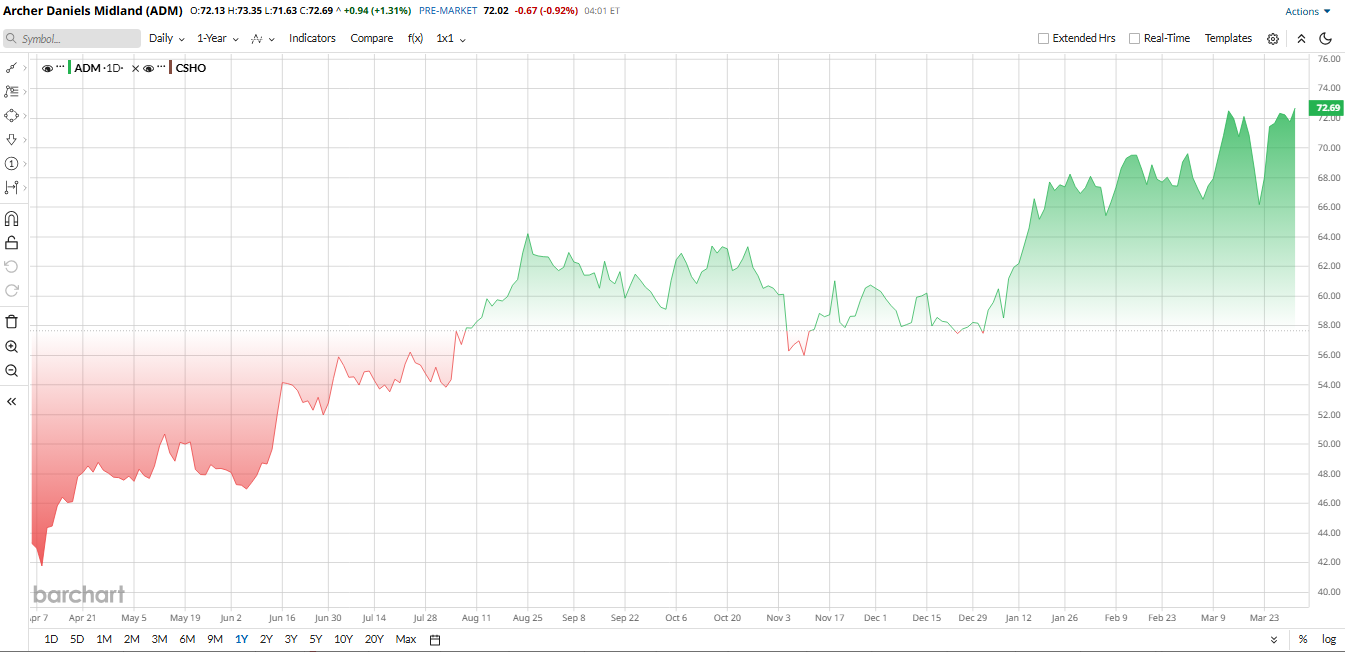

Agribusiness giants have had a rough couple of months. Grain prices and biofuel margins have softened, and trade disputes have kept international volumes choppy. Stocks like Archer Daniels Midland (ADM) have been under pressure amid rising costs and policy uncertainty. But on March 30, one technical newsletter caught the attention of investors when CappThesis founder and President Frank Cappelleri flagged ADM stock as breaking out of a multi-month base with a measured upside near $90. Cappelleri thinks ADM stock could rally by more than 20% from today's levels. His insight helped spark a bounce in shares, even as the S&P 500 Index ($SPX) itself neared oversold levels.

For traders who like chart-driven setups, this kind of call is hard to ignore.

Why This Setup Matters for ADM Stock

Archer Daniels Midland is one of the biggest crop processors in the world. The company handles grain, oilseeds, animal feed, ethanol, sweeteners, and nutrition ingredients, making it a core part of the global food and fuel supply chain.

That scale is part of what makes the stock interesting here. ADM is not a small, speculative name that needs perfect conditions to move higher. It is a large, established business with a broad footprint, and when the chart turns constructive, investors tend to pay attention.

Despite the choppy environment, as commodity margins have weakened, China's demand has been softer, and policy questions around biofuels continue to hang over the sector. Shares of ADM, however, have managed to deliver decent returns of 28% in 2026.

ADM stock trades at around 16.8 times forward earnings, but that figure sits below the broader food-processor peer group average. ADM also changes hands at about 14 times EV/EBITDA and roughly 0.44 times sales. These are not the kind of numbers that suggest a market pricing in a lot of growth, which is part of the appeal.

