Shares of electric vehicle (EV) and energy specialist Tesla (TSLA) have faced a bumpy and volatile stretch on Wall Street throughout 2026, despite growing excitement surrounding the company’s aggressive push into physical artificial intelligence (AI). More than ever, Tesla’s long-term future is becoming tied to the success of its expanding Robotaxi network and autonomous ride-sharing ambitions, transforming the company’s identity from simply an EV maker into a broader AI-driven mobility powerhouse.

Still, investors remain torn between Tesla’s futuristic promise and the mounting pressures weighing on its core business, including slowing EV demand, relentless price competition, and intensifying competition from fast-rising Chinese automakers that are reshaping the global EV landscape. In fact, the pressure has only intensified after reports surfaced that SpaceX could launch its highly anticipated IPO as early as next month.

The prospect of another major Elon Musk-led company entering public markets has fueled fresh concerns on Wall Street over a potential tug-of-war for investor capital, and even management focus, between Musk’s growing empire of companies. As a result, Tesla shares have remained under pressure even as the company pushes deeper into AI-driven mobility and autonomous transportation. Still, not everyone is backing away from the EV giant.

In a striking new vote of confidence, Paul Tudor Jones’s hedge fund, Tudor Investment Corporation, dramatically increased its stake in Tesla to roughly 585,000 shares worth about $217.4 million, up from just 60,000 shares previously, an increase of more than ninefold. The massive boost in exposure, despite the growing list of concerns surrounding Tesla, suggests that at least some major institutional investors still see enormous long-term upside in the company’s AI, autonomy, and Robotaxi-driven future. Thus, here’s a closer look at TSLA.

About Tesla Stock

Founded in 2003 and now headquartered in Austin, Tesla was created with a mission to push electric vehicles into the mainstream and challenge the dominance of traditional gasoline-powered cars. Led by Elon Musk, the company quickly distinguished itself by blending advanced technology with sleek, high-performance design. What began with the niche Roadster eventually evolved into mass-market successes like the Model 3 and Model Y, vehicles that played a major role in accelerating the global shift toward EV adoption.

Over time, however, Tesla has transformed into far more than just an automaker. The company has steadily expanded into energy storage, solar solutions, artificial intelligence, and robotics, with offerings such as the Megapack battery system, Full Self-Driving (FSD) software, and the upcoming Optimus humanoid robot showcasing the scale of its ambitions. Increasingly, Tesla is positioning itself as a broader AI and technology platform, using innovation and automation as the foundation across its entire ecosystem rather than limiting itself to the automotive industry alone.

That vision received fresh attention on May 18 when CEO Elon Musk said he expects fully autonomous vehicles operating without human safety monitors to become increasingly common across the United States later this year, after already being rolled out in Texas. Speaking via video link at the Smart Mobility Summit in Tel Aviv, Musk noted that self-driving Tesla vehicles are already operating in Texas without safety monitors and indicated the rollout would gradually expand nationwide.

But despite its massive scale, ambitions, and market capitalization of roughly $1.54 trillion, Tesla’s stock has struggled to maintain momentum in 2026. Investor sentiment has been pressured by slowing EV demand, concerns surrounding the company’s aggressive spending plans, and growing skepticism over Tesla’s costly push to reinvent itself as a physical AI powerhouse. While the stock has still gained 17.88% over the past 52 weeks, it has significantly trailed the broader S&P 500 Index ($SPX), which has advanced about 23.46% during the same period.

The weakness has become even more pronounced in 2026, with Tesla shares falling nearly 10.33% year-to-date (YTD) while the broader market has climbed roughly 7.6%. In fact, Tesla has emerged as the second-worst-performing stock among the “Magnificent Seven” group this year, trailing only Microsoft (MSFT), highlighting the rapid pace at which Wall Street enthusiasm has cooled despite the company’s sweeping long-term vision.

Inside Tesla’s Q1 Earnings Report

Tesla’s fiscal 2026 first-quarter results, released on April 22, highlighted a company pouring enormous resources into a sweeping transformation, and Wall Street’s reaction reflected just how divided investors remain on that strategy. Although the headline numbers comfortably topped expectations, Tesla shares still slipped roughly 3.6% in the following trading session as concerns around spending and the company’s long-term transition overshadowed the earnings beat. On the surface, the quarter looked impressive. Revenue climbed 16% year-over-year (YOY) to $22.39 billion, ahead of analysts’ expectations of $21.92 billion. Adjusted earnings also came in stronger than expected at $0.41 per share, beating consensus estimates of $0.36 and surging 52% from the prior-year period. Tesla’s traditional EV business continues to serve as the primary engine behind the company’s financial performance. Automotive revenue jumped roughly 16% to $16.2 billion from $14 billion a year earlier, reinforcing that the company’s core vehicle segment remains central to its growth story even as Tesla pushes deeper into AI and robotics.

