Investors took a victory lap yesterday -- the S&P 500 gained 2.5%, delivering a rare gap up -- but the future is far from clear.

The fact that the ceasefire agreed to by the U.S., Iran, and Israel is already hanging on by a thread, the uncertainty should have most investors in a neutral stance right now.

On Monday, MarketWatch contributor Barbara Kollmeyer discussed why the S&P 500 could drop to 6000 before it reaches a new high.

“The bottom line is that many investors are looking past Middle East tensions, assuming stocks will swiftly return to prior highs, but ‘the reality is we are lacking the fully oversold conditions that typically accompany a breach of the 200 DMA,’ he said,” Kollmeyer referring to BTIG chief market technician Jonathan Krinsky.

Prior to yesterday’s move, the index had traded below its 200-day moving average (MA) since March 19. Krinsky suggests that as long as the index doesn’t close above 6,800, it could drop to 6,150 or lower.

Further, the last time the index traded below its 20-day MA was from February to May 2025. Before that, it was September to October 2024.

So, the gap up yesterday could be good, or it could be a head fake on its way down. Fortunately, I’m not a market timer.

In yesterday’s unusual options activity, RTX (RTX), maker of Pratt & Whitney jet engines, had the most unusually active option on the day. Its May 1 $220 call had a Vol/OI (volume-to-open-interest) ratio of 217.22, more than double Rocket Lab’s (RKLB) Jan. 21/2028 $85 call at 92.93.

Whether you are big into options or not, RTX’s call is a no-brainer. Here’s why.

The Option in Question

As you can see, the call had a volume of 23,400 yesterday, 217.22 times the open interest. There wasn’t one massive trade, but a bunch of medium-sized bets -- 10 of 500 or more contracts and 41 between 100 and 500 contracts. That tells you interest was broad among institutional investors. But there were also many trades of one or two calls by retail investors.

The net trade sentiment for RTX options on Wednesday was bullish at $678,100, according to Barchart options flow data. Many of the bullish trades at the ask price occurred from 2:50 p.m. ET to the close at 4.

That’s not to say there weren’t trades at the bid (Covered Calls). I counted 26 out of 137, while there were 83 at the ask, with the remaining 28 somewhere in between.

I’ll assume that most were bullish.

Why Be Bullish About RTX?

It's safe to say RTX is a momentum stock. Its shares are up 11% year-to-date, 59% over the past year, and 160% over the past five years, with most of the gains in the past two years.

As for specific reasons, the war in Iran is an obvious tailwind. The world is getting more dangerous by the day, and RTX’s products help countries protect themselves.

The company finished 2025 with a backlog of $268 billion, with commercial business accounting for 60% and defense business for the remaining 40%, spread across its three operating segments: Collins Aerospace, Pratt & Whitney, and Raytheon.

Based on its 2025 sales of $88.63 billion, the backlog will take three years to complete. There’s no shortage of business, which is a nice problem to have.

As I mentioned, RTX has three operating segments, averaging sales of $30.39 billion, a nod to the company’s diversification. It’s one thing to have significant revenue; it’s another to have it spread so evenly. That’s really attractive to long-term investors.

Another positive is the company’s guidance for 2026.

In the year ahead, RTX expects sales of $92.5 billion at the midpoint of its guidance, about 4.4% higher than in 2025, with organic sales of 5.5%. On the bottom line, it expects earnings per share of $6.70, while analysts are calling for $6.81 in 2026 and $7.50 in 2027. Its stock trades at 27.2 times the 2027 estimate, which is reasonable given the strength of its business.

In 2026, it expects free cash flow to grow by 7% to $8.50 billion. Based on an enterprise value of $308.29 billion, it has a free cash flow yield of 2.8%. It’s definitely not a bargain.

Lastly, analysts tend to like it. Of the 25 covering it, 16 rate it a Buy, with a target price of $215.43, slightly above its current share price.

