/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

After taking a steep hit earlier this year amid fears that artificial intelligence (AI) startup Anthropic could upend traditional software players, the sector is roaring back to life, and investors are taking notice once again. The shift in sentiment has been quite strong. For context, the iShares Expanded Tech-Software Sector ETF (IGV) has surged nearly 9% in just the past five days, outperforming nearly every major leadership ETF and even eclipsing the iShares Semiconductor ETF (SOXX), which climbed 5.41% over the same stretch.

And riding this renewed wave of momentum is Oracle Corporation (ORCL), whose stock has skyrocketed 12.54% in just five days, making it one of the standout winners of the broader software resurgence. The recent rally in Oracle shares isn’t happening in a vacuum. It’s being fueled by a series of aggressive, forward-looking moves in AI infrastructure and energy strategy. For instance, on April 13, the software giant announced a major expansion of its partnership with Bloom Energy (BE), securing up to 2.8 gigawatts of Bloom’s fuel cell capacity to support power-hungry AI data centers.

And just days later, on April 16, the company announced plans to expand its multicloud networking capabilities, enabling enterprise-grade, high-performance connectivity between Oracle Cloud Infrastructure (OCI) and Amazon’s (AMZN) Amazon Web Services (AWS). So, with these developments unfolding alongside a broader industry rebound, should investors continue piling up Oracle shares?

About Oracle Stock

Oracle Corporation has spent decades quietly becoming one of the most essential players in the global tech ecosystem. Founded in 1977 and headquartered in Austin, Texas, the company built its reputation on powering the world’s most critical data systems, especially through its dominance in relational database management systems (RDBMS). Over time, Oracle has transformed into a full-scale enterprise technology provider.

The company’s portfolio now stretches from Oracle Cloud and cloud infrastructure to AI-powered business applications and the globally recognized Java platform. A major focus today is Oracle Cloud Infrastructure (OCI) and its autonomous database, both designed to streamline operations while enhancing performance, scalability, and security. Oracle’s technology sits at the core of operations for major institutions, from banks to healthcare networks, where reliability and data integrity are non-negotiable.

This deep enterprise integration has helped the company remain a dominant force in ERP and mission-critical systems. By 2025, Oracle’s scale spoke for itself, ranking 66th on the Forbes Global 2000 list and generating approximately $57 billion in annual revenue, underscoring its enduring relevance in an increasingly data-driven world. The company’s market capitalization presently stands at about $503.5 billion.

Despite a shaky start to the year, with Oracle shares still down 10.14% in 2026 amid broader industry weakness, the latest rebound has been hard to ignore. Driven by company-specific developments and a wider software sector recovery, the stock has rallied an impressive 12.54% in just the last five trading sessions, comfortably outpacing the broader S&P 500 Index ($SPX), which managed a more modest 3.12% gain over the same period.

Inside Oracle’s Q3 Earnings Report

Oracle delivered a defining moment in its fiscal third-quarter 2026 earnings report, released on March 10, underscoring its rapid transformation from a legacy software provider into a full-fledged AI powerhouse. The market reaction was immediate, and shares jumped nearly 9.2% in the very next trading session. Management didn’t hold back, calling the results “exceptional,” as Oracle marked its first time in over 15 years where both organic revenue and non-GAAP earnings grew by 20% or more.

Total quarterly revenue climbed to $17.19 billion, up 22% year-over-year (YOY) and comfortably ahead of analyst expectations of $16.89 billion. The clear standout was Oracle Cloud Infrastructure (OCI), where revenue surged an impressive 84% to $4.9 billion, fueled by relentless demand for AI training capacity. Oracle is increasingly carving out its niche as a faster, more flexible alternative to larger competitors for enterprises deploying large language models (LLMs).

When combined with Cloud Applications (SaaS), Oracle’s total cloud segment has now crossed a major milestone, generating $8.9 billion in revenue, up 44% YOY and accounting for more than half of the company’s total revenue. Perhaps the most eye-catching metric was Remaining Performance Obligation (RPO), which skyrocketed 325% to a staggering $553 billion.

This massive backlog of contracted future revenue is largely tied to long-term AI infrastructure deals with hyperscalers and large enterprises, offering strong visibility into Oracle’s growth runway. Profitability followed suit, with non-GAAP earnings per share rising 21% to $1.79, well ahead of the consensus estimate of $1.70.

On the capital front, Oracle moved aggressively to fund its expansion. In February, the company announced plans to raise up to $50 billion through a mix of debt and equity financing, while stating it does not expect to issue additional bonds beyond this amount in calendar 2026.

