With a market cap of $23.9 billion, Equity Residential (EQR) is a leading real estate company that owns and manages 312 rental properties comprising over 85,000 apartment units across major U.S. metro areas. It focuses primarily on dynamic coastal markets while maintaining a strong presence in high-growth cities such as Atlanta, Austin, Dallas, and Denver.

Shares of the Chicago, United States-based company have underperformed the broader market over the past 52 weeks. EQR stock has declined 9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 23.9%. Moreover, shares of the company are up 3.3% on a YTD basis, compared to SPX’s 7.9% gain.

Zooming in further, shares of Equity Residential have lagged behind the State Street Real Estate Select Sector SPDR ETF’s (XLRE) 3.7% return over the past 52 weeks.

Shares of Equity Residential rose marginally following its Q1 2026 results on Apr. 28. The company reported improving fundamentals in key markets like San Francisco and New York, with leasing concessions down 21%, physical occupancy rising to 96.5%, bad debt improving by 10 basis points, and Normalized FFO per share increasing 4.2% year-over-year to $0.99 despite weaker EPS and FFO figures.

Investor sentiment was further supported by the company’s $219.4 million share repurchase program, a 1.4% dividend increase to $2.81 annually, and upbeat Q2 2026 guidance projecting FFO per share of $0.97 - $1.01 and Normalized FFO per share of $0.98 - $1.02.

For the fiscal year ending in December 2026, analysts expect EQR’s NFFO per share to rise 2.5% year-over-year to $4.09. The company’s earnings surprise history is mixed. It beat or met the consensus estimates in three of the last four quarters while missing on another occasion.

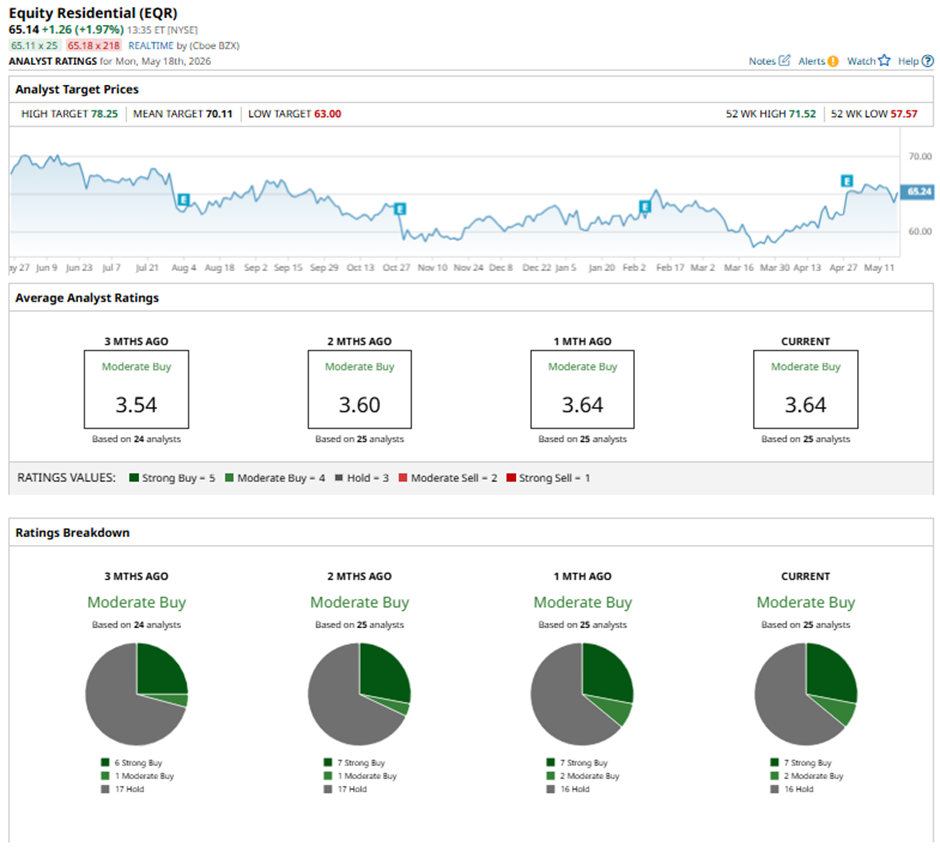

Among the 25 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on seven “Strong Buy” ratings, two “Moderate Buys,” and 16 “Holds.”

On May 4, BofA raised its price target for Equity Residential to $75 while maintaining a “Neutral" rating.

The mean price target of $70.11 represents a 7.6% premium to EQR’s current price levels. The Street-high price target of $78.25 suggests a 20.1% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)