/Teledyne%20Technologies%20Inc%20logo%20on%20website-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Valued at a market cap of $29.1 billion, Teledyne Technologies Incorporated (TDY) is a diversified industrial technology company that provides advanced instrumentation, digital imaging products, aerospace and defense electronics, and engineered systems for highly specialized markets. Headquartered in Thousand Oaks, California, the company serves customers across industries including aerospace, defense, marine, industrial automation, energy, environmental monitoring, and life sciences.

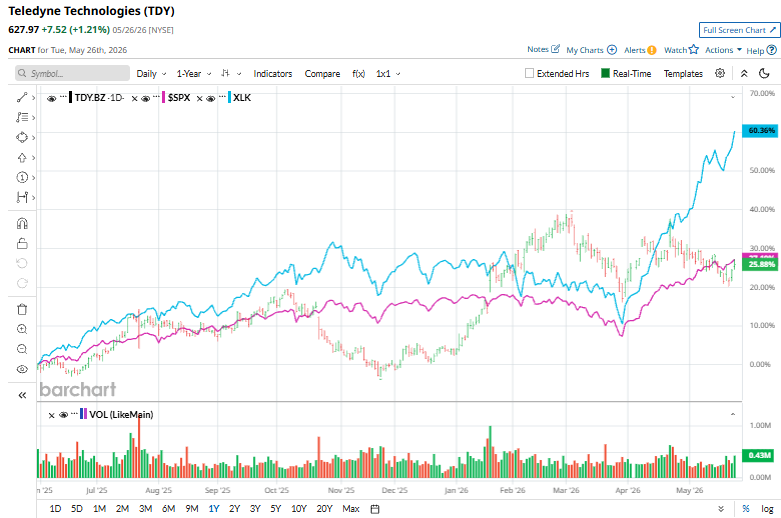

Over the past 52 weeks, the company’s stock has surged by 29.2%, and it is up by 23% year-to-date. In contrast, the S&P 500 Index ($SPX) has gained around 29.6% over the past year and 9.8% this year.

Furthermore, the stock has trailed behind the State Street Technology Select Sector SPDR ETF (XLK), which is up 63.3% over the past 52 weeks and has delivered a 28.6% YTD rise.

Shares of Teledyne Technologies rose 2.2% on Apr. 22 after the company reported stronger-than-expected first-quarter fiscal 2026 results. Teledyne posted record quarterly sales of $1.56 billion, up 7.6% year over year, while non-GAAP EPS increased 17.2% to $5.80. Management highlighted continued strength in defense electronics and infrared imaging technologies, alongside improving demand trends in shorter-cycle industrial and semiconductor-related markets. Operating margins also expanded to 22.6% year over year on a non-GAAP basis, driven by favorable product mix, pricing actions, and operational efficiencies.

For the fiscal year 2026, ending in December, Wall Street analysts expect Teledyne’s EPS to grow 9.5% YOY to $24.07 on a diluted basis. The company has a solid history of surpassing consensus estimates, topping in each of the trailing four quarters.

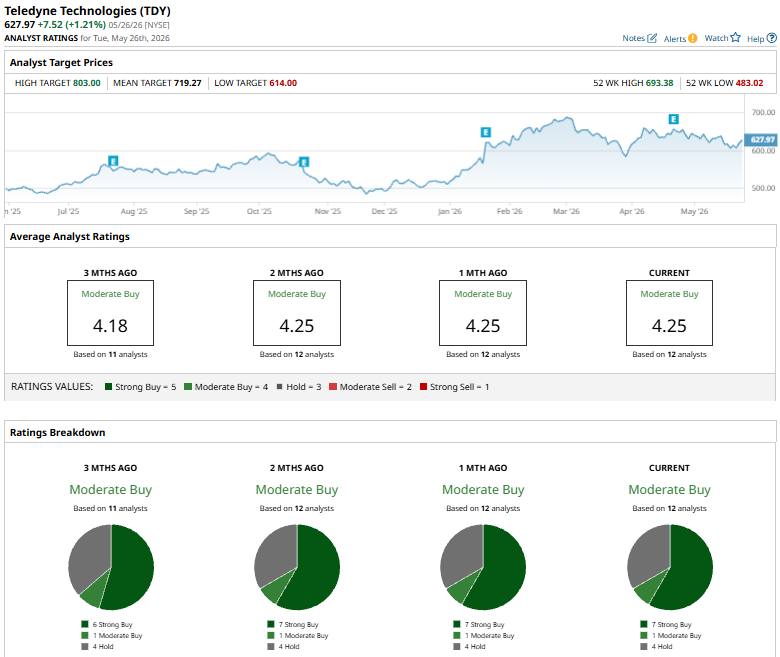

Among the 12 Wall Street analysts covering Teledyne’s stock, the consensus is a “Moderate Buy.” That’s based on seven “Strong Buy” ratings, one “Moderate Buy,” and four “Holds.”

This configuration is bullish than three months ago, when the stock had six “Strong Buy” suggestions.

On May 3, Greg Konrad raised the price target on Teledyne Technologies to $775 from $770 while maintaining a “Buy” rating on the shares. The analyst cited the company’s better-than-expected quarterly results and increased guidance, expressing confidence that Teledyne is re-entering a positive earnings revision cycle driven by strength in its defense business and improving trends in shorter-cycle industrial markets.

Teledyne’s mean price target of $719.27 indicates a 14.5% premium over current market prices. Moreover, the Street-high price target of $803 implies a potential upside of 27.9%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)