As war-driven disruptions gripped global oil markets, a sharp supply shock rippled through the system, turning crude into one of the most sought-after assets and lifting energy stocks across the board. At the heart of the turmoil was the Strait of Hormuz, a critical artery for 20% of global oil, where Iran’s restrictions tightened flows and forced a rapid reshaping of trade routes.

With fewer cargoes available in benchmark markets and pricing mechanisms shifting almost overnight, volatility surged, creating a rare window for a dominant player to seize control. And that’s exactly where TotalEnergies SE (TTE) made its move. Leveraging its deep-rooted infrastructure in the Middle East, TotalEnergies executed a masterclass in market timing, locking in nearly every available May-loading cargo from the UAE and Oman, around 70 shipments last month, just as supply tightened and competition thinned.

As buyers scrambled for alternative grades that bypassed the disrupted route, prices surged dramatically, with Dubai crude oil skyrocketing from roughly $70 to nearly $170 per barrel, far outpacing global benchmarks like Brent. In fact, TotalEnergies paired its aggressive physical purchases with derivatives like futures, options, and swaps, allowing it to hedge risks while doubling down on rising prices.

With less oil being traded and markets more vulnerable to large positions, the company effectively dominated the space, turning geopolitical chaos into a strategic advantage. The payoff was enormous, with trading profits reportedly exceeding $1 billion, cementing TotalEnergies as one of the biggest winners in a market defined by disruption. So, does this strategic win make TTE a stock worth buying now?

About TotalEnergies Stock

France-based TotalEnergies operates as a global integrated energy player with a footprint spanning roughly 120 countries, reflecting both its scale and diversification. The company’s portfolio stretches across traditional fuels like oil and biofuels to natural gas, biogas, and emerging areas such as low-carbon hydrogen, renewables, and electricity, positioning it at the intersection of legacy energy and the ongoing transition.

Backed by a workforce of over 100,000 employees, TotalEnergies has been steadily reshaping its operations, placing increasing emphasis on sustainability while balancing the realities of global energy demand. Currently valued at $218.14 billion by market capitalization, TotalEnergies is riding a powerful wave of momentum, fueled by surging trading profits amid escalating geopolitical tensions in the Middle East, factors that have broadly lifted energy stocks.

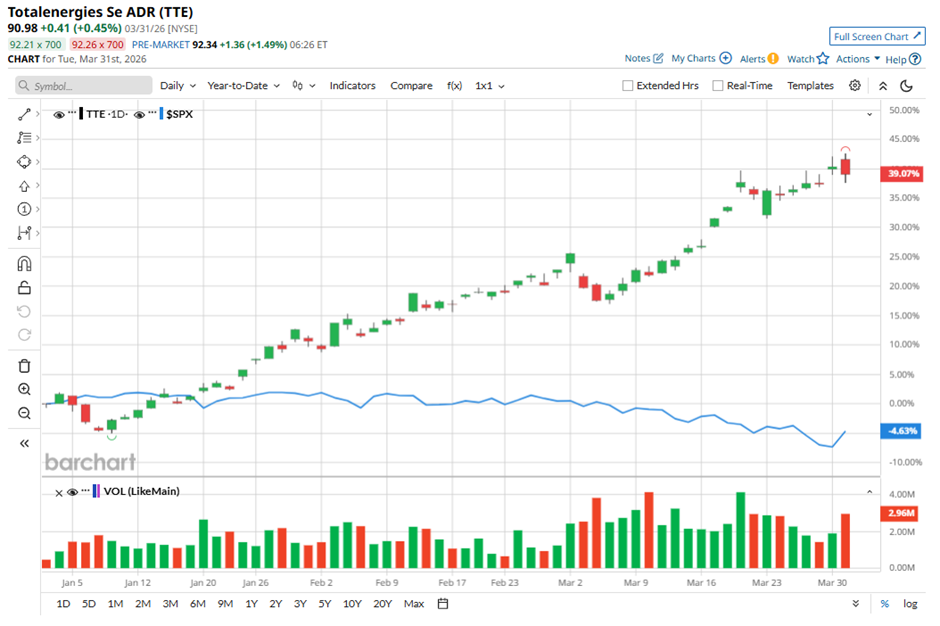

Moreover, the company’s recent bold, highly strategic move in the Dubai crude market, which reportedly delivered over $1 billion in gains, has been a major catalyst behind the rally in TTE shares. After delivering a strong 39% return in 2025, TotalEnergies has carried that momentum into 2026, with shares soaring another 37.24% year-to-date (YTD), an eye-catching rally that underscores the strength of its recent positioning.

In fact, the stock recently climbed to an all-time high of $93.29 on Mar. 31 and has slipped just 3.8% since then. For perspective, the broader S&P 500 Index ($SPX) has risen 16.7% over the past year but is down 3.95% so far in 2026, highlighting just how significantly TotalEnergies has outperformed the market.

