/Micron%20Technology%20Inc_logo%20and%20website-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

Micron Technology (MU) is a global leader in innovative memory and storage solutions. As one of the world's largest semiconductor companies, Micron specializes in DRAM and NAND technologies that are fundamental to modern computing. The company has pivoted aggressively toward enterprise and data center markets, recently announcing its exit from the consumer-facing Crucial brand to focus on high-growth AI infrastructure.

By producing industry-leading High Bandwidth Memory (HBM) and low-power server modules, Micron provides the essential "fuel" for large language models (LLM), positioning itself as a primary beneficiary of the global generative AI spending cycle.

About MU Stock

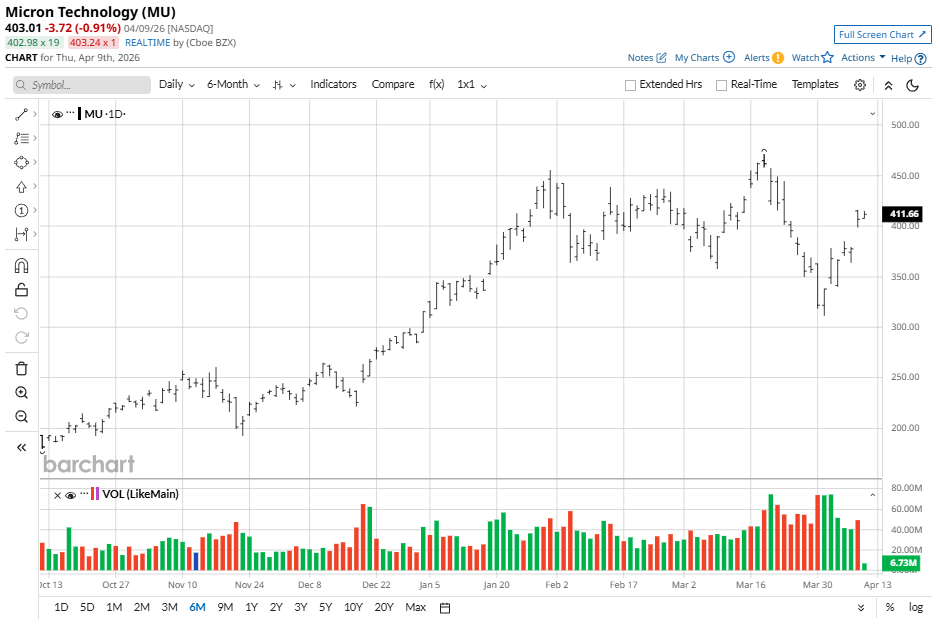

Micron stock has been a standout performer, surging over 230% since late 2025 and recently touching all-time highs near $471. Investors have flocked to the name as memory prices for DRAM and NAND are projected to rise significantly throughout the year. However, the stock is now down 13% from its mid-March peak of $471.

In comparison to the S&P 500 Information Technology Index ($SRIT), Micron has delivered massive outperformance during the 2026 bull run. While the broader tech benchmark dominated by software and cloud giants has benefited from AI interest, Micron’s triple-digit gains have significantly outpaced the index's growth.

This divergence is fueled by the structural shift in the semiconductor cycle, where Micron's hardware has become a primary bottleneck for AI development. Unlike the more diversified, software-heavy components of the Information Tech index, Micron’s performance is tightly coupled with the supply-demand dynamics of the memory market, allowing it to capture outsized gains as global shortages persist.

Micron's Stellar Results

Micron delivered a knockout performance for its second quarter ending February 26, 2026, reporting record revenue of $23.86 billion. This represented a staggering 196% year-over-year (YoY) increase, shattering analyst expectations of $19.19 billion. The company achieved a record non-GAAP diluted EPS of $12.20, a massive beat against the $8.79 consensus.

This exceptional profitability was driven by a sharp expansion in non-GAAP gross margins to 74.9%, as the product mix shifted toward high-margin AI assets like HBM3E. Operating cash flow reached $11.9 billion, supporting a 30% increase in the company's quarterly dividend.

The quarter marked a turning point where memory transitioned from a commodity to a "strategic asset." Revenue in the Cloud Memory Business Unit doubled, while the Automotive and Mobile units saw gains of 49% and 63%, respectively.