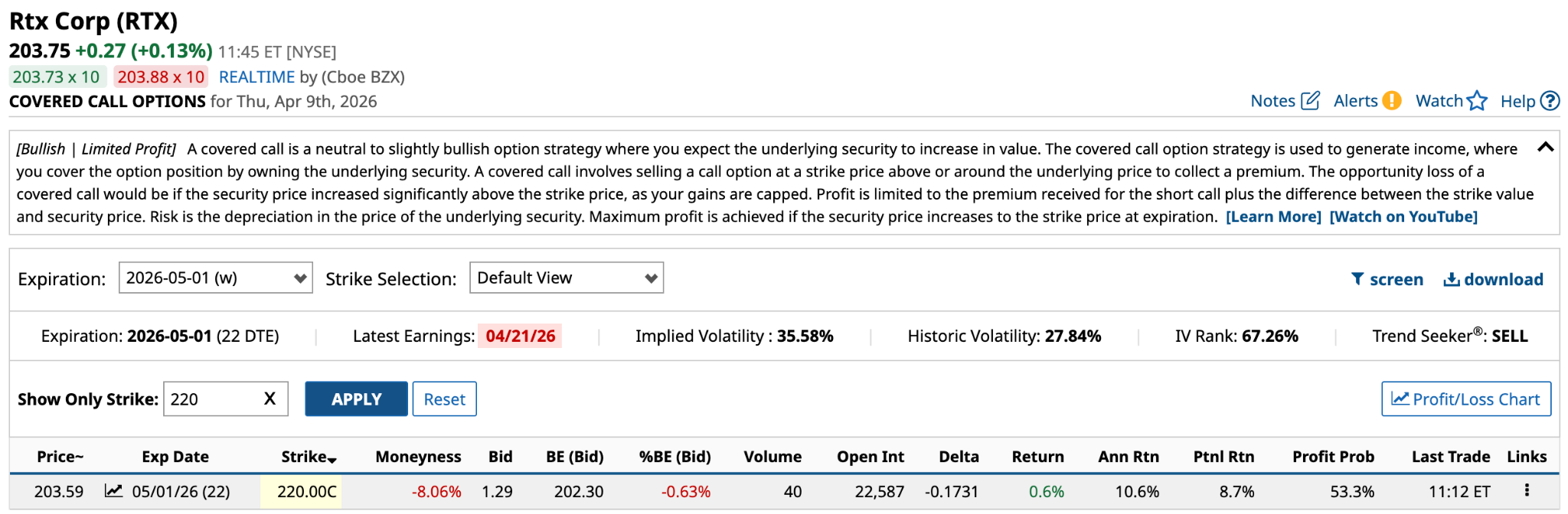

Why Be Bullish About RTX May 1 $220 Call

The information above is the latest trading information for the May 1 $220 call as I write this late Thursday morning. The ask price is higher at $1.55, but the share price is about the same as yesterday’s close. The call’s breakeven is about 8.82% above the current share price.

The first thing you might focus on is the 13.97% probability of profit. That’s not high. Further, the expected move between now and May 1 is $16.44 (8.07%), leaving you $1.52 shy of moving into profit territory.

Yes, but based on the 0.1766 delta, you can double your money by selling to close the call prior to expiration if it appreciates by $8.77 (4.3%). So, you’ve risked just $155 or 0.8% of the share price, while having an escape valve available to get your money back and then some.

Assuming the share price goes to $212.36 [$203.59 share price + $8.77 in appreciation], and you close the position, your annualized return would be 1,659% [100% return * 365 / 22 DTE].

On the other hand, if you’ve owned shares for a long time, selling the $220 call for income with a covered call would also be an attractive play. Of course, you’d have to be willing to sell your shares to the buyer should the share price be above $220 at expiration. However, if I didn’t already have gains in the stock, I’d probably avoid this play. The risk/reward isn’t high enough.

Either way, it’s a no-brainer in my books.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)