CappThesis Catalysts

On March 30, technical traders perked up. CappThesis highlighted ADM’s chart as “breaking out,” implying the stock could see a substantial move higher.

CappThesis is basically saying ADM looks like it may be waking up after spending months moving sideways. In technical terms, a breakout happens when a stock pushes above a range that has acted like a ceiling for a while, which can attract momentum buyers.

That matters because ADM stock has been stuck in a weak stretch, so a move above the base can signal that sellers may be losing control. If the stock can hold those higher levels instead of quickly slipping back, traders often see it as a sign the trend may be shifting.

Cappelleri’s target near $90 suggests the chart could still have room to run from around $70. But the move needs follow-through, meaning the stock has to stay strong rather than fade after the first bounce.

The Business Still Faces Real Pressure

Archer Daniels Midland’s latest quarter showed mixed results. Revenue for the fourth quarter of 2025 came in at $18.56 billion, down roughly 14% from a year earlier and below Wall Street expectations. Adjusted EPS fell to $0.87 from $1.14 a year earlier. Net income also declined, slipping to about $456 million from $567 million in the same period a year ago.

The weakest area was Ag Services and Oilseeds, where operating profit fell about 31% as crush margins narrowed and exports slowed. Carbohydrate Solutions held up somewhat better, helped by ethanol exports, while Nutrition was mixed as some categories offset weaker results elsewhere.

Even so, ADM continued to generate solid cash. Operating cash before working capital was $2.7 billion for 2025, while net cash from operations reached $5.5 billion. The company also ended the year with adjusted debt to EBITDA at about 1.9 times, which leaves the balance sheet in reasonable shape.

Management Is Trying to Reset the Story

ADM is not standing still. Management has been working on portfolio changes and cost reductions, and the company recently moved ahead with a joint venture involving its U.S. feed mills and Alltech. That deal is expected to streamline the business and free up resources for higher-return areas.

CEO Juan Luciano has also stressed that the company is focusing on portfolio optimization, plant efficiency, and targeted cost cuts. ADM expects to deliver between $500 million and $750 million in cost savings over the next three to five years.

The company also raised its quarterly dividend by 2%, marking another year of steady payouts. That helps reinforce ADM stock’s appeal to income-focused investors, even while the business works through a tougher operating backdrop.

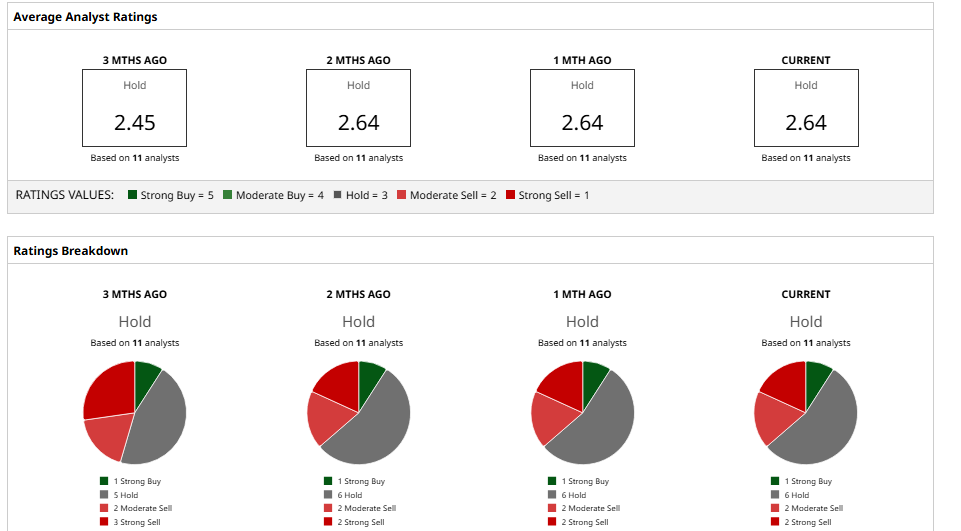

What Do Analysts Think of ADM Stock?

Wall Street is still cautious overall. The consensus from 11 analysts covering ADM stock is a “Hold” rating. The stock also currently trades above the mean price target of $61.50 as well as the Street-high target of $70, which shows a possible signal of a pullback.

With that said, in my opinion, ADM is not a clean growth story here, and the fundamentals are still uneven. But that is exactly why the technical setup has caught attention. If the breakout pattern holds and policy or margin trends improve, shares could have room to run.

For now, the case is simple: ADM looks cheap, cash-generative, and technically interesting. In a market short on conviction, that is enough to put it back on traders’ radars.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)