Broadcom (AVGO) delivered strong quarterly numbers, but investors were not impressed. The semiconductor giant beat Wall Street's earnings expectations and posted solid year-over-year revenue growth. However, revenue came in slightly below analysts' forecasts.

Shares of Broadcom fell more than 13% in early market trading following the earnings release. The biggest disappointment was management's artificial intelligence (AI) revenue outlook.

Despite the explosive demand for AI infrastructure, Broadcom simply reiterated its existing guidance rather than raising it. The company forecasts approximately $56 billion in AI semiconductor revenue for fiscal 2026, representing roughly 180% year-over-year (YoY) growth. Management reaffirmed expectations for more than $100 billion in AI semiconductor revenue by fiscal 2027, supported by multi-year customer commitments and growing orders from hyperscale cloud providers.

While the guidance remains solid, investors were hoping for an upward revision. Instead, Broadcom chose to stay conservative, and the market responded negatively.

Nonetheless, the post-earnings selloff is an attractive buying opportunity as Broadcom’s growth trajectory remains solid. Broadcom remains well-positioned to benefit from the AI spending boom through its rapidly growing custom AI chip business and its industry-leading networking portfolio. As hyperscalers continue investing heavily in next-generation AI infrastructure, both businesses could drive strong revenue and earnings growth for years to come.

Broadcom's AI Growth Story Is Far Stronger Than the Market Thinks

Investors punished Broadcom after management didn’t raise its long-term AI revenue forecast. But the company's AI business continues to grow at an extraordinary pace. Broadcom generated $10.8 billion in AI semiconductor revenue during fiscal Q2, up 143% YoY, driven by surging demand for custom AI accelerators (XPUs) and AI networking solutions.

Further, Broadcom’s growth is accelerating. Management expects AI semiconductor revenue to reach $16 billion in fiscal Q3, representing more than 200% YoY growth. That would mark another significant step higher from an already massive revenue base.

Supporting Broadcom's outlook is its solid order book. During the quarter, customers placed more than $30 billion of AI semiconductor orders, while Broadcom shipped $10.8 billion.

Further, Broadcom reiterated its expectation to generate more than $100 billion in AI semiconductor revenue in fiscal 2027. Moreover, management expects AI semiconductor revenue growth to continue into fiscal 2028. The solid growth outlook reflects long-term commitments from some of the world's largest AI companies.

Broadcom recently expanded its strategic partnership with Google (GOOG) (GOOGL), signing a long-term agreement to develop and supply multiple generations of TPU chips and AI networking infrastructure. The company is also deepening its relationship with Anthropic. Meanwhile, Broadcom has already delivered silicon to OpenAI and remains on track for production deployments in late 2026.

Meta (META) is becoming another major growth driver. In April, Broadcom announced a partnership to support multiple generations of Meta's MTIA AI accelerators. Moreover, for Broadcom's remaining AI customers, shipments are expected to begin in late 2026 and ramp significantly throughout 2027. To date, the company has already secured approximately $6 billion in purchase orders from these two customers.

In short, the market may have wanted a higher long-term AI revenue forecast, but the underlying story remains intact. AI revenue is growing at triple-digit rates, bookings are running well ahead of shipments, and Broadcom has secured multi-year commitments from many of the largest AI builders worldwide. All these indicate that Broadcom is well-positioned to deliver solid growth ahead, supporting its share price rally.

Is AVGO Stock a Buy on Dip?

Broadcom's growth story remains solid as the demand for the company's custom AI accelerators continues to surge. Meanwhile, Broadcom's networking business is gaining traction, providing an additional catalyst for growth.

These powerful AI-driven trends position Broadcom to deliver robust revenue and earnings growth in the years ahead.

Further, the post-earnings dip will make AVGO's valuation more compelling. Wall Street expects Broadcom's earnings to increase by about 76% in fiscal 2026 and another 67% in fiscal 2027. Given the solid earnings growth outlook, Broadcom stock appears attractively valued relative to its future earnings potential.

