One of the most common metrics used when trading options is the Implied Volatility Percentile.

IV Percentile is a measure of implied volatility where current implied volatility is compared to the range of implied volatilities in this past.

This comparison is made on the same stock.

For example, Apple’s IV percentile takes the current implied volatility and compares it to the past implied volatilities Apple has had.

This is then made into a percentage ranging from 0-100%.

A percentage of zero would depict a stock is currently at the lowest level of implied volatility it has been during the lookback period.

In contrast, an IV percentile of 100% illustrates that the stock is trading at its highest level of implied volatility.

As discussed previously, an upcoming earnings announcement can mean a stock has an elevated level of implied volatility. To get a true picture of stocks with a high implied volatility percentile, we can use the Stock Screener.

Using The Stock Screener To Find High Volatility Stocks

Despite the VIX index dropping to its lowest level in 6 months, there are still some stocks showing high implied volatility.

Using the Stock Screener, we can set the following filters to find stocks with a high implied volatility percentile.

- Total Call Volume 2,000

- Market Cap greater than 60 billion

- IV Percentile greater than 70%

This screener gives us the following stocks ranked from highest IV Percentile to lowest:

Activision Blizzard (ATVI)

Tesla (TSLA)

Intel (INTC)

Amazon (AMZN)

Verizon (VZ)

Walt Disney Company (DIS)

Gilead Sciences (GILD)

AT&T (T)

International Business Machines (IBM)

Netflix (NFLX)

Alphabet (GOOGL)

Here is the full list of stock with high IV Percentile.

How To Use IV Percentile

As a general rule, when implied volatility percentile is high, it’s better to focus on short volatility trades such as iron condors, short straddles and strangles.

It also makes sense to compare a stock’s current IV Percentile to the market in general. If all stocks are showing high IV Percentile, then there might not be much of an edge in selling volatility on a specific stock. But, if general market IV percentile is low, that could be a good time to sell overpriced volatility in some of the names above.

It’s also a good idea to keep an eye on the upcoming earnings dates as stock can make big moves following earnings announcements.

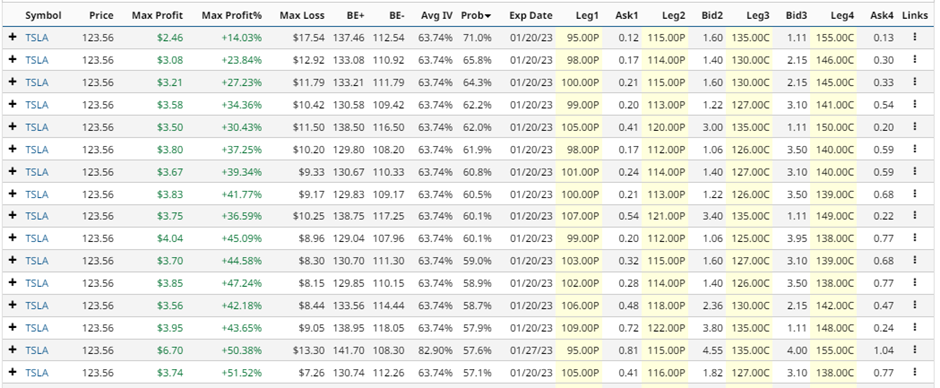

Iron Condor Screener

Let’s run an iron condor screener for Tesla and analyze the results. Keep in mind that Tesla is due to report earnings on January 25th.

Let’s look at the first line item.

Using the January 20 expiry, the trade would involve selling the 115 put and buying the 95 put. Then on the calls, selling the 135 call and buying the 155 call.

The price for the condor is $2.46 which means the trader would receive $246 into their account. The maximum risk is $1,754 for a total profit potential of 14.03% with a probability of 71.0%.

The profit zone ranges between 112.54 and 137.46. This can be calculated by taking the short strikes and adding or subtracting the premium received.

Please remember that options are risky, and investors can lose 100% of their investment. This article is for education purposes only and not a trade recommendation. Remember to always do your own due diligence and consult your financial advisor before making any investment decisions.

More Stock Market News from Barchart

- Stocks Higher as Bond Yields Tumble on Slowing U.S. Inflation

- Easing U.S. Inflation Pressures Boost Case for Slower Fed Rate Hikes

- Stocks Rally After As-Expected CPI Report

- Options Traders Suggest a Little Patience is Necessary for AbbVie (ABBV)

On the date of publication, Gavin McMaster did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)