Within days, Oracle secured $30 billion via investment-grade bonds and mandatory convertible preferred stock, backed by a record order book that was heavily oversubscribed. Looking ahead, Oracle’s growth trajectory remains firmly intact. For the fiscal fourth quarter of 2026, the company expects revenue growth in the range of 19% to 21%, with non-GAAP EPS projected to grow between 15% and 17%, landing between $1.96 and $2.00.

For the full fiscal year 2026, Oracle reaffirmed its outlook of $67 billion in revenue and $50 billion in capital expenditures. And signaling even bigger ambitions, the company has raised its fiscal 2027 revenue guidance to $90 billion.

How Are Analysts Viewing Oracle Stock?

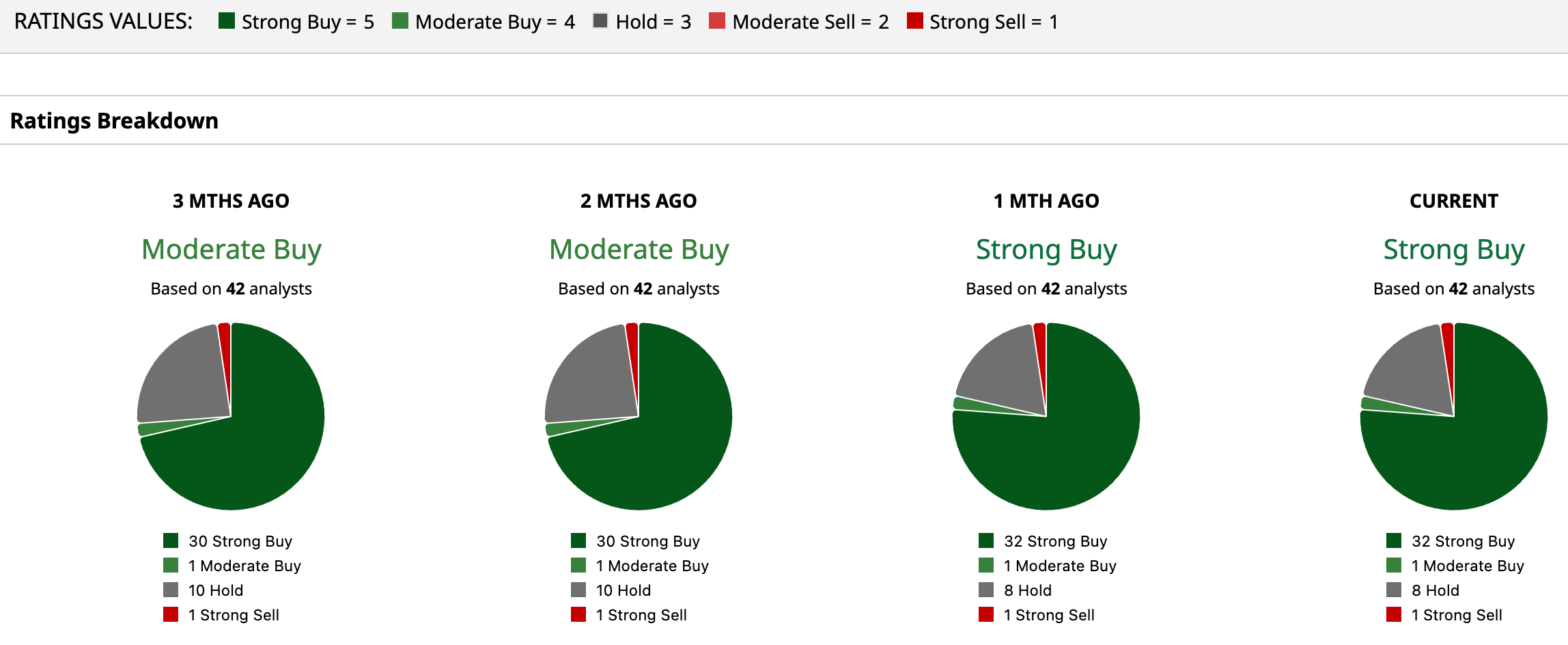

Overall, Wall Street continues to show strong conviction in Oracle, with the stock earning a “Strong Buy” consensus rating. Of the 42 analysts covering the name, an overwhelming 32 recommend “Strong Buy,” one suggests a “Moderate Buy,” eight remain cautious with “Hold,” and just one holds a bearish “Strong Sell” view.

Backing up this bullish sentiment is the significant upside analysts still see ahead. The average price target of $253.21 implies a 44.2% potential gain from current levels, while the Street-high target of $400 points to an even more ambitious 127.8% upside, signaling that, in the eyes of many, Oracle’s growth story may still have plenty of room to unfold.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Quantum%20Computing/A%20concept%20image%20showing%20a%20ray%20of%20light%20passing%20through%20cyberspace_%20Image%20by%20metamorworks%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)