/Paycom%20Software%20Inc%20logo%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

With a market cap of $5.9 billion, Oklahoma-based Paycom Software, Inc. (PAYC) is a cloud-based human capital management (HCM) provider that offers an end-to-end platform for payroll, HR, and employee management. The company offers an integrated platform that manages the entire employee life cycle, from recruitment and onboarding to payroll, benefits, and retirement.

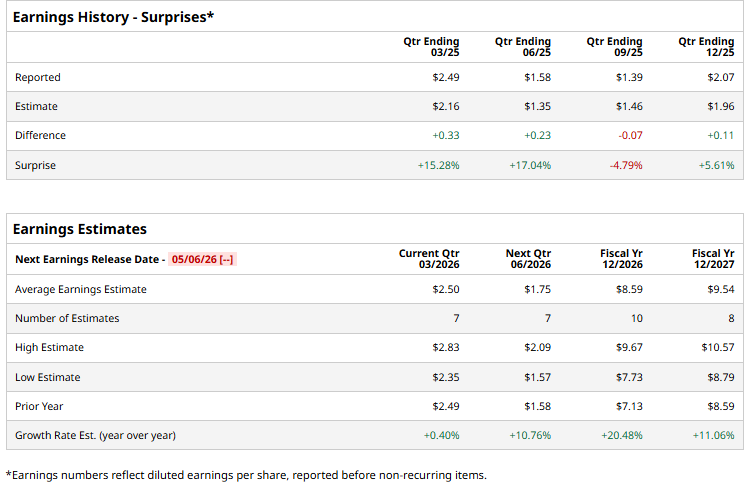

The company is expected to release its Q1 2026 earnings soon. Ahead of the event, analysts expect the company to generate a profit of $2.50 per share on a diluted basis, up marginally from $2.49 per share in the year-ago quarter. The company has surpassed Wall Street’s EPS estimates in three of its last four quarters, while missing on one occasion.

For the current year, analysts expect the company to report EPS of $8.59, up 20.5% from $7.13 in fiscal 2025. However, its EPS is expected to rise 11.1% year over year to $9.54 in fiscal 2027.

Shares of PAYC have declined 21.6% over the past 52 weeks, underperforming the S&P 500 Index’s ($SPX) 19.3% rise and the Technology Select Sector SPDR ETF’s (XLK) 29% return during the same time frame.

On Apr. 9, Paycom Software shares fell about 3.2% amid a broader SaaS sell-off triggered by renewed Middle East tensions and rising concerns that advances in autonomous AI, such as Anthropic’s Managed Agents, could disrupt traditional software models.

Analysts’ consensus opinion on the stock is somewhat bullish, with a “Moderate Buy” rating overall. Among the 21 analysts covering the stock, six are recommending a “Strong Buy,” and the remaining 15 analysts suggest a “Hold” for the stock. PAYC’s average analyst price target is $154.56, indicating an upside of 23.1% from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)