With a market cap of $6.2 billion, The Campbell's Company (CPB) is a leading manufacturer and marketer of food, beverage, and snack products, operating through its Meals & Beverages and Snacks segments across the United States and international markets. It offers well-known brands such as Campbell’s soups, Prego, V8, Goldfish, Pepperidge Farm, and Rao’s through a wide retail and foodservice distribution network.

Shares of the Camden, New Jersey-based company have underperformed the broader market over the past 52 weeks. CPB stock has dropped 43% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 25.6%. On a YTD basis, shares of the company are down 26.5%, compared to SPX’s 7.2% gain.

Focusing more closely, shares of Campbell's have lagged behind the State Street Consumer Staples Select Sector SPDR ETF’s (XLP) 4.2% gain over the past 52 weeks.

Shares of Campbell's tumbled 7.1% on Mar. 11 after the company reported weaker-than-expected Q2 2026 results, with net sales falling 5% to $2.56 billion, adjusted EBIT dropping 24% to $282 million, and adjusted EPS declining 31% to $0.51. Investor sentiment was further hurt by significant weakness in the Snacks segment, where organic sales declined 6% and operating earnings plunged 39%, alongside storm-related shipment disruptions that reduced quarterly net sales, cut adjusted EBIT by roughly $14 million, and lowered adjusted EPS by approximately $0.04 per share.

The company also lowered its full-year fiscal 2026 guidance, projecting organic net sales to decline 2% to 1%, adjusted EBIT to fall 20% to 17%, and adjusted EPS to come in at $2.15 to $2.25, reflecting a more cautious outlook for the remainder of the year.

For the fiscal year ending in July 2026, analysts expect CPB’s adjusted EPS to decrease 26.3% year-over-year to $2.19. The company's earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing on another occasion.

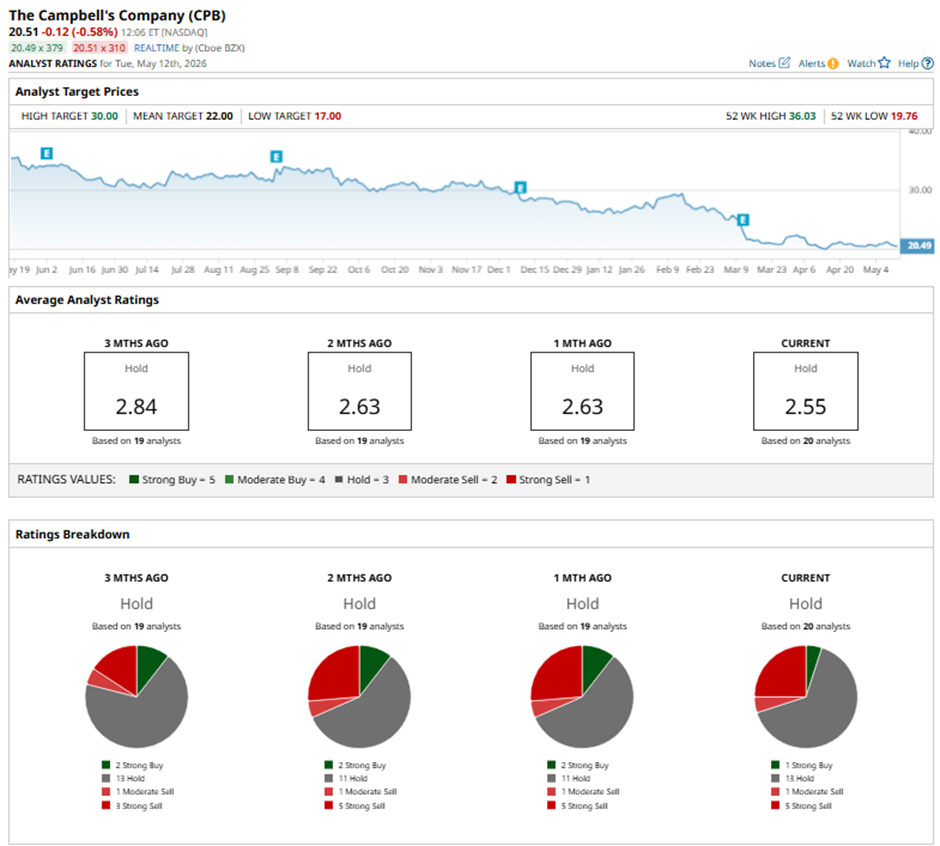

Among the 20 analysts covering the stock, the consensus rating is a “Hold.” That’s based on one “Strong Buy” rating, 13 “Holds,” one “Moderate Sell,” and five “Strong Sells.”

On Apr. 23, Morgan Stanley lowered its price target on Campbell's to $23 while maintaining an “Equal Weight” rating.

The mean price target of $22 represents a 7.3% premium to CPB’s current price levels. The Street-high price target of $30 suggests a 46.3% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)