/Advanced%20Micro%20Devices%20Inc_%20logo%20on%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

Shares of Advanced Micro Devices (AMD) have moderated after a solid rally over the past year. Although the stock remains up about 157% over the last 12 months, it has retreated more than 18% from its all-time high of $267.08. Broader macroeconomic and geopolitical uncertainty continues to weigh on investor sentiment and may continue to keep the stock volatile in the short term. However, AMD’s outlook remains strong, suggesting that the recent pullback presents a buying opportunity for long-term investors.

AMD entered 2026 with solid operational momentum across its core businesses. Growth has been supported by the accelerating adoption of the company’s high-performance EPYC and Ryzen processors, as well as rapid expansion in its data center artificial intelligence (AI) segment.

Importantly, demand trends across AMD’s end markets remain favorable. The company is experiencing accelerating demand in data center infrastructure, personal computers, gaming platforms, and embedded systems. Overall, AMD is well-positioned to deliver strong growth in the coming quarters.

AMD Stock Poised for Big Gains

AMD appears well-positioned to benefit from a multiyear demand in high-performance computing driven by the rapid expansion of AI workloads. During its fourth-quarter conference call, management noted that AMD captured additional market share in both server and PC processors.

At the same time, AMD significantly expanded its data center AI operations, driven by increasing adoption of its Instinct accelerators and software platform among cloud providers, enterprises, and AI-focused customers. With differentiated products, strong customer partnerships, and growing operational scale, AMD is likely to capture a meaningful share of this expanding market in the coming quarters.

Looking ahead, AMD projects continued strong revenue growth and earnings expansion through 2026. Accelerating data center AI adoption and improving operating leverage across the business will drive its top and bottom lines at a solid pace.

Demand for AMD’s server processors is rising sharply. AMD’s EPYC CPUs are seeing strong adoption as emerging agentic AI applications and other advanced workloads rely on high-performance processors. At the same time, AMD’s AI accelerator portfolio, including AMD Instinct GPUs, is gaining traction in data centers.

Overall, AMD is well-positioned to benefit from increasing adoption of EPYC and Instinct processors, continued client market share gains, and improving performance in the embedded segment.

Over a longer time horizon, AMD aims to grow revenue at a CAGR exceeding 35% in the next three to five years while significantly expanding operating margins. Management also projects a considerable increase in its bottom line, with its annual earnings per share (EPS) expected to exceed $20 in the medium term, supported by growth across all business segments and the rapid scaling of its data center AI operations.

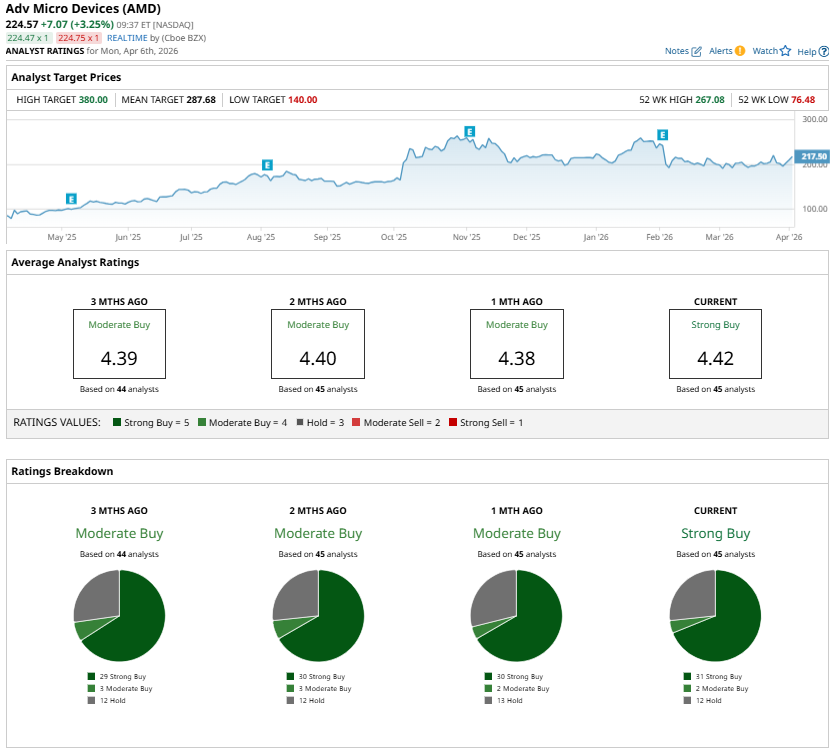

Wall Street Projects 28% Upside for AMD Stock

Wall Street analysts are optimistic about AMD stock and project notable upside over the next 12 months. AMD stock currently has a “Strong Buy” consensus rating among analysts, reflecting confidence in its growth prospects. Moreover, based on the average price target of $287.68, AMD shares could rise by approximately 28% over the next year.

Analysts’ bullish sentiment is supported by expectations of strong earnings growth in the coming years and compelling valuation. AMD stock trades at a forward price-to-earnings (P/E) ratio of about 37.3, which is attractive given the company’s solid earnings growth trajectory. Consensus estimates suggest that AMD’s earnings could grow by more than 72% in 2026 and by around 60% in 2027.

The Bottom Line

AMD’s recent pullback comes after a strong rally, but the company’s long-term growth story remains intact. Rising demand for AI infrastructure, strong adoption of EPYC and Instinct processors, and continued market share gains position AMD for solid earnings expansion in the coming years. While short-term volatility may persist, the company’s growth outlook and analyst upside potential suggest the dip is an attractive entry point for investors.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)