/Super%20Micro%20Computer%20Inc%20HQ%20photo-by%20Tada%20Images%20via%20Shutterstock.jpg)

Super Micro Computer (SMCI) is no stranger to controversy. But its latest challenge, an indictment of three people who were allegedly tied to export-control violations, has investors asking a pointed question: Is this a manageable speed bump or a sign of deeper trouble?

The company's response to the March 2026 indictment has been swift and unusually transparent. It launched an independent board-led investigation within weeks. The question is whether that's enough to restore confidence in SMCI stock.

What the Indictment Means for SMCI Stock

On March 19, 2026, the U.S. Attorney's Office for the Southern District of New York unsealed an indictment against three individuals who were linked to Supermicro at the time, alleging an export-control conspiracy.

Crucially, Supermicro itself is not named as a defendant.

The three individuals charged are Yih-Shyan "Wally" Liaw, the company's former senior vice president of business development and a then-sitting board member; Ruei-Tsang "Steven" Chang, a Taiwan-based sales manager; and Ting-Wei "Willy" Sun, a contractor. All three no longer have any relationship with the company.

Liaw resigned from the board on March 20. The same day, Supermicro promoted DeAnna Luna, a trade compliance veteran with more than two decades of experience at companies like Intel (INTC) and Teledyne Technologies (TDY), to acting chief compliance officer.

CEO Charles Liang called the alleged conduct by those individuals a betrayal of the company's mission. "It appears that Supermicro has been a victim of the elaborate schemes orchestrated by these individuals, which deceived both federal authorities and our internal compliance team," Liang said in a letter to stakeholders.

The Independent Probe Matters

On April 7, 2026, Supermicro confirmed it has launched an independent investigation led by two of its board's independent directors: Lead Independent Director Scott Angel and Audit Committee Chair Tally Liu.

- Angel spent nearly four decades at Deloitte, including 25 years as an audit partner.

- Liu brings 25 years of experience as a certified public accountant.

- The pair retained Munger, Tolles & Olson LLP, a top-tier law firm with five decades of experience leading independent investigations, as well as forensic accounting firm AlixPartners.

- All findings will be reported to the four other independent board members and not to management.

In 2024, SMCI delayed its annual report and changed auditors amid an accounting scandal, while investors learned that governance optics don't always match reality. This time, the probe's design, which includes outside counsel, forensic accountants, and direct board reporting, looks credible on paper.

SMCI Continues to Grow Rapidly

Even as the legal clouds gathered, Supermicro posted record fiscal second-quarter 2026 revenue of $12.7 billion, up 123% year-over-year (YoY), blowing past its own guidance of $10 billion to $11 billion.

Artificial intelligence GPU platforms drove more than 90% of that revenue. One large data center customer alone accounted for 63% of total revenue in the quarter, a concentration that has some analysts nervous.

Gross margins remain a soft spot. The non-GAAP gross margin came in at 6.4% in Q2, down from 9.5% in the prior quarter. Liang attributed the compression to customer mix, expedited transportation costs, component shortages, and tariff pressure. The good news: management guided for at least $12.3 billion in Q3 revenue and raised its full-year fiscal 2026 guidance to at least $40 billion.

Liang also pointed to the company's growing Data Center Building Block Solutions, or DCBBS, product line, a higher-margin infrastructure offering, as a key lever for improving profitability going forward.

DCBBS contributed roughly 4% of profit in the first half of fiscal 2026. Management expects to reach double-digit contribution by the end of calendar year 2026.

Should You Buy SMCI Stock Right Now?

The bull case for SMCI stock is real.

- Demand for AI infrastructure is exploding.

- Supermicro has a first-mover edge in liquid cooling and full data center solutions.

- Revenue is growing at a triple-digit clip.

- And the company is not a defendant in the indictment.

But the bear case has teeth too.

- Gross margins are thin and narrowing.

- Customer concentration is extreme.

- The company has a recent history of accounting and compliance problems.

- And the outcome of the investigation is genuinely unknown.

