Nvidia (NVDA) stock hit a record high on May 14 amid reports that the company has received approval to sell its H200 chips to 10 Chinese firms, including Alibaba (BABA), which has developed its own artificial intelligence (AI) chips. At $5.46 trillion today, Nvidia’s market capitalization is on its way to approaching the $6 trillion mark. If Nvidia can achieve that feat, it would become the first company to do so, repeating the success it saw as the first-ever company to hit a market cap of $4 trillion and later $5 trillion.

Meanwhile, Nvidia will report fiscal first-quarter 2027 earnings on May 20 after the market close. Let's take a closer look and gauge whether NVDA stock can continue to rally following the Q1 confessional.

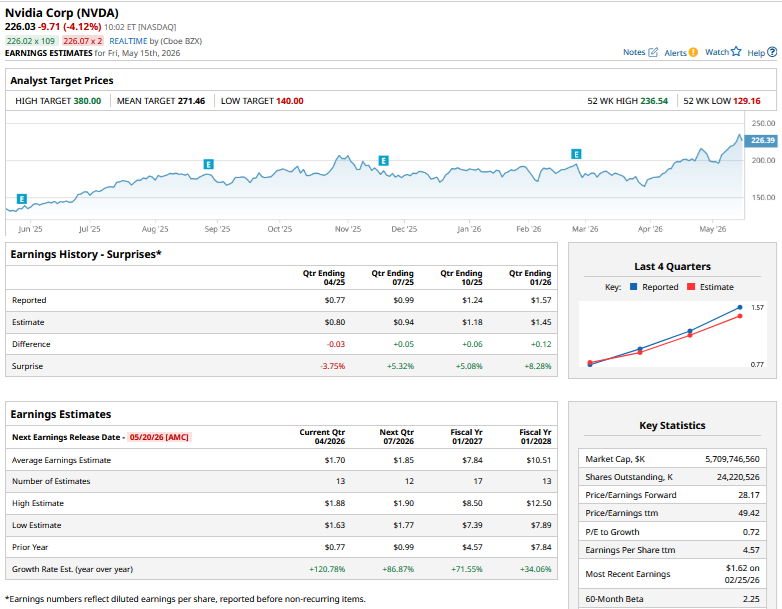

Nvidia's Q1 Earnings Estimates

Analysts expect Nvidia to report revenue of $79.2 billion in Q1, which would mark a year-over-year (YOY) rise of nearly 80%. This estimate is higher than even the top end of Nvidia’s outlook, which is unsurprising as the company invariably beats its guidance. Notably, when Nvidia provided Q1 guidance during the fiscal Q4 2026 earnings call, it was ahead of even the most bullish projections.

As for earnings, analysts are modeling for Q1 EPS to rise 121% YOY to $1.70 per share.

What Do Analysts Think of Nvidia Stock?

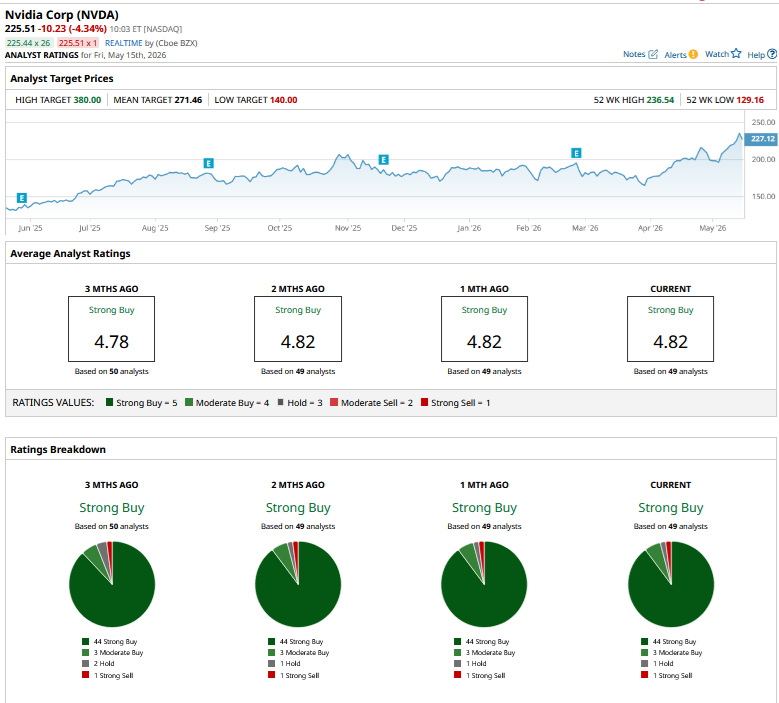

The sell-side analyst community is upbeat on Nvidia heading into earnings. Cantor Fitzgerald, UBS, Bank of America, Wells Fargo, and Susquehanna have all raised their price targets on NVDA stock ahead of the report.

Overall, Nvidia has a consensus “Strong Buy” rating from 49 analysts tracked by Barchart. The mean target price is $273.16, which implies roughly 23% potential upside from current levels.

Should You Buy Nvidia Stock?

While Nvidia pretty much had a home run in the AI chip market initially, the competitive pressure is rising. Hyperscalers like Amazon (AMZN) and Alphabet (GOOGL) are looking to sell their own chips to third parties. Citizens JMP expects Alphabet’s Tensor Processing Unit (TPU) sales to reach about $3 billion in 2026, then rise to $25 billion in 2027. Meanwhile, Amazon estimates that if its chip business were a standalone company, its annual revenue would be $50 billion. Elsewhere, Elon Musk has roped in Intel (INTC) as a partner for Terafab, a massive semiconductor project from Tesla (TSLA), SpaceX, and xAI.

Dependence upon hyperscalers has been a risk for Nvidia, but the company has been looking to diversify its customer base. Sovereign AI and physical AI could be the next growth drivers, and while the former was a $30 billion business for Nvidia last year, the latter generated $6 billion in revenue. Nvidia has also touted the revenue opportunity from autonomous vehicles as companies like Tesla, Waymo, and Uber (UBER) continue to scale up robotaxi operations.

NVDA stock trades at a forward price-to-earnings (P/E) raito of 30 times, while the P/E-to-growth (PEG) multiple is 0.74 times. Usually, these valuations — particularly a PEG multiple below 1, which is rare among Big Tech companies — would have made Nvidia a screaming buy. However, there are genuine concerns over the sustainability of the current growth that Nvidia is witnessing.

Many fear AI chip sales might not continue to keep growing the way they have over the last three years, and that eventually the competition will catch up. That said, I believe we are still in the initial phase of the AI buildout, and that more companies will join the race. Given the demand for chips, there is also plenty of room for other chipmakers to joyfully thrive alongside Nvidia.

Another potential trigger for Nvidia is the resumption of sales to China, which could help add billions more to the firm's burgeoning revenues and profits. Finally, Q1 earnings could mark yet another beat, and investors should hear upbeat commentary from Huang and the rest of management.

Overall, I see potential for NVDA stock to head higher after the Q1 report, even as the recent rally lowers the scope for a major post-earnings pop.

On the date of publication, Mohit Oberoi had a position in: NVDA, TSLA, AMZN, GOOG, BABA. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/United%20Parcel%20Service%2C%20Inc_%20logo%20on%20truck-by%20100pk%20via%20iStock.jpg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)