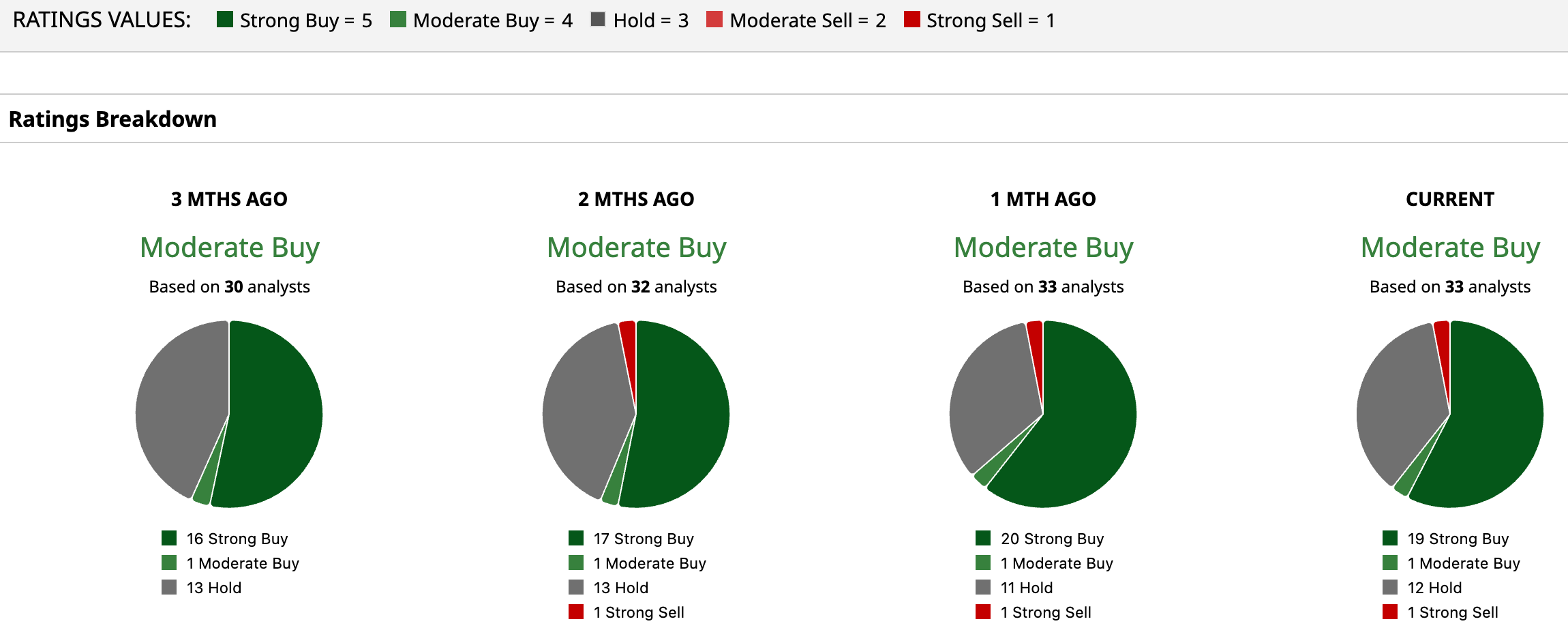

Considering all this, analysts have assigned an overall rating of “Moderate Buy” for CRWV stock. The mean target price of $133.26 denotes an upside potential of 31.58% from current levels. Out of 33 analysts covering the stock, 19 have a “Strong Buy” rating, one has a “Moderate Buy," 12 have a “Hold," and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)