Valued at $10.2 billion by market cap, The J. M. Smucker Company (SJM) is a prominent consumer packaged goods (CPG) company specializing in branded food and beverage products. Headquartered in Orrville, Ohio, the company has built a portfolio of well-known household brands across coffee, spreads, snacks, and pet food.The leading consumer packaged goods company is expected to announce its fiscal fourth-quarter earnings for 2026 in the near term.

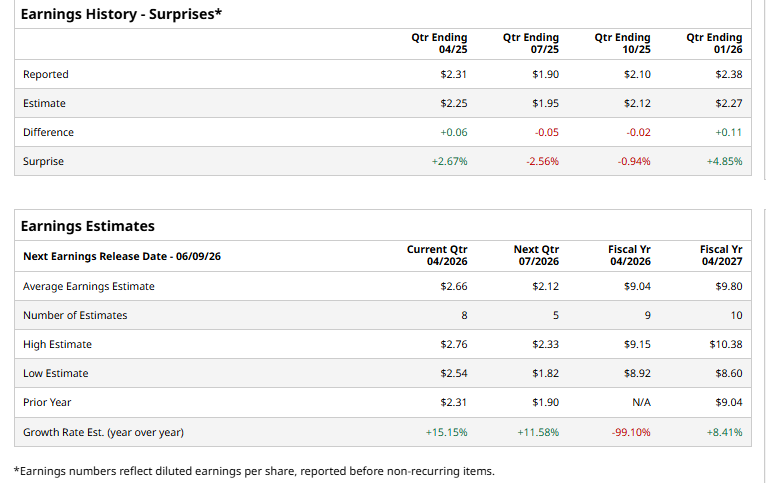

Ahead of the event, analysts expect SJM to report a profit of $2.66 per share on a diluted basis, up 15.2% from $2.31 per share in the year-ago quarter. The company beat the consensus estimates in two of the last four quarters while missing the forecast on two other occasions.

For the current year, analysts expect SJM to report EPS of $9.04, down 99.1% from fiscal 2025. However, its EPS is expected to rise 8.4% year over year to $9.80 in fiscal 2027.

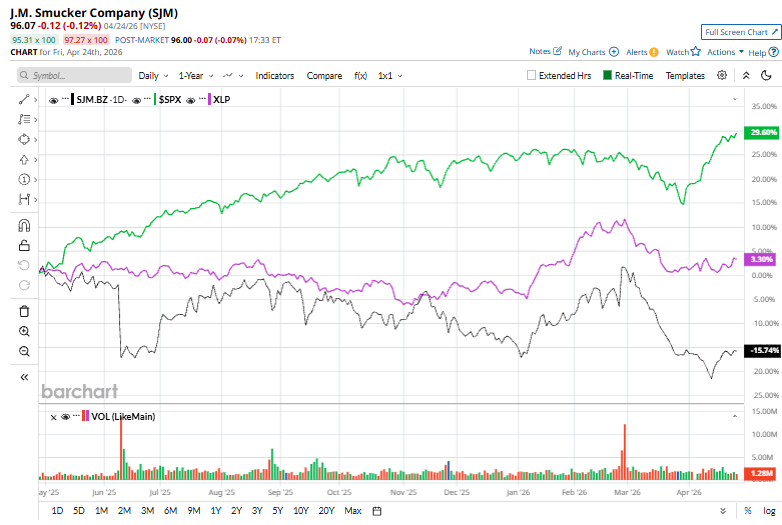

SJM stock has plunged 17% over the past 52 weeks, underperforming the S&P 500 Index’s ($SPX) 30.6% gains and the State Street Consumer Staples Select Sector SPDR Fund’s (XLP) 2.7% returns over the same time frame.

J. M. Smucker gave investors something to cheer about on Apr. 16, announcing a $1.10 per share dividend, a steady signal of confidence in its cash flows. The payout, sourced from capital surplus, is scheduled for June 1, 2026, with shareholders on record as of May 15 set to benefit.

Beyond returns, Smucker also outlined its upcoming Annual Shareholder Meeting, which will take place virtually on August 12, 2026, at 1:00 p.m. ET. The market responded positively to the update, with SJM shares rising 1.7% in the following session, reflecting investor approval of both the dividend commitment and continued shareholder engagement.

Analysts’ consensus opinion on SJM stock is moderately bullish, with a “Moderate Buy” rating overall. Out of 19 analysts covering the stock, eight advise a “Strong Buy” rating, two suggest a “Moderate Buy,” and nine give a “Hold.” SJM’s average analyst price target is $119.50, indicating a potential upside of 24.4% from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)