/NVIDIA%20Corp%20logo%20on%20phone-by%20Evolf%20via%20Shutterstock.jpg)

Nvidia’s (NVDA) upcoming earnings report is shaping up to be one of the biggest checkpoints for the AI trade this spring. Shares of Nvidia have climbed to record territory as investors continue to bet that spending on data-center chips, networking gear, and AI software will stay strong, even after a volatile stretch for semiconductor stocks.

The chipmaker is due to report fiscal 2026 first-quarter results on May 20 after the market close, and that date now sits at the heart of the market’s calendar. The question is no longer whether Nvidia matters to the AI boom, but how much more of that boom is already priced into NVDA stock? Let's take a closer look.

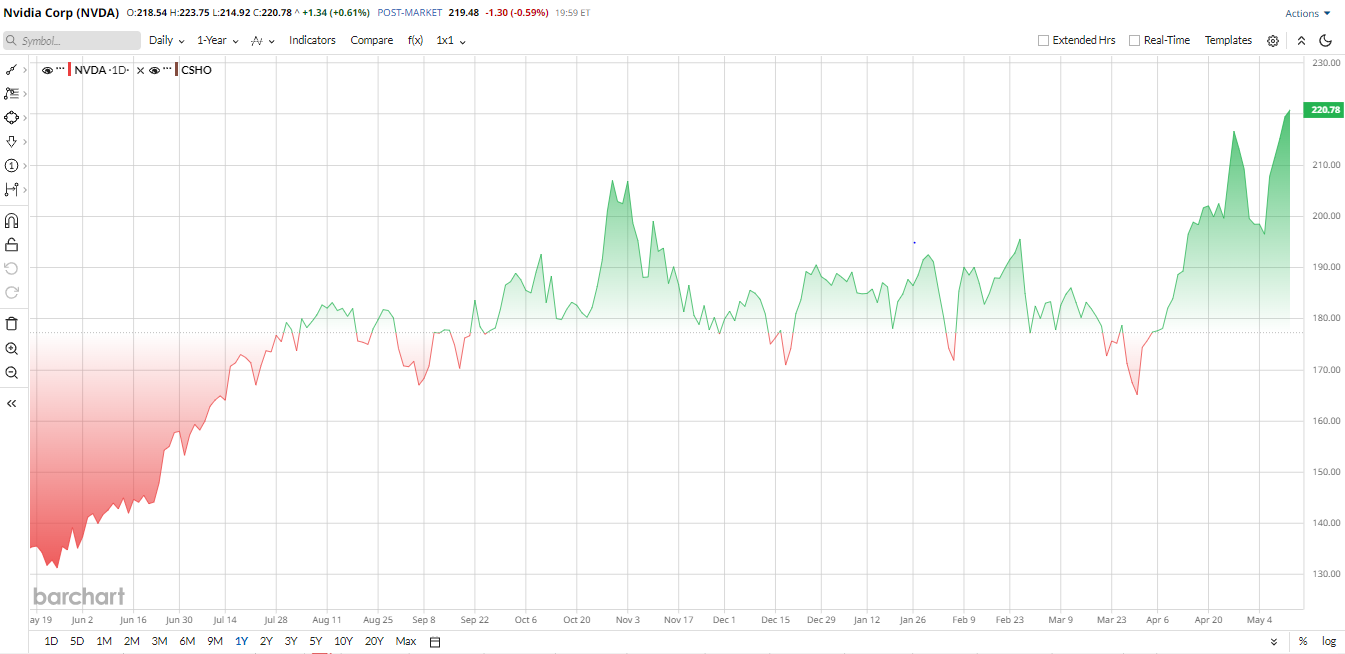

A Strong Stock Run, Yet Reasonable Valuation

Nvidia has already had a strong 2026. NVDA stock is up about 26% year-to-date (YTD) and has climbed 74% over the past 12 months, helped by steady demand for data-center chips and the market’s willingness to pay up for AI exposure.

Despite the massive run, NVDA is trading at an attractive valuation. Nvidia trades at roughly 28 times forward earnings, which is below the semiconductor industry median of about 32 times. That makes the stock look less demanding on one common measure.

