With a market cap of $74.4 billion, CRH plc (CRH) is a leading provider of building materials and infrastructure solutions, serving markets across Ireland, the United States, the United Kingdom, Europe, and other international regions. It manufactures and supplies a wide range of products, including cement, aggregates, concrete, asphalt, precast concrete, and outdoor living solutions for residential, commercial, and large-scale infrastructure projects.

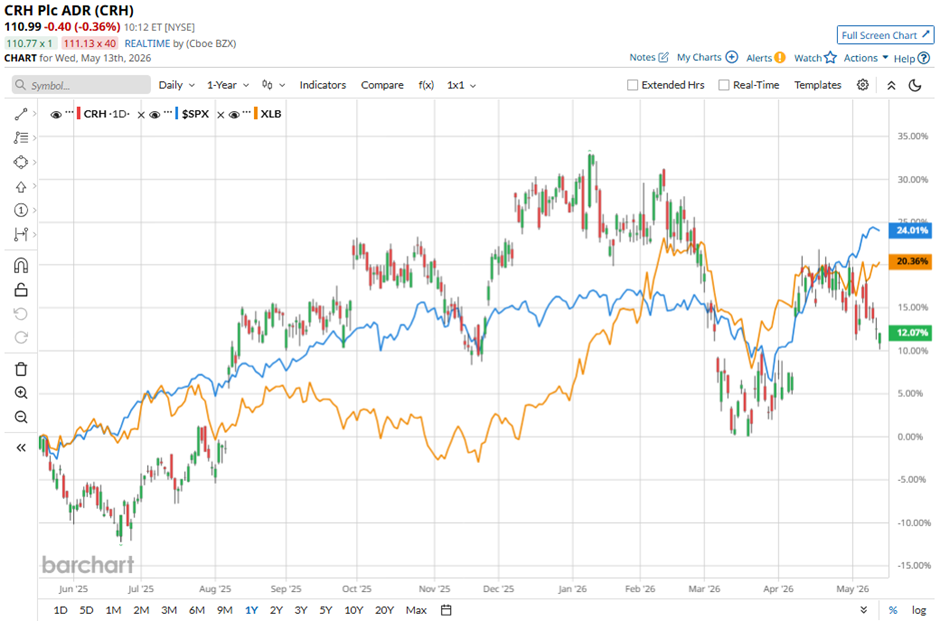

Shares of the Dublin, Ireland-based company have underperformed the broader market over the past 52 weeks. CRH stock has returned 11.4% over this time frame, while the broader S&P 500 Index ($SPX) has gained 25.6%. Moreover, shares of the company have declined 12.4% on a YTD basis, compared to SPX's nearly 8% rise.

Looking closer, shares of CRH have lagged behind the State Street Materials Select Sector SPDR ETF's (XLB) 21.1% increase over the past 52 weeks.

Shares of CRH rose 4.4% on Apr. 30 after the company reported stronger-than-expected Q1 2026 results, with total revenue increasing 9% year-over-year to $7.4 billion and adjusted EBITDA rising 18% to $600 million, while EBITDA margin improved to 8%. Investor sentiment was further boosted by CRH reaffirming its full-year 2026 guidance, including expected net income of $3.9 billion to $4.1 billion and adjusted EBITDA of $8.1 billion to $8.5 billion.

For the fiscal year ending in December 2026, analysts expect CRH's EPS to grow 6.6% year-over-year at $5.94. The company's earnings surprise history is mixed. It has exceeded or met the consensus estimates in three of the last four quarters while missing on three other occasions.

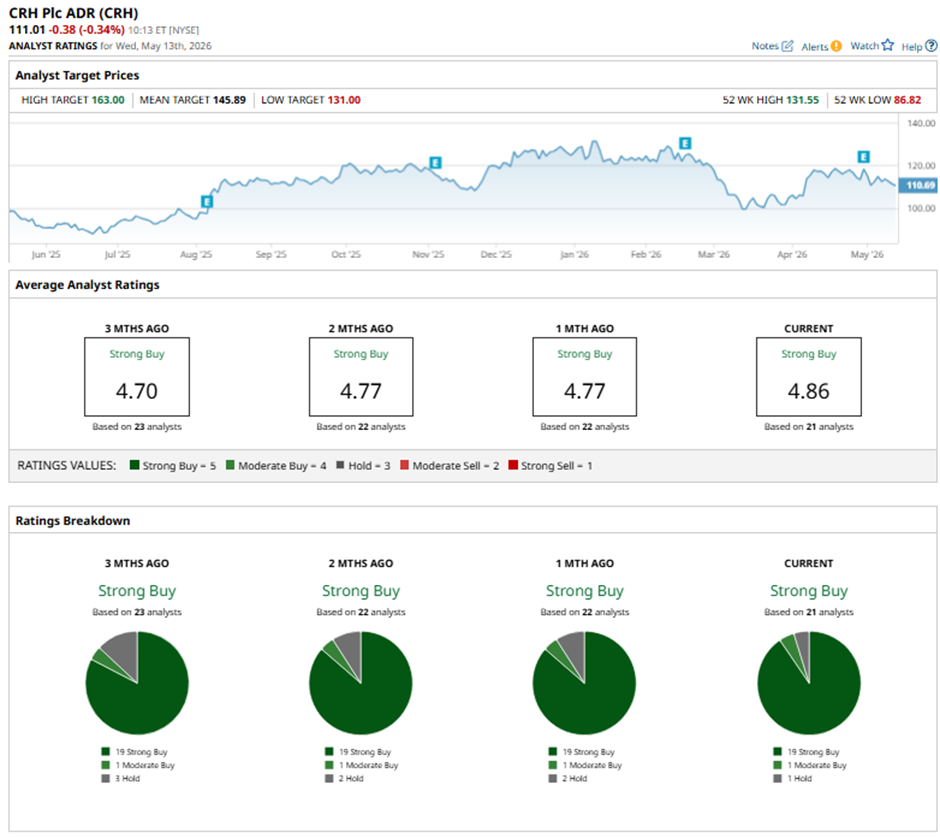

Among the 21 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on 19 “Strong Buy” ratings, one “Moderate Buy,” and one “Hold.”

On Mar. 3, JPMorgan raised its price target for CRH to $140 and maintained an “Overweight” rating.

The mean price target of $145.89 represents a 31.4% premium to CRH’s current price levels. The Street-high price target of $163 suggests a 46.8% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)