/Apple%20products%20arranged%20on%20desk%20by%20tashka2000%20via%20iStock.jpg)

Markets haven’t had it easy lately. Rising geopolitical tensions of the U.S.-Iran war have rattled sentiment, fueling concerns around supply shocks and sticky inflation just as investors were hoping for stability. The benchmark S&P 500 Index ($SPX) has struggled to find its footing in 2026, slipping into negative territory as investors rotate out of risk. While weakness has been broad-based, a large chunk of the downside has come from the “Magnificent Seven,” the very names that powered the rally. As risk appetite fades and valuations compress, these heavyweight tech stocks have gone from market leaders to market drags.

But even within this selloff, there’s a clear divergence. Tech giant Apple (AAPL) has managed to hold its ground far better than its Magnificent Seven peers, with only a modest single-digit decline compared to the sharper double-digit drops seen elsewhere in the group. As cracks begin to show across high-growth tech, Apple’s resilience is standing out, making it one of the few mega-cap names still commanding confidence in this uneasy market. So, keeping these factors in mind, is AAPL stock a compelling investment candidate now?

About Apple Stock

Cupertino, California-based Apple remains one of the most deeply entrenched players in the technology sector, built on a portfolio that spans the iPhone, Mac computers, Apple Watch, and AirPods. Over the years, the company has focused on weaving these products together through a tightly integrated ecosystem of hardware, software, and services, allowing users to move seamlessly across devices within a single, connected environment.

Its presence extends across multiple layers of the tech landscape, from smartphones and personal computing to digital content and cloud-based services. At the same time, Apple has been gradually channeling investments into newer areas such as artificial intelligence (AI), wearables, and mixed reality, an indication of how it is positioning itself to adapt alongside shifting industry dynamics rather than relying solely on its legacy strengths.

With a hefty market capitalization of roughly $3.6 trillion, the iPhone maker ranks as the world’s second-most-valuable company, trailing only Nvidia (NVDA), which has surged on the back of AI enthusiasm. Yet, even a company of Apple’s scale and legacy hasn’t been spared from the current wave of market pressure. Moreover, mounting competitive pressures and a slower-than-expected rollout in AI initiatives have introduced a degree of caution among investors, and the stock has lagged the broader S&P 500 Index, which itself is down 5.83% so far in 2026.

Still, Apple’s relative performance tells a more nuanced story. Despite the headwinds, it remains the best-performing stock within the Magnificent Seven, declining a comparatively modest 8.38% year-to-date (YTD). That’s a far smaller drop than what peers like Microsoft (MSFT) and Tesla (TSLA) have experienced, with losses of 24.16% and 18.94%, respectively. Even Nvidia, despite its AI-driven narrative, has slipped more, down 8.5% this year.

Apple’s Q1 Earnings Snapshot

Apple kicked off fiscal 2026 with a performance that reminded investors why it remains a cornerstone of the tech sector. In its first-quarter results reported on Jan. 29, the company comfortably cleared Wall Street’s expectations on both revenue and earnings, driven largely by the continued strength of its flagship iPhone business. Revenue climbed 15.6% year-over-year (YOY) to $143.76 billion, handily surpassing the consensus estimate of $137.81 billion.

The iPhone once again did the heavy lifting. Sales surged 23.3% annually to $85.3 billion, fueled by strong demand for the iPhone 17 lineup launched in September. CEO Tim Cook described it as a “record-breaking quarter,” highlighting robust demand across all regions. Notably, Apple saw exceptional traction in Greater China, including Taiwan and Hong Kong, where revenue jumped 38% to $25.5 billion, underscoring the brand’s enduring global appeal.

However, outside of the iPhone, the picture was more mixed. iPad revenue posted a modest 6.3% increase, while Mac sales declined 7%, reflecting softer demand in personal computing. The Wearables, Home, and Accessories segment, which includes products like AirPods, Apple Watch, and Vision Pro, also edged lower by about 2%, suggesting some pressure in discretionary spending categories.

Still, Apple’s broader ecosystem continues to expand at scale. The company’s active installed base reached 2.5 billion devices, up from 2.35 billion a year ago, reinforcing the strength of its worldwide footprint. Meanwhile, its high-margin services business, spanning offerings like Apple TV+, iCloud, advertising partnerships, and AppleCare, grew 14% YOY to $30 billion, providing a steady and increasingly important revenue stream.

