/Textron%20Inc_%20magnified%20logo-by%20Pavel%20Kapysh%20via%20Shuuerstock.jpg)

Providence, Rhode Island-based Textron Inc. (TXT) operates in the aircraft, defense, industrial, and finance businesses worldwide. With a market cap of $17.1 billion, the company operates in six segments: Textron Aviation, Bell, Textron Systems, Industrial, Textron eAviation, and Finance.

Shares of this multi-industry company have outperformed the broader market over the past year. TXT has surged 35.7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 12.9%. In 2026, TXT stock is up 13.3%, compared to the SPX’s marginal dip on a YTD basis.

Narrowing the focus, TXT has also surpassed the iShares U.S. Aerospace & Defense ETF (ITA). The exchange-traded fund has gained about 48.7% over the past year and 8.3% rise on a YTD basis.

On Jan. 28, Textron reported fourth-quarter earnings, after which its shares tanked 7.9%. Revenue rose 16% year over year to about $4.2 billion, and adjusted EPS increased roughly 29% to $1.73, driven by higher aircraft deliveries at Textron Aviation and strong military demand at Bell, with additional support from operational improvements and easing supply-chain constraints. However, the otherwise solid quarter was overshadowed by a softer 2026 outlook, as the company guided adjusted EPS to $6.40–$6.60 and warned of lower manufacturing cash flow due to elevated investment in the MV-75 program.

For the current fiscal year, ending in December, analysts expect TXT’s EPS to grow 7.1% to $6.53 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in three of the last four quarters, while missing on another occasion.

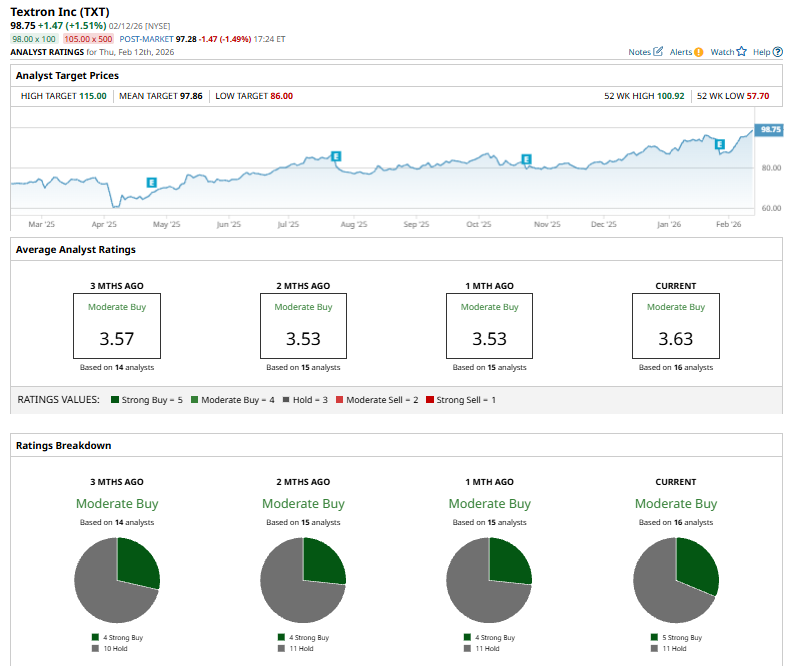

Among the 16 analysts covering TXT stock, the consensus is a “Moderate Buy.” That’s based on five “Strong Buy” ratings and 11 “Holds.”

This configuration is bullish than a month ago, with four analysts suggesting a “Strong Buy.”

On Feb. 2, Jefferies analyst Sheila Kahyaoglu reiterated a “Buy” rating on Textron while trimming the price target to $110 from $115, reflecting a modestly tempered valuation outlook without altering her positive investment stance.

While the company currently trades above the mean price target of $97.86, the Street-high price target of $115 suggests an ambitious upside potential of 16.5%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Salesforce%20Inc%20HQ%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

/Semiconductor%20close%20up%20by%20Yosi%20Azwan%20via%20iStock.jpg)