/Carnival%20Corp_%20logo%20at%20night%20by-%20JHVEPhoto%20via%20Shutterstock.jpg)

With a market cap of $33.2 billion, Carnival Corporation & plc (CCL) is a global cruise company that provides leisure travel services across North America, Europe, Australia, and other international markets, operating through four key segments, including cruise operations and travel support services. It manages a diverse portfolio of cruise brands and also owns port destinations, hotels, railcars, and motorcoaches.

Shares of the Miami, Florida-based company have outpaced the broader market over the past 52 weeks. CCL stock has surged 40.2% over this time frame, while the broader S&P 500 Index ($SPX) has increased 29.1%. However, shares of the company are down 13.4% on a YTD basis, lagging behind SPX’s 4.3% rise.

Shares of the cruise operator have outperformed the State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) 18.6% return over the past 52 weeks.

Shares of Carnival Corporation fell 4.3% on Mar. 27 after the company cut its full-year adjusted EPS outlook to around $2.21 from a prior expectation of up to $2.48, reflecting pressure from rising fuel costs. The surge in oil prices, driven by geopolitical tensions linked to the Iran conflict, poses a major risk, with Carnival expecting more than $500 million in additional fuel expenses, only partly offset by roughly $150 million in operational improvements.

Despite strong Q1 2026 results and record bookings, investor sentiment weakened due to margin concerns, especially since Carnival typically does not hedge fuel, making it more exposed to cost volatility.

For the fiscal year ending in November 2026, analysts expect CCL’s adjusted EPS to decrease marginally year-over-year to $2.23. Nevertheless, the company's earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

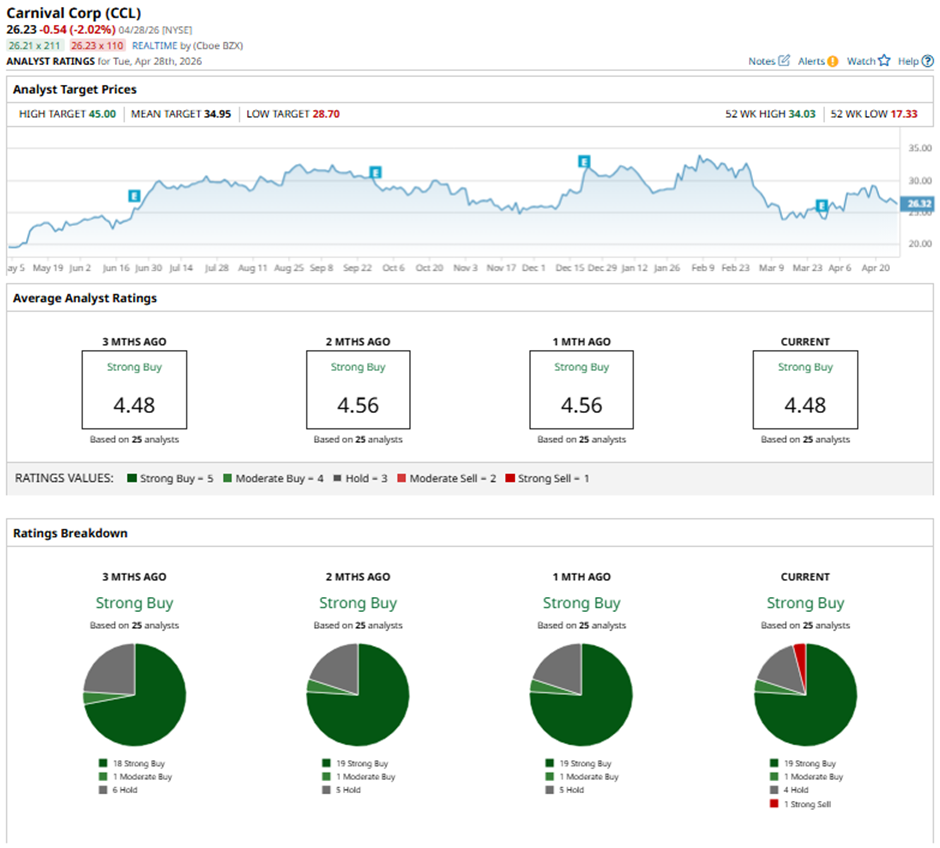

Among the 25 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on 19 “Strong Buy” ratings, one “Moderate Buy,” four “Holds,” and one “Strong Sell.”

On Apr. 15, Wells Fargo cut its price target on Carnival to $36 while maintaining an “Overweight” rating.

The mean price target of $34.95 represents a premium of 33.2% to CCL's current price. The Street-high price target of $45 suggests a 71.6% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)