/Republic%20Services%2C%20Inc_%20trash%20truck-by%20refina%20via%20Shutterstock.jpg)

With a market cap of $66.1 billion, Republic Services, Inc. (RSG) is a leading environmental services company that provides waste collection, recycling, disposal, and industrial waste management solutions across the United States and Canada. It serves residential, commercial, and industrial customers through its extensive network of recycling centers, transfer stations, and landfills.

Shares of the Phoenix, Arizona-based company have underperformed the broader market over the past 52 weeks. RSG stock has decreased 16% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 24.7%. Moreover, shares of the company are down marginally on a YTD basis, compared to SPX’s 8.2% gain.

Focusing more closely, shares of Republic Services have lagged behind the State Street Industrial Select Sector SPDR ETF’s (XLI) 18.9% return over the past 52 weeks.

Republic Services posted strong Q1 2026 results on May 7, including 2.6% revenue growth, 4.3% adjusted EBITDA growth, 50-basis-point margin expansion to 32.1%, adjusted EPS of $1.70, and a 35% jump in adjusted free cash flow to $984 million. The company also outlined plans to deliver at least $100 million in annual AI and digital benefits by 2028 and exceed $1 billion in acquisitions in 2026. The company reported its first year-over-year growth in the temporary large container business in over two years and projected stronger performance in the second half of 2026. However, the stock fell marginally the next day.

For the fiscal year ending in December 2026, analysts expect RSG’s adjusted EPS to grow 3.6% year-over-year to $7.27. The company's earnings surprise history is promising. It topped the consensus estimates in the last four quarters.

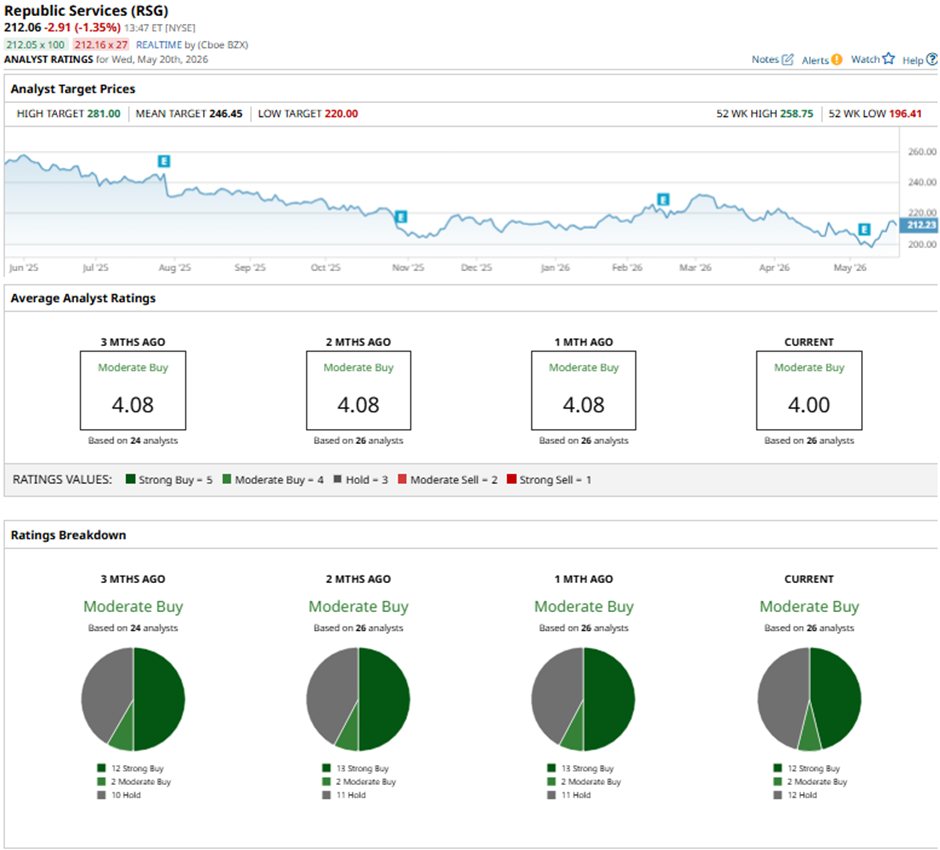

Among the 26 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 12 “Strong Buy” ratings, two “Moderate Buys,” and 12 “Holds.”

On May 12, UBS analyst Jon Windham cut the price target for Republic Services to $223 and maintained a “Neutral” rating.

The mean price target of $246.45 represents a 16.2% premium to RSG’s current price levels. The Street-high price target of $281 suggests a 32.5% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

/EV%20in%20showroom%20by%20Robert%20Way%20via%20Shutterstock.jpg)

/Gen%20Digital%20Inc%20logo%20on%20building-by%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)