Inside TotalEnergies’ Latest Financial Performance

In mid-February, TotalEnergies delivered its fiscal 2025 fourth-quarter and full-year results, showcasing a resilient performance even in a challenging environment marked by a 15% drop in oil prices. For the full year, the company generated an adjusted net income of $15.6 billion and a strong cash flow of $27.8 billion, while posting a return on average capital employed of 12.6%, the best among major oil players for the fourth consecutive year.

In the fourth quarter, revenue slipped 2.5% year-over-year (YOY) to $45.93 billion but still comfortably beat expectations of $32.10 billion, while adjusted earnings came in at $1.73 per share, just shy of the $1.80 estimate. The quarter’s strength was underpinned by exceptional cost discipline, with operating costs held at just $5 per barrel, one of the lowest in the industry.

At the same time, TotalEnergies accelerated high-margin projects in Brazil and the Gulf of Mexico, helping drive a robust quarterly cash flow of $7.2 billion in the fourth quarter alone. This operational efficiency translated into a strong 13.6% return on equity, reinforcing its position as one of the most profitable players in the global energy space.

Strategically, the company continued to execute a balanced and disciplined growth plan, investing $17.1 billion in 2025. Of this, 37% was directed toward new oil and gas projects, while around $3.5 billion was allocated to low-carbon energy initiatives, including nearly $3 billion in electricity. It ended the year with a gearing ratio of just 15%, highlighting a solid and well-managed balance sheet.

Backed by strong cash generation and financial stability despite an uncertain macro backdrop, the board has proposed a final 2025 dividend of €0.85 per share, bringing the full-year payout to €3.40 per share, up 5.6% from 2024. This comes alongside $7.5 billion in share buybacks executed in 2025, with management reaffirming a $3 billion to $6 billion buyback plan for 2026.

Looking ahead, TotalEnergies is targeting 5% overall energy production (oil, gas and electricity) growth in fiscal 2026 while continuing to advance its sustainability goals, including a 70% reduction in methane emissions compared to 2020 levels.

How Are Analysts Viewing TotalEnergies Stock?

