/Advanced%20Micro%20Devices%20Inc_%20office%20sign-by%20Poetra_RH%20via%20Shutterstock.jpg)

Santa Clara, California-based Advanced Micro Devices, Inc. (AMD) produces semiconductor products and devices. Valued at $567 billion by market cap, the company offers products such as microprocessors, embedded microprocessors, chipsets, graphics, video and multimedia products and supplies it to third-party foundries, as well as provides assembling, testing, and packaging services.

Shares of this semiconductor giant have significantly outperformed the broader market over the past year. AMD has gained 246.3% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 29.8%. In 2026, AMD stock is up 56.3%, surpassing the SPX’s 4.8% rise on a YTD basis.

Zooming in further, AMD’s outperformance is also apparent compared to the iShares Semiconductor ETF (SOXX). The exchange-traded fund has gained about 146.4% over the past year. Moreover, AMD’s gains on a YTD basis outshine the ETF’s 51.2% returns over the same time frame.

AMD is well-positioned to ride the multiyear AI wave, gaining share in server and PC processors while expanding data center AI with Instinct GPUs and EPYC CPUs. Hyperscalers are scaling up AMD instances about 50% YoY, and partnerships with OpenAI and Meta Platforms, Inc. (META) signal massive demand. With Venice CPUs and MI500 GPUs coming, plus a full-stack AI push, AMD expects its data center segment to grow over 60% annually, targeting tens of billions in AI revenue by 2027.

For fiscal 2026, ending in December, analysts expect AMD’s EPS to grow 76.8% to $5.78 on a diluted basis. The company’s earnings surprise history is mixed. It beat or matched the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

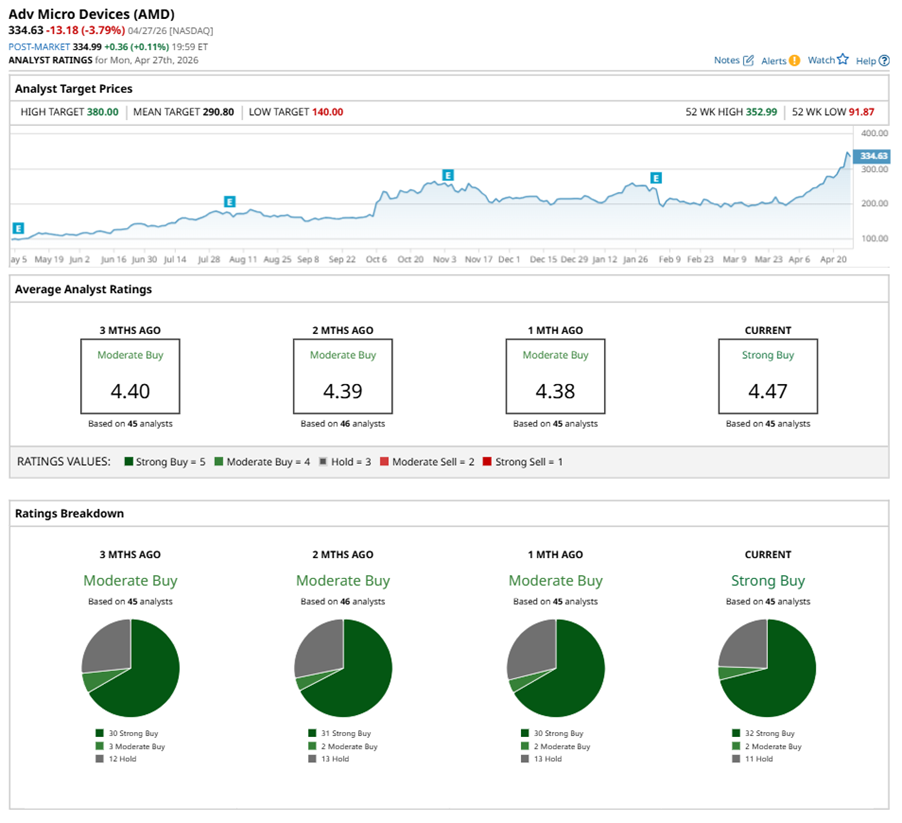

Among the 45 analysts covering AMD stock, the consensus is a “Strong Buy.” That’s based on 32 “Strong Buy” ratings, two “Moderate Buys,” and 11 “Holds.”

This configuration is more bullish than a month ago, with an overall “Moderate Buy” rating, consisting 30 analysts suggesting a “Strong Buy.”

On Apr. 27, Northland analyst Gus Richard downgraded AMD to a “Market Perform” rating with a $260 price target.

While AMD currently trades above its mean price target of $290.80, the Street-high price target of $380 suggests a 13.6% upside potential.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Robot%20arm%20industrial%20automation%20manufacturing%20by%20Eakrin%20via%20Adobe%20Stock.jpeg)