On the profitability front, Apple delivered earnings per share of $2.84, up 18.3% YOY and well ahead of expectations of $2.65. Also, CFO Kevan Parekh highlighted the company’s robust cash generation, with nearly $54 billion in operating cash flow during the quarter, enabling Apple to return close to $32 billion to shareholders. In summary, it was a quarter that showcased both the company’s core strength and the evolving dynamics within its broader business mix.

How Are Analysts Viewing Apple Stock?

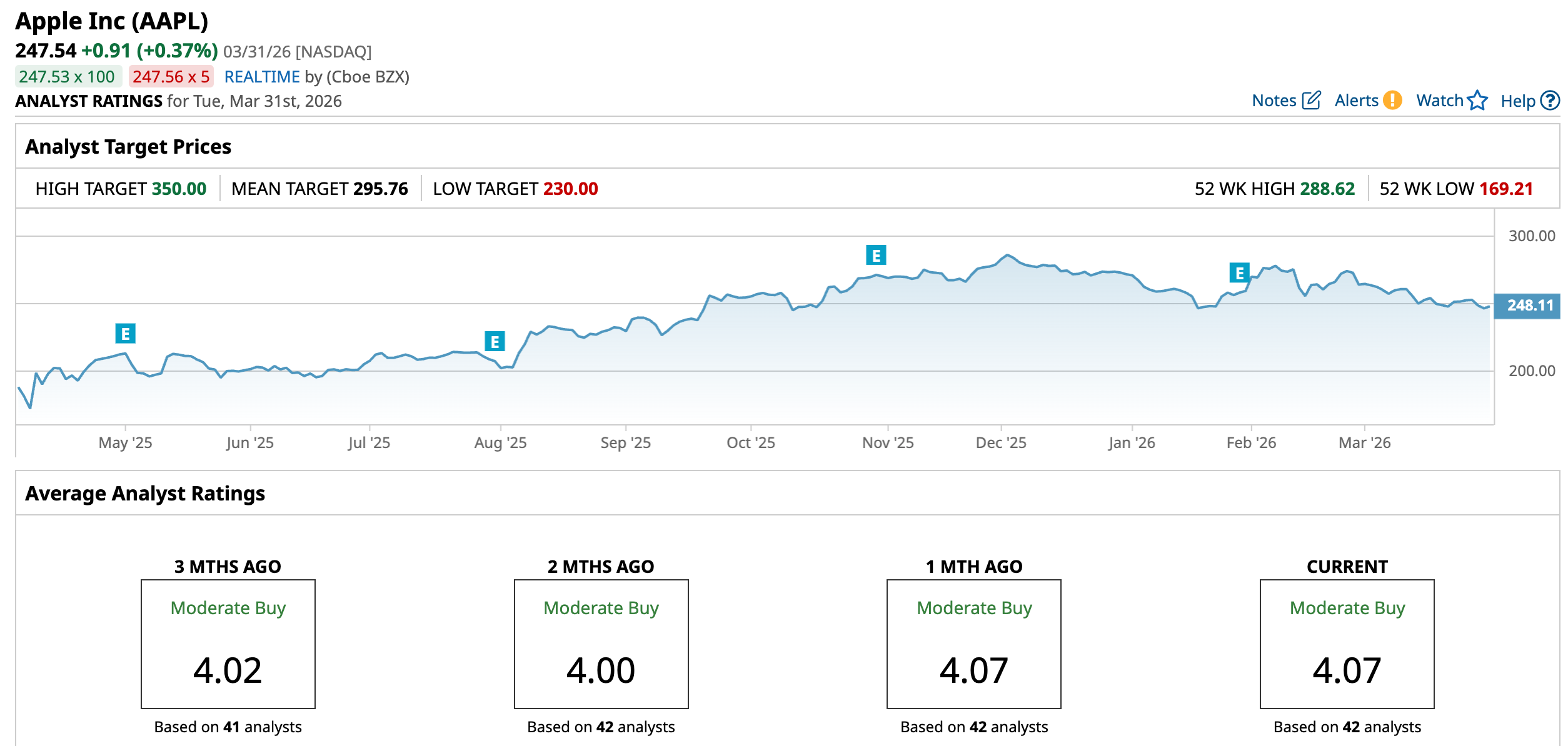