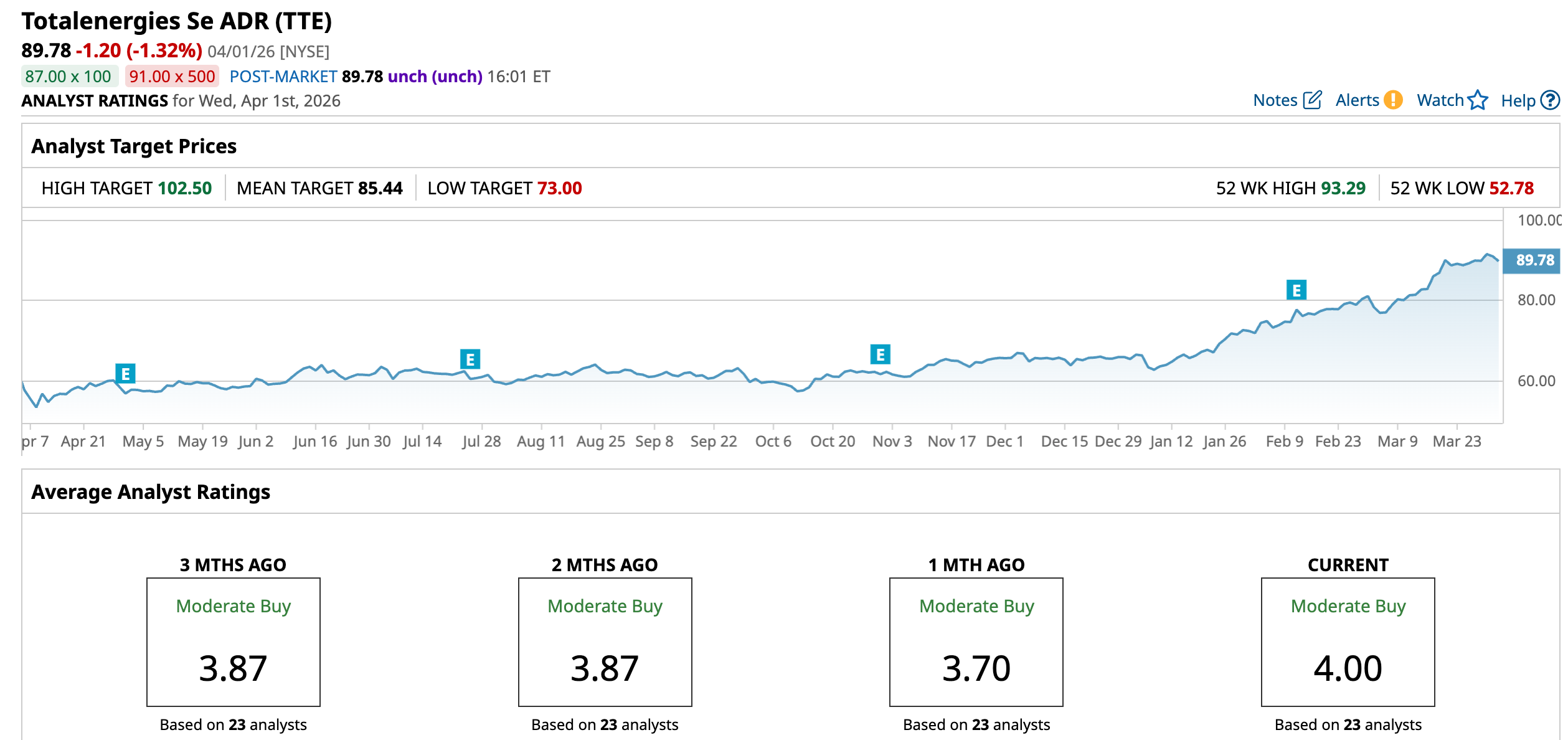

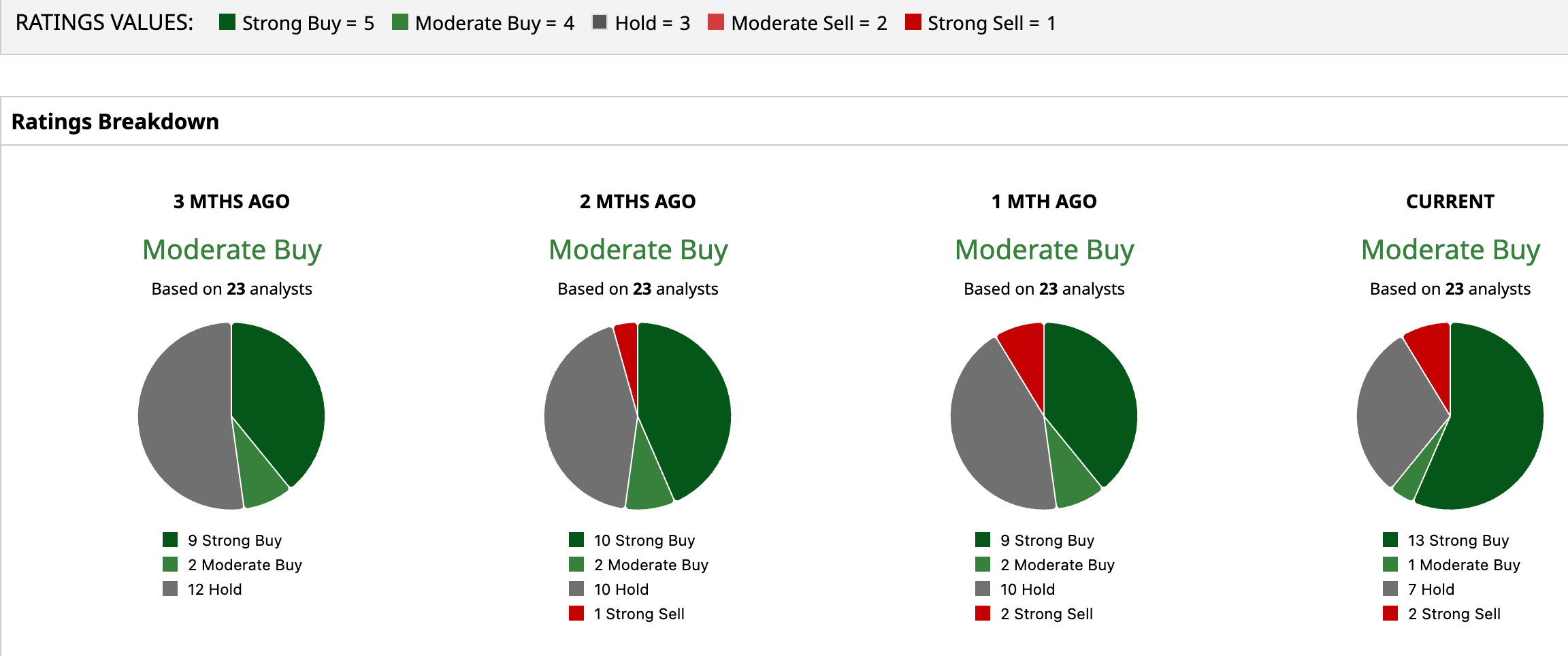

Wall Street’s stance on TotalEnergies remains decisively upbeat, with the stock carrying a “Moderate Buy” consensus, though the underlying sentiment skews far more bullish than the headline suggests. Of the 23 analysts covering the name, 13 have issued “Strong Buy” ratings, one recommends “Moderate Buy,” seven remain on the sidelines with “Hold,” and just two take a bearish stance with “Strong Sell” ratings.

While the stock has already surpassed the average price target of $85.44, expectations for further upside haven’t faded. The Street-high target of $102.50 still implies roughly 14.17% upside from current levels, pointing to continued confidence in the company’s earnings resilience and disciplined capital strategy.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)