/Tesla%20Inc%20tesla%20by-%20Iv-olga%20via%20Shutterstock.jpg)

Tesla (TSLA) has evolved far beyond its origins as an electric vehicle (EV) pioneer into a dominant force in physical artificial intelligence (AI) and sustainable energy. Founded in 2003, the company integrates a vast ecosystem ranging from high-performance EVs like the Model 3 to utility-scale energy storage solutions like the Megapack. By leveraging its massive real-world fleet data and proprietary Dojo supercomputing clusters, Tesla aims to solve generalized autonomy and accelerate the world's transition to a fully automated, sustainable energy economy.

Investors have something to watch for with TSLA stock this month, as the company is due to report its first-quarter earnings results on April 22. Let's take a closer look as Tesla gears up for its latest earnings release.

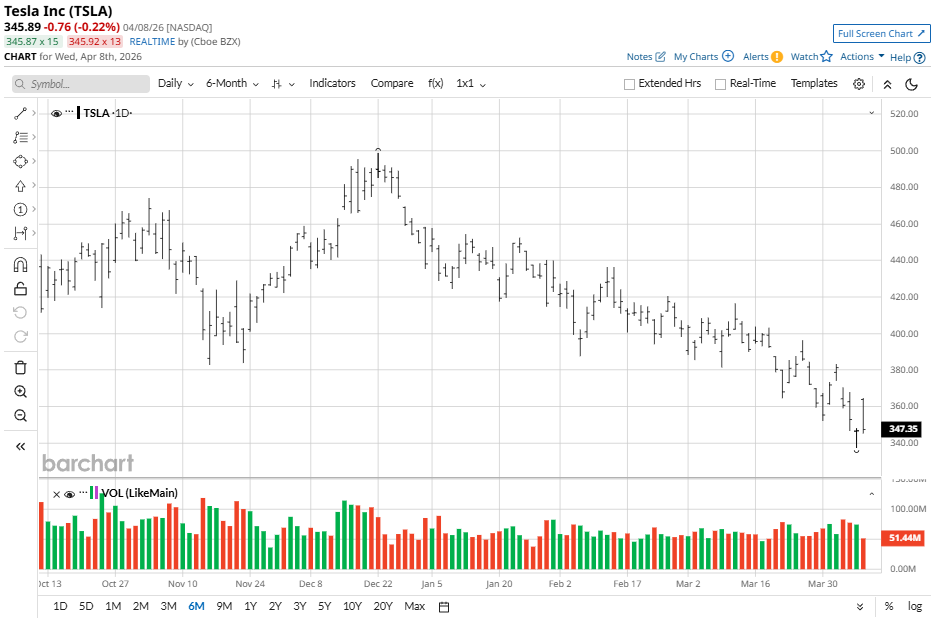

Tesla Is Facing a Rough 2026

Tesla stock has had a challenging start to the year following a robust 2025. The stock has experienced a sharp 25% decline year-to-date (YTD), significantly underperforming the broader market. This pullback is largely attributed to a "transition year" narrative, as investors weigh decelerating automotive delivery growth against the massive capital expenditures required for AI infrastructure.

In comparison to the Nasdaq 100 Index ($IUXX), Tesla has been a notable laggard during Q1 2026. While the tech-heavy Nasdaq 100 has maintained relative stability despite broader macroeconomic headwinds — anchored by diversified software and semiconductor giants — Tesla's valuation is increasingly tied to "prove-it" milestones in robotics and Full Self-Driving (FSD) technology.

Tesla's Q4 Results and Q1 Deliveries

Tesla concluded fiscal 2025 with a resilient Q4, reporting revenue of $24.9 billion, surpassing analyst estimates of $24.7 billion. Despite pricing pressures in the automotive sector, the company delivered non-GAAP EPS of $0.50, beating the consensus estimate of $0.44.

A major highlight was the Energy Generation & Storage segment, which saw revenue grow 25% year-over-year (YOY) as deployments reached record levels. On a GAAP basis, the company posted net income of $840 million, maintaining its streak of profitability while generating $1.4 billion in free cash flow to fund its ambitious AI and robotics roadmap.

Looking to the first quarter, Tesla recently reported Q1 2026 deliveries of 358,023 vehicles. That fell slightly short of the 365,000 vehicle consensus estimate but still reflected a 6% YOY increase. The company is scheduled to release its full Q1 2026 financial results on April 22, 2026.

With more than $44 billion in total cash as of Q4, Tesla is aggressively scaling its "unboxed" manufacturing process for the Cybercab. While near-term margins remain under pressure due to R&D spending, the company’s focus is squarely on its evolution into a high-margin, software-driven "physical AI" powerhouse.

Tesla Earnings Preview

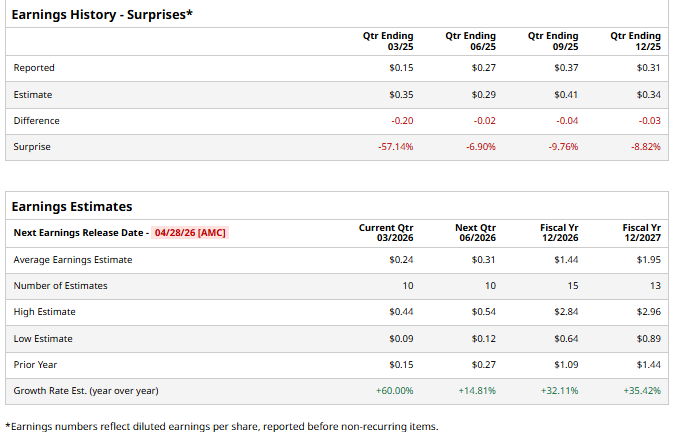

Tesla is set to report its Q1 2026 results soon, with analysts placing the average earnings estimate at $0.24 per share. While this represents a 60% YOY increase compared to the prior year’s $0.15, expectations vary widely. The high EPS estimate is $0.44 while the low is $0.09 per share.

The outlook for full-year fiscal 2026 remains optimistic as the company pivots toward autonomy. Analysts project average EPS of $1.42, reflecting robust growth of 30% YOY from the $1.09 earned in 2025. For fiscal 2026, the Street-high estimate reaches $2.84 while the low is marked at $0.64. Investors are weighing the scaling of the Cybercab against the capital-intensive ramp-up of new AI infrastructure and robotics production.

Should You Buy TSLA Stock?

Tesla’s upcoming earnings preview highlights a period of significant transition, with analysts forecasting a significant YOY increase in Q1 earnings as the company pivots toward its robotaxi future. TSLA stock currently earns a consensus "Hold" rating based on 43 analysts with coverage, featuring a wide split of 15 "Strong Buy" ratings, two “Moderate Buy” ratings, 16 “Hold” ratings, and 10 "Strong Sell" ratings. With a mean price target of $403.47, TSLA stock offers potential upside of nearly 18% from current levels.

The long-term robotics and AI thesis remains compelling for Tesla. However, investors may face near-term volatility as the market weighs high capital expenditures against cooling EV delivery growth.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)