When energy stocks start running, it is easy for the story to become all about oil prices and headlines.

But for investors, the better question is which companies actually have the numbers to back up the move. That's what makes ConocoPhillips and EOG Resources worth putting side by side. Both are well-known oil and gas producers, both have posted strong gains this year, and both have reasons to stay on investors’ radar.

The question is: Which one looks more compelling today?

ConocoPhillips (COP)

Let’s start with ConocoPhillips, the larger and more diversified company in this matchup. It is one of the biggest independent oil and gas producers in the world, with operations across major energy-producing regions. Put simply, ConocoPhillips makes money by finding and producing oil and natural gas on a large scale.

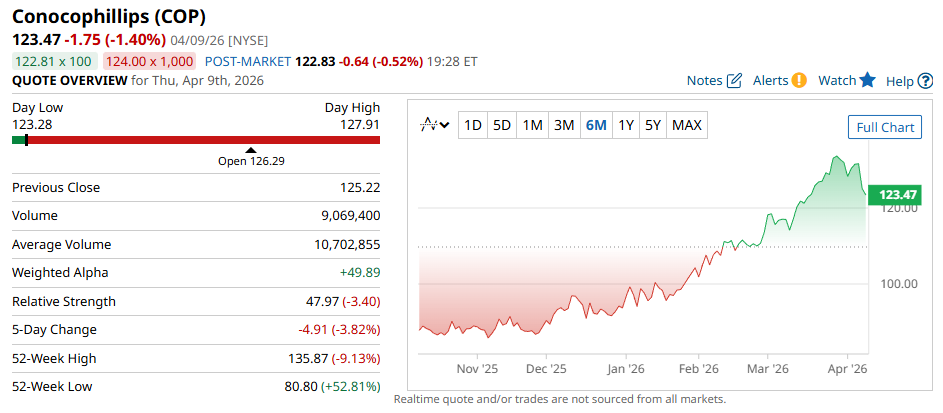

COP stock is up 32% year to date, trading around $123.

EOG Resources (EOG)

Then there is EOG Resources, the smaller, more focused of the two. It is a major oil and gas producer best known for its shale operations in the United States. EOG makes money the same way as ConocoPhillips, but it is often seen as the more focused and efficient operator of the two.

Currently trading at around $136, EOG stock is up 30% year-to-date.

So far, these two companies look equal, at least in terms of performance. Now, let’s dive deeper.

How do they make money: COP vs EOG

ConocoPhillips is built around the upstream side of the energy business, meaning it makes money by exploring for, producing, transporting, and marketing oil and natural gas. Its advantage is scale. The company has a broad portfolio spanning multiple major producing regions, providing geographic diversification and greater exposure to certain asset types.

Meanwhile, EOG Resources also operates on the upstream side, but its model is more focused on generating strong returns from a core portfolio of oil and gas assets, particularly in U.S. shale. Rather than relying on global breadth, EOG is better known for running a tighter operation and getting more from the wells it develops.

While both companies make money from producing oil and gas, ConocoPhillips offers more scale and diversification, while EOG is the more focused operator.

Financial health

Continuing, let’s look at what the latest quarterly figures say.

| Metric | ConocoPhillips | EOG Resources |

| Sales | $14.19 billion | $5.64 billion |

| Net Income | $1.44 billion | $701 million |

| Operating Cash Flow | $19.8 billion | $10 billion |

| Price-to-Earnings (Forward) | 18x | 11x |

The first thing that stands out is scale. ConocoPhillips is operating on a much larger level, with $14.19 billion in sales in the latest quarter, compared with $5.64 billion for EOG. The same goes for earnings, where ConocoPhillips reported $1.44 billion in net income, while EOG reported $701 million.

Cash generation also leans in ConocoPhillips’ favor. Its operating cash flow came in at $19.8 billion, versus $10 billion for EOG. That figure basically shows how much cash the business is bringing in from its normal operations, and for energy companies, it matters because it gives a better sense of how much financial room they have to fund spending, support dividends, or return cash to shareholders, which is critical, especially during these times of uncertainties in the industry.

Valuation tells a different story. EOG has a forward P/E of 11, while ConocoPhillips sits at 18. For context, the broader energy sector average is 23. The P/E ratio compares a stock’s price with its future earnings, so it is one of the easier ways to judge whether investors are paying a lot or a little for each dollar of profit. On that basis, both stocks are still trading below the sector average, but EOG looks cheaper.

So while ConocoPhillips has the clear advantage in size, revenue, profit, and cash flow, EOG makes its case on valuation. In other words, COP looks like a bigger brother, while EOG looks more attractively priced.