Management provided "mind-blowing" guidance for the third quarter, projecting $33.5 billion in revenue, which would exceed the full-year revenue of any year in company history before 2024. With $14.6 billion in liquidity and ongoing investments in advanced wafer fabrication plants in Singapore, Micron is scaling its HBM4 production to meet an insatiable demand for AI compute platforms, cementing its role as a foundational pillar of the semiconductor industry.

Micron Stock Pops on Ceasefire

Micron saw its stock skyrocket 7.7% on Wednesday as investors rushed back into the memory trade following news of a two-week U.S.-Israel-Iran ceasefire. The potential reopening of the Strait of Hormuz has signaled a "green light" for momentum trades, particularly for the high-end chips essential to AI infrastructure.

The rally is fueled by a massive surge in hardware pricing. Analysts at UBS report that memory prices jumped nearly 95% in the first quarter, with another 40% increase expected in the second quarter. KeyBanc echoed this optimism, projecting price hikes of up to 50% for DRAM and NAND components. While hardware giants like Dell (DELL) and HP (HPQ) are raising their own prices to offset these costs, demand for Micron’s products shows no signs of slowing.

Experts believe this cycle could remain profitable until late 2027. Furthermore, a shift toward long-term supply agreements may help Micron avoid the "boom-and-bust" crashes typical of past chip cycles, creating a more stable and predictable growth path as the company scales its AI-ready hardware.

Should You Bet on MU Stock?

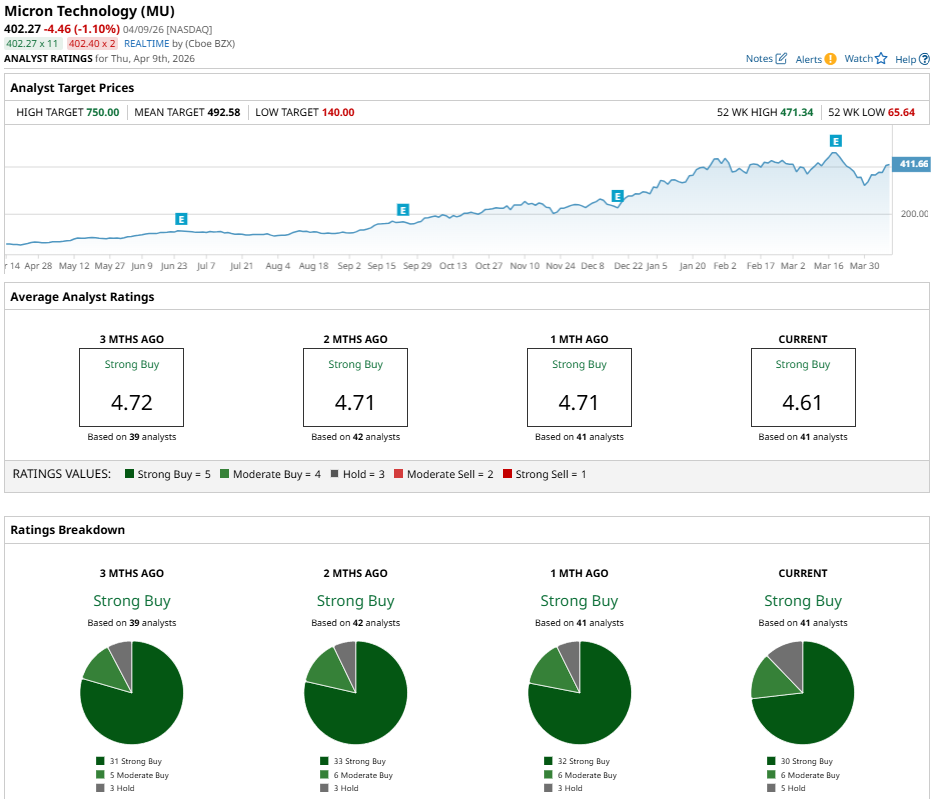

The recent ceasefire has removed a significant geopolitical overhang, clearing the path for Micron to capitalize on record-breaking memory price hikes. Currently, MU stock maintains a "Strong Buy" consensus from 41 analysts, including 30 "Strong Buy" and six "Moderate Buy" ratings, and five give it a "Hold" rating. With a mean price target of $492.58, Micron offers a projected 22% upside from its current price.

Supported by structural AI demand and a shift toward stable, long-term supply agreements, Micron remains a premier growth play for investors targeting the heart of the semiconductor super-cycle.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)