But on enterprise value-to-EBITDA, Nvidia is at about 37 times, which is above the sector median of roughly 27 times. That suggests the market still assigns a premium for growth, scale and execution. In other words, Nvidia is not cheap across the board, even if one valuation yardstick looks friendlier than the other.

The Hyperscaler Spending Boom Is Fueling Nvidia’s AI Demand

The biggest cloud companies are still spending massive amounts on AI infrastructure, and that continues to support Nvidia’s growth story. Microsoft (MSFT) plans to spend about $190 billion in 2026, while Amazon (AMZN) still expects roughly $200 billion in capital expenditures this year. Alphabet (GOOGL) has also said its annual capex — already projected between $180 billion and $190 billion — will rise even further in 2027. That spending is largely tied to AI data centers and advanced chips.

Nvidia remains the dominant AI GPU supplier, so rising infrastructure budgets could directly boost demand. The trend is also showing up across the chip sector. AMD (AMD) recently reported 38% year-over-year (YOY) revenue growth to $10.3 billion, while its data-center revenue surged 57% to $5.8 billion, thanks to stronger GPU shipments. Analysts expect similar results for Nvidia, too.

Why Nvidia's Upcoming Earnings Matter

Nvidia's Q1 earnings matter because they give investors a fresh test of whether Nvidia can keep turning AI demand into hard numbers. The stock has already moved a long way on expectations, so traders will likely care most about the outlook for the next quarter and the rest of the year.

Wall Street is still looking for another strong report. Consensus estimates point to earnings of $1.70 per share, up more than 120% from a year ago, with revenue expected in the mid-$70 billion range. That would follow a quarter in which Nvidia posted revenue of $68.1 billion, up 73% YOY, and data-center revenue of $62.3 billion, up 75% YOY.

Options traders are also bracing for a sizable move. One recent read put the expected swing at about 8.8% around earnings, with implied volatility at 53%, which suggests the market is pricing in a sharp reaction even if the results are solid.

Nvidia has beaten estimates in three of the last four quarters, but guidance, Blackwell shipments, and cloud demand will likely matter just as much as the headline numbers.

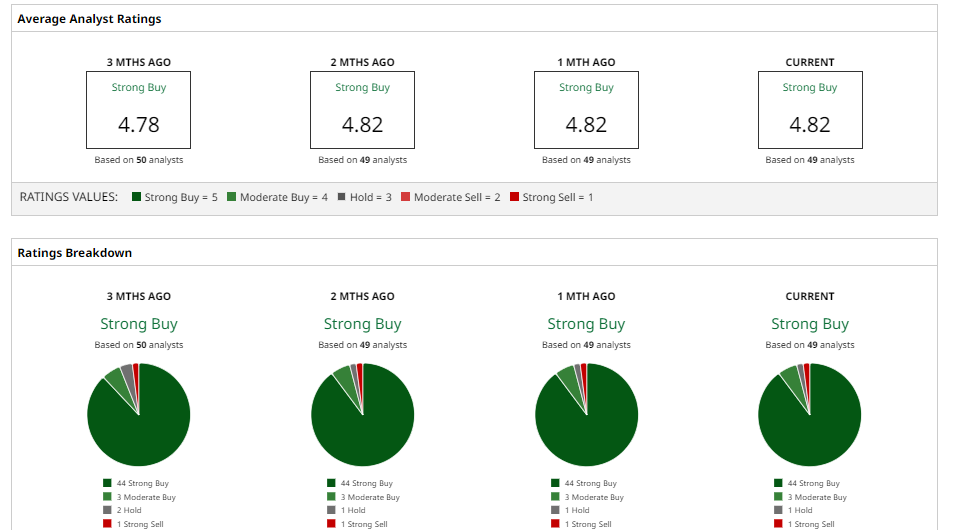

What Does Wall Street Think of NVDA Stock?

Wall Street remains broadly positive on Nvidia, even after NVDA stock’s strong run. Morgan Stanley recently kept an “Overweight” rating and a $260 price target, saying the shares still look workable for investors who want AI exposure. Goldman Sachs kept a “Buy” rating with a $250 target, while Citi also kept a constructive view and pointed to continued demand later this year.

The overall message is still bullish. NVDA stock has a consensus “Strong Buy” rating with a mean price target of $271.03, which implies about 15% potential upside from current levels. That leaves room for more gains if May 20 brings another clean beat and a confident outlook.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)