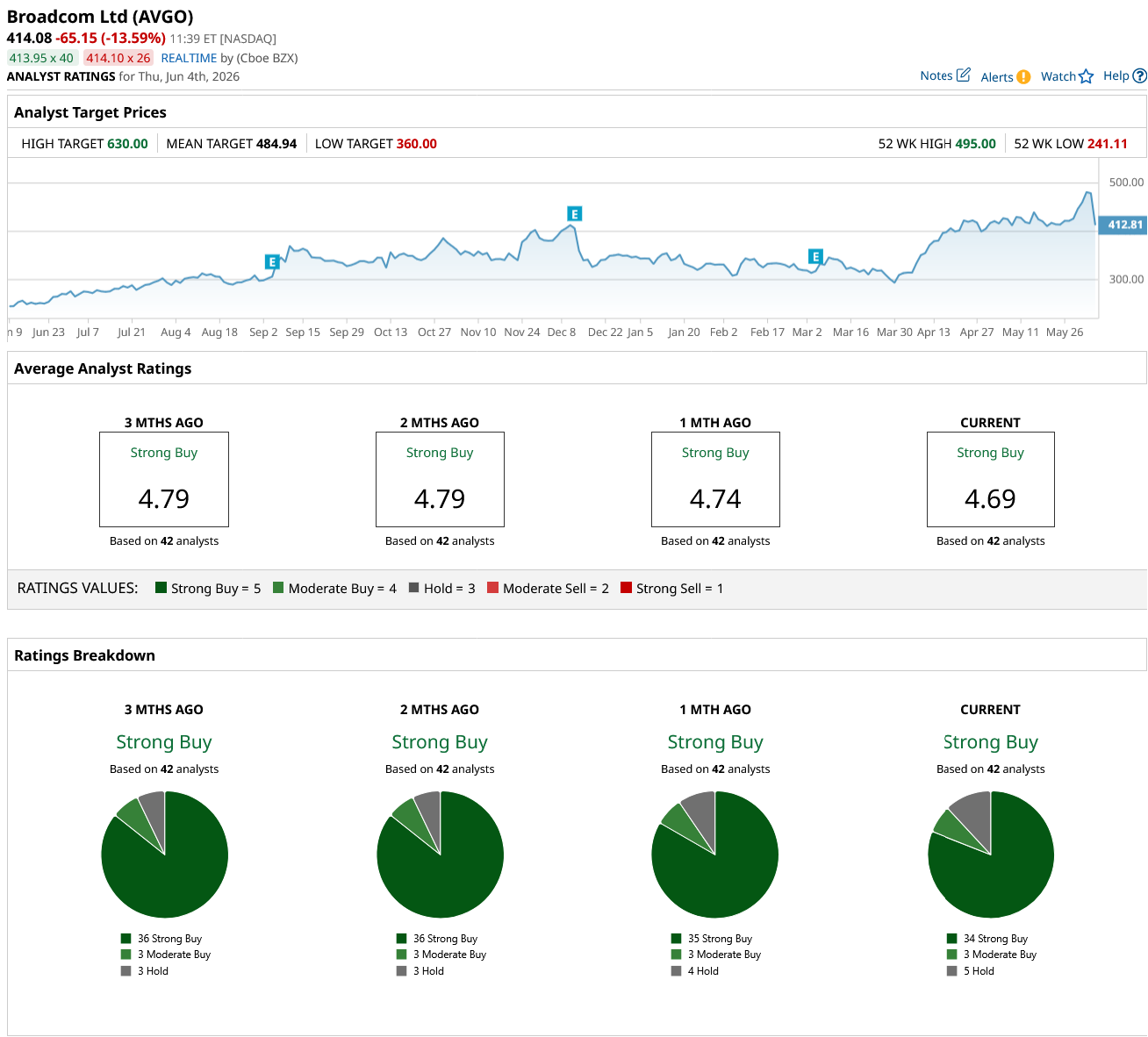

Analysts remain bullish, with AVGO currently carrying a “Strong Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

/Broadcom%20Inc%20HQ%20photo-by%20Sundry%20Photogrpahy%20via%20iStock.jpg)

/AI%20(artificial%20intelligence)/3D%20Graphics%20Concept%20Big%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)