/Ross%20Stores%2C%20Inc_%20outside%20sign%20by-%20Ken%20Wolter%20via%20Shutterstock.jpg)

With a market cap of $72.9 billion, Ross Stores, Inc. (ROST) is a major U.S. off-price retailer headquartered in Dublin, California, best known for its Ross Dress for Less and dd’s DISCOUNTS chains. The company offers apparel, accessories, footwear, and home fashions products.

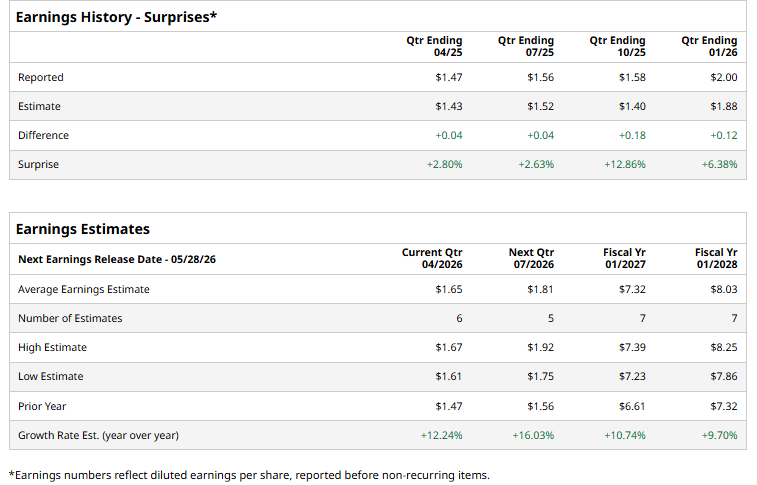

ROST is expected to report its Q1 earnings soon. Ahead of the event, analysts expect ROST to report a profit of $1.65 per share, up 12.2% from a profit of $1.47 per share reported in the year-ago quarter. It has exceeded analysts' earnings estimates in each of the past four quarters, which is notable.

For the current year ending in January 2027, analysts expect ROST to report EPS of $7.32, up 10.7% from $6.61 in fiscal 2026. Moreover, its EPS is likely to rise 9.7% year over year to $8.03 in FY2028.

Over the past year, ROST shares surged 64.2%, significantly outperforming the S&P 500 Index’s ($SPX) 32.2% gains and the Consumer Discretionary Select Sector SPDR Fund’s (XLY) 23.7% returns over the same time frame.

On Mar. 9, ROSS shares rose marginally following the company’s announcement of the first phase of its fiscal 2026 expansion strategy. The retailer unveiled the opening of 17 new stores, comprising 13 Ross Dress for Less and four dd’s DISCOUNTS locations, across 11 states, signaling the start of a broader plan to add approximately 110 stores this year, representing around 5% unit growth.

The expansion builds on strong new store performance in 2025, with Ross extending its footprint across the Mountain, Midwest, and Northeast regions while strengthening its presence in key Sunbelt markets and expanding dd’s into both core and new territories. The update reinforced investor confidence in the company’s long-term growth outlook, including its vision to scale to 2,900 Ross and 700 dd’s DISCOUNTS locations nationwide.

The consensus opinion on ROST stock is highly upbeat, with an overall “Strong Buy” rating. Out of the 18 analysts covering the stock, 14 recommend a “Strong Buy” and four recommend a “Hold.” Its mean price target of $231.93 indicates a robust 2.2% upside potential from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)