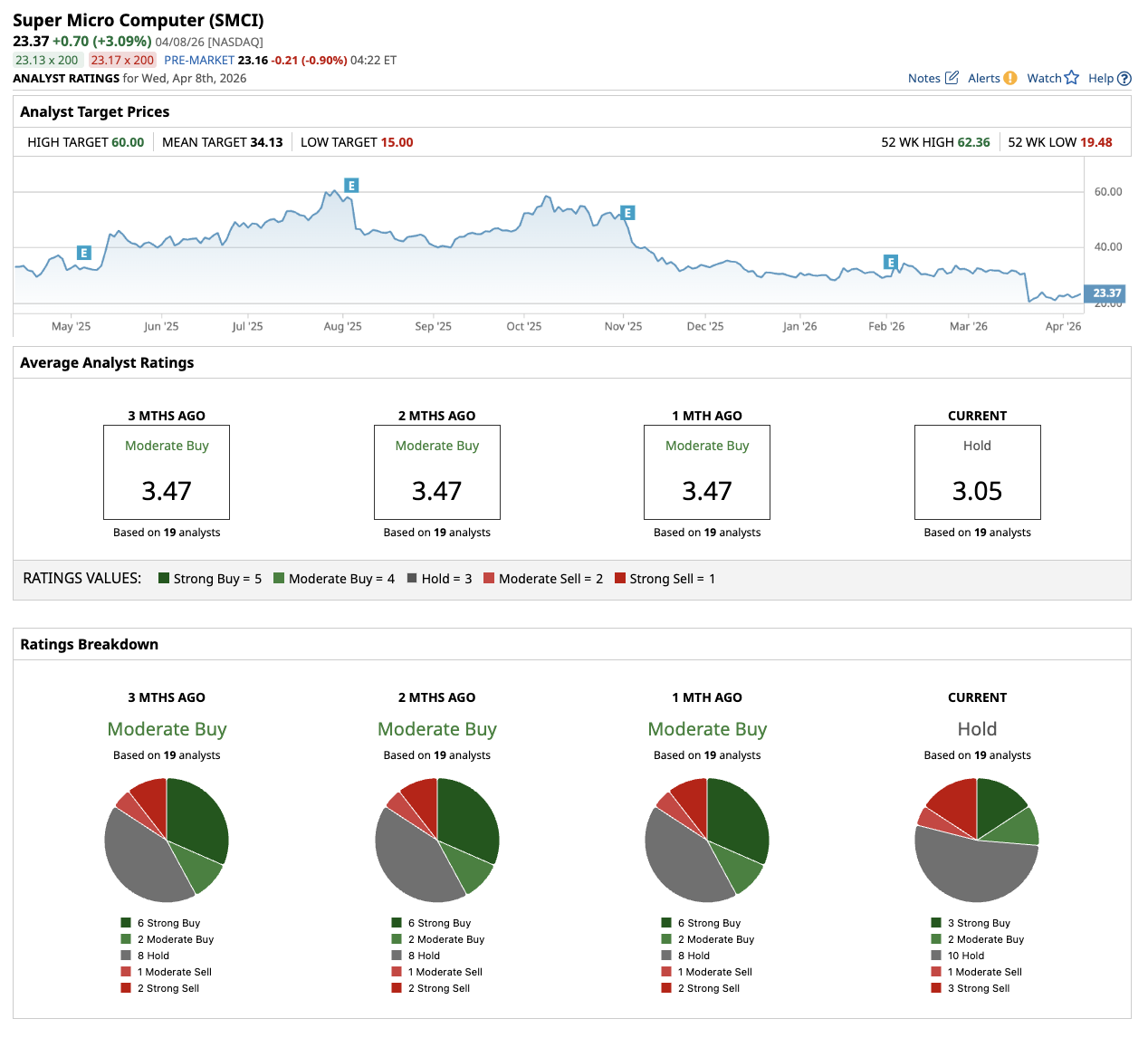

Out of the 19 analysts covering SMCI stock, three recommend “Strong Buy,” two recommend “Moderate Buy,” 10 recommend “Hold,” one recommends “Moderate Sell,” and three recommend “Strong Sell.” The average SMCI stock price target is $34.13, above the current price of about $23.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20and%20sign%20on%20headquarters%20by%20Michael%20Vi%20via%20Shutterstock.jpg)

/Gen%20Digital%20Inc%20logo%20on%20building-by%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

/EV%20in%20showroom%20by%20Robert%20Way%20via%20Shutterstock.jpg)