Profitability metrics showed a notable rebound. Tesla’s total GAAP gross margin improved sharply to 21.1%, up from 16.3% in the year-ago quarter. Meanwhile, automotive gross margin excluding regulatory credits rose to 19.2%, recovering significantly from 12.5% in Q1 2025 and improving from 17.9% in the previous quarter. The improvement suggested that Tesla’s aggressive operational efficiencies and product mix are beginning to offset some of the pricing pressure that has weighed on margins in recent years.

Still, the company acknowledged that the road ahead remains challenging. Tesla pointed to intensifying competition and an increasingly aging vehicle lineup as key risks, prompting plans to launch lower-cost variants of its popular Model Y SUV and Model 3 sedan. The move comes as competitors, especially Chinese EV giants like BYD Company (BYDDY) and Xiaomi (XIACY), continue flooding the market with newer, cheaper, and increasingly advanced electric vehicles, intensifying pressure across the global EV landscape.

From a balance sheet perspective, Tesla remains in a strong financial position. The company ended the quarter with $44.7 billion in cash, cash equivalents, and short-term investments, slightly higher than the $44.1 billion reported previously. That increase was supported by $1.4 billion in free cash flow alongside another $1.2 billion generated through financing activities, although part of those gains was offset by a $2 billion equity investment in SpaceX.

However, the figure that appeared to unsettle investors most was Tesla’s aggressive increase in spending tied to its broader “Physical AI” ambitions. The company raised its 2026 capital expenditure forecast to more than $25 billion, a dramatic leap from the $8.6 billion spent in 2025, as Tesla accelerates investments in AI infrastructure, manufacturing expansion, and next-generation product development. And management cautioned that the heavy spending cycle, particularly around AI training clusters and the Cybercab supply chain, could push free cash flow into negative territory for the remainder of the year.

Looking ahead, Tesla appears focused on squeezing more efficiency from its existing operations before committing to major new factory builds. At the same time, the company said its next-generation product pipeline, including the Cybercab, Semi, and Megapack 3, remains on track for large-scale production in 2026. Early assembly lines for the Optimus humanoid robot are also already being installed, underscoring Tesla’s broader push to evolve from an EV manufacturer into a far-reaching AI and robotics platform.

What Do Analysts Think About Tesla Stock?

