Alexandria Real Estate Equities, Inc. (ARE) is a specialized real estate investment trust (REIT) focused on the life sciences industry, with a portfolio centered around research-driven innovation hubs across the United States. Founded in 1994, the company played a major role in establishing the life science real estate niche and has since built a large presence in key biotechnology and research markets, including Boston, the San Francisco Bay Area, San Diego, Seattle, Maryland, Research Triangle, and New York City.

The company develops and operates large-scale collaborative campuses designed to serve biotechnology, pharmaceutical, and scientific research tenants. But despite its established position in the life sciences real estate market, Alexandria Real Estate has struggled to gain traction on Wall Street. The company, currently valued at roughly $8.43 billion by market capitalization, has seen its shares tumble about 29.5% over the past year, sharply underperforming the broader S&P 500 Index ($SPX), which rallied 28% during the same period.

The weakness has carried into 2026, with the stock slipping another 1.2% year-to-date (YTD), even as the broader market has climbed 9.2%. The underperformance becomes even more noticeable when compared to sector peers. The State Street Real Estate Select Sector SPDR ETF (XLRE) has gained roughly 9.7% over the past 12 months and another 10.4% so far this year, underscoring how significantly Alexandria has lagged both the broader market and the real estate sector.

Alexandria Real Estate’s weak stock performance reflects the mounting pressures facing the life sciences real estate market. Investor concerns intensified after the company released a mixed set of first-quarter 2026 results on Apr. 27, sparking a sharp selloff that sent the stock down nearly 11.3% in the following trading session. While the REIT managed to edge past revenue expectations, the broader results highlighted growing operational challenges.

Alexandria reported revenue of $671 million, slightly above Wall Street estimates of $668 million, but still well below the $778 million generated in the year-ago quarter. Profitability also weakened, with adjusted funds from operations (FFO) falling 25% year over year to $1.73 per share, while basic EPS came in at $2.10. The softer performance was closely tied to weakening property fundamentals. Operating occupancy declined sharply to 87.7%, down from 90.9% in the previous quarter, largely due to several major lease expirations early in the year.

The company has also faced increasing pressure from slower funding activity and weaker tenant demand across the life sciences sector, trends that continue to weigh on this highly specialized segment of the REIT market. Moreover, investor unease has been compounded by the company’s significant dividend cut, a move widely viewed as a sign that conditions in the life sciences real estate space remain difficult despite Alexandria’s longstanding position in the industry.

Looking ahead, Wall Street expects Alexandria to remain under pressure in fiscal 2026, with analysts forecasting FFO to decline nearly 29% year over year to $6.40 per share. The company’s earnings surprise history has also been mixed. While Alexandria managed to meet or exceed consensus estimates in three of the past four quarters, it also fell short on one occasion, highlighting the uneven operating environment the REIT continues to navigate.

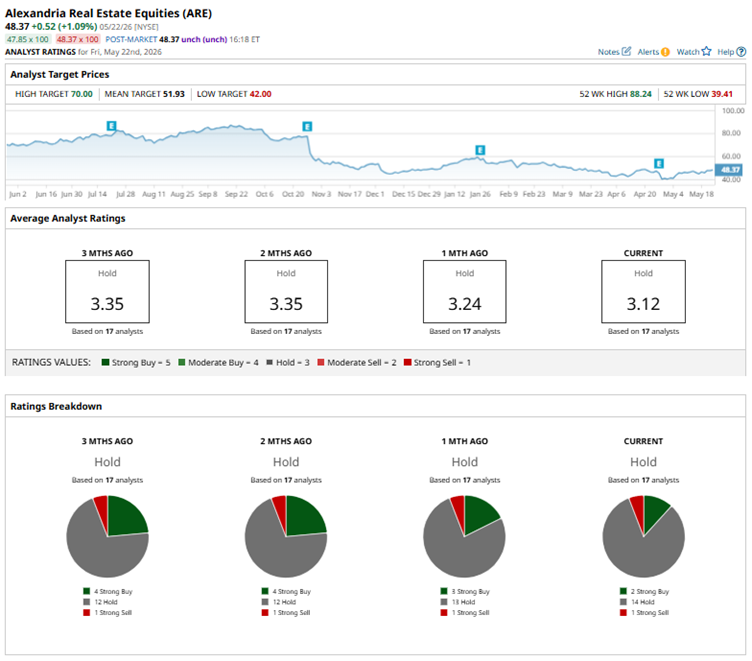

Wall Street’s stance on Alexandria Real Estate remains largely cautious, with the stock currently carrying a consensus “Hold” rating from 17 analysts. The breakdown includes two “Strong Buy” ratings, 14 “Holds,” and one “Strong Sell.” Sentiment has also softened slightly over the past month, as the number of “Strong Buy” recommendations has slipped from three to two, a sign that analysts have become somewhat more cautious on the REIT’s near-term outlook.

In late April, Cantor Fitzgerald turned more cautious on Alexandria Real Estate, cutting its price target on the stock to $43 from $60 while maintaining a “Neutral” rating, reflecting growing concerns around the company’s operating environment and near-term growth outlook. Even so, Wall Street’s broader view suggests analysts still see room for recovery. The average price target of $51.93 implies roughly 7.4% upside from current levels, while the Street-high target of $70 points to a potential rally of nearly 45%.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)