Dividends, dividends, dividends

Of course, for many investors, the appeal here is not just capital upside. Energy stocks like these can also attract attention for their ability to generate cash and return some of it to shareholders.

ConocoPhillips pays a forward annual dividend of $3.36 per share, which yields about 2.7%. Its payout ratio is 51.18%, meaning it returns a little over half of its earnings as dividends.

EOG, meanwhile, pays $4.08 annually, yielding around 3%. Its payout ratio is 38.7%, which is lower than ConocoPhillips’.

Both look solid for income, but EOG appears to be the stronger dividend play based on yield and payout ratio.

What does Wall Street say?

Both stocks are still in Wall Street’s good graces.

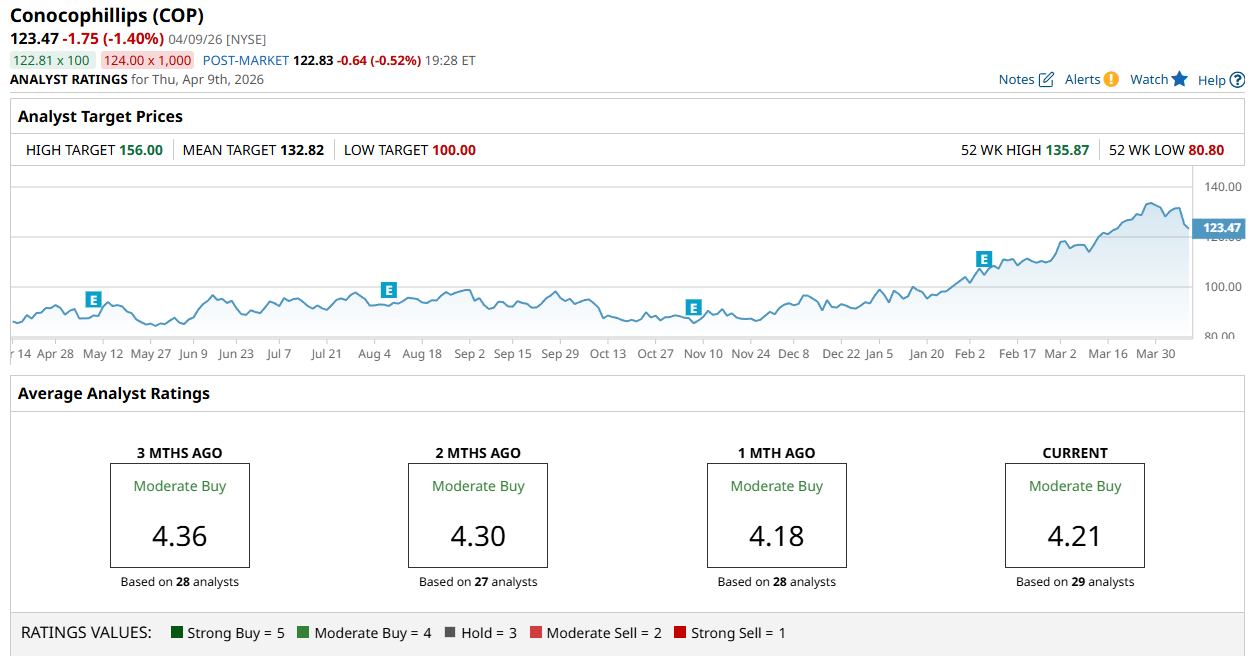

ConocoPhillips stock, according to a consensus of 29 analysts, has a “Moderate Buy” rating with a score of 4.21 out of 5. Its mean and high target prices suggest a potential upside of between 8% to 26% over the next year.

Meanwhile, a consensus among 34 analysts rates EOG stock a "Moderate Buy" rating, though with a score of 3.82 out of 5. The mean and high target prices imply potential upside of between 10% and 35%.

Meanwhile, a consensus among 34 analysts rates EOG stock a "Moderate Buy" rating, though with a score of 3.82 out of 5. The mean and high target prices imply potential upside of between 10% and 35%.

Verdict

With all that, it is fair to say that ConocoPhillips and EOG are both solid energy investments.

So while both names remain well-liked by analysts, ConocoPhillips has the stronger overall rating, while EOG offers a higher yield, a lower payout ratio (which could suggest more room to grow the dividend in the future), and a wider upside range.

From here, it really comes down to preference. ConocoPhillips looks stronger in terms of size and overall financial muscle, while EOG stands out as the less expensive option that comes with a slightly better yield.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Super%20Micro%20Computer%20Inc%20HQ%20photo-by%20Tada%20Images%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_logo%20and%20website-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)