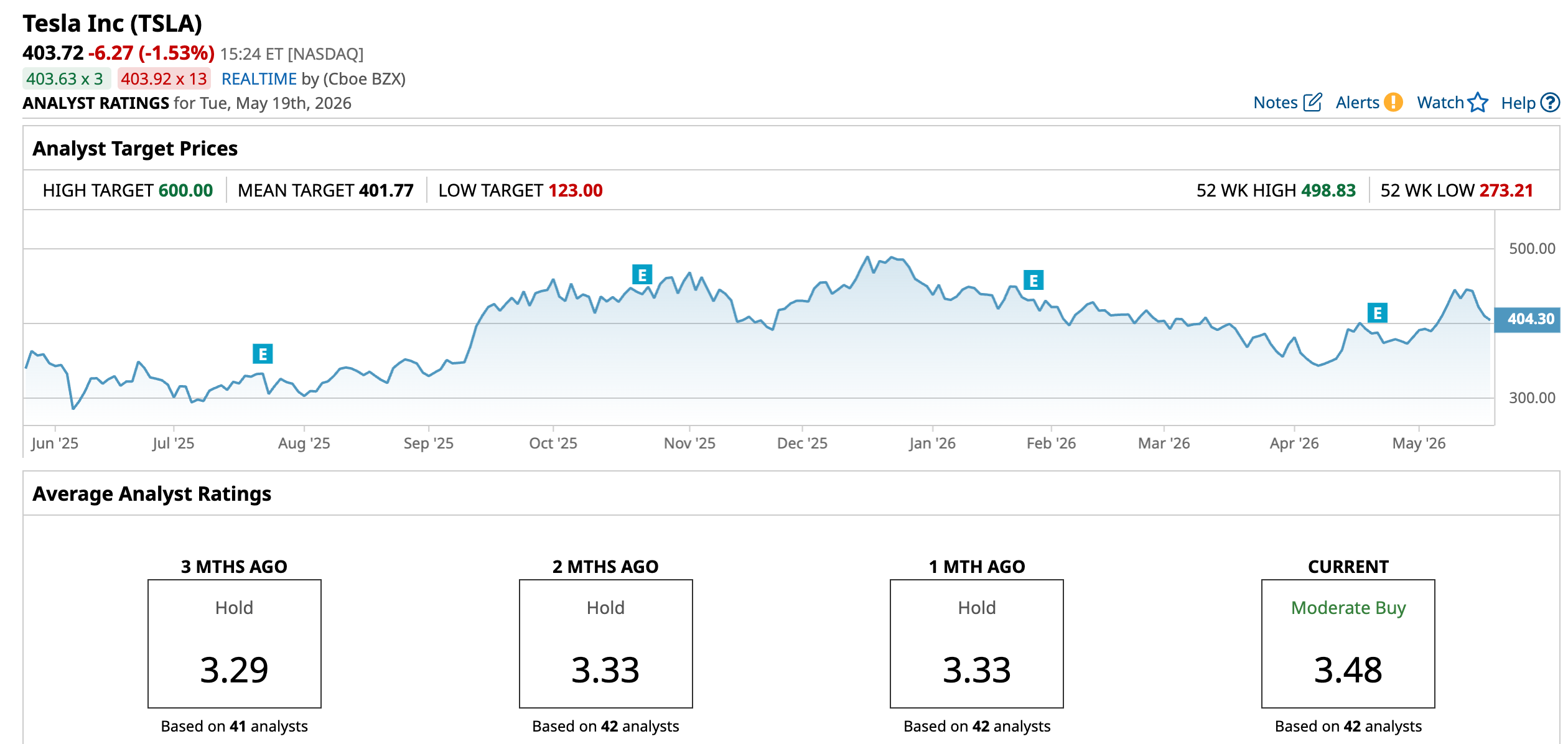

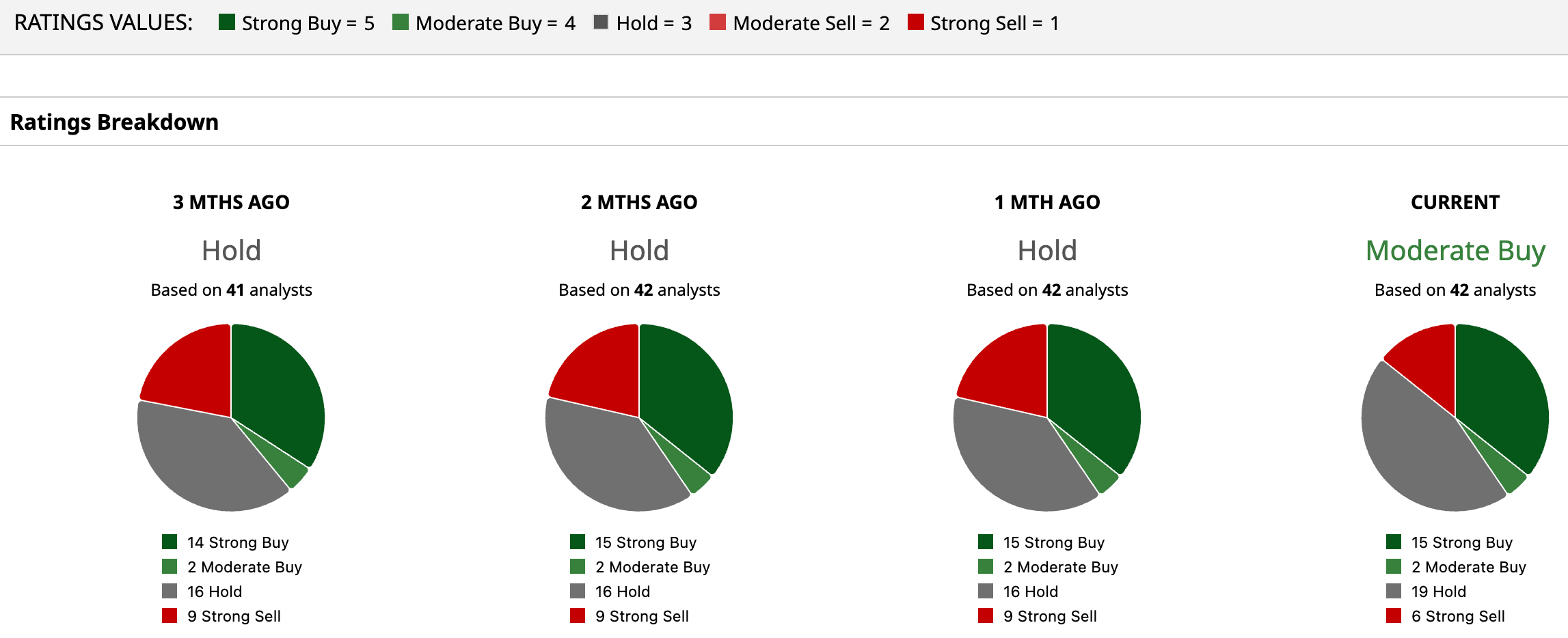

Even though Tesla’s latest earnings report failed to fully impress investors, Wall Street’s broader outlook on the stock has quietly become more optimistic. Tesla now holds a consensus “Moderate Buy” rating, a meaningful improvement from the consensus “Hold” rating it carried just a month earlier. Out of the 42 analysts covering the EV giant, 15 currently recommend “Strong Buy,” two suggest “Moderate Buy,” 19 remain cautious with “Hold” ratings, while six analysts continue to maintain bearish “Strong Sell” calls.

While Tesla shares are already trading slightly above the average analyst price target of $401.77, some bulls on Wall Street still see substantial upside ahead. The Street-high target of $600 implies the stock could surge another 48.6% from current levels, reflecting growing confidence among optimistic analysts that Tesla’s long-term AI, autonomy, and robotaxi ambitions could eventually outweigh its near-term challenges.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Doctor%20stacking%20healthcare%20medical%20insurance%20icons%20by%20Dilok%20via%20Adobe%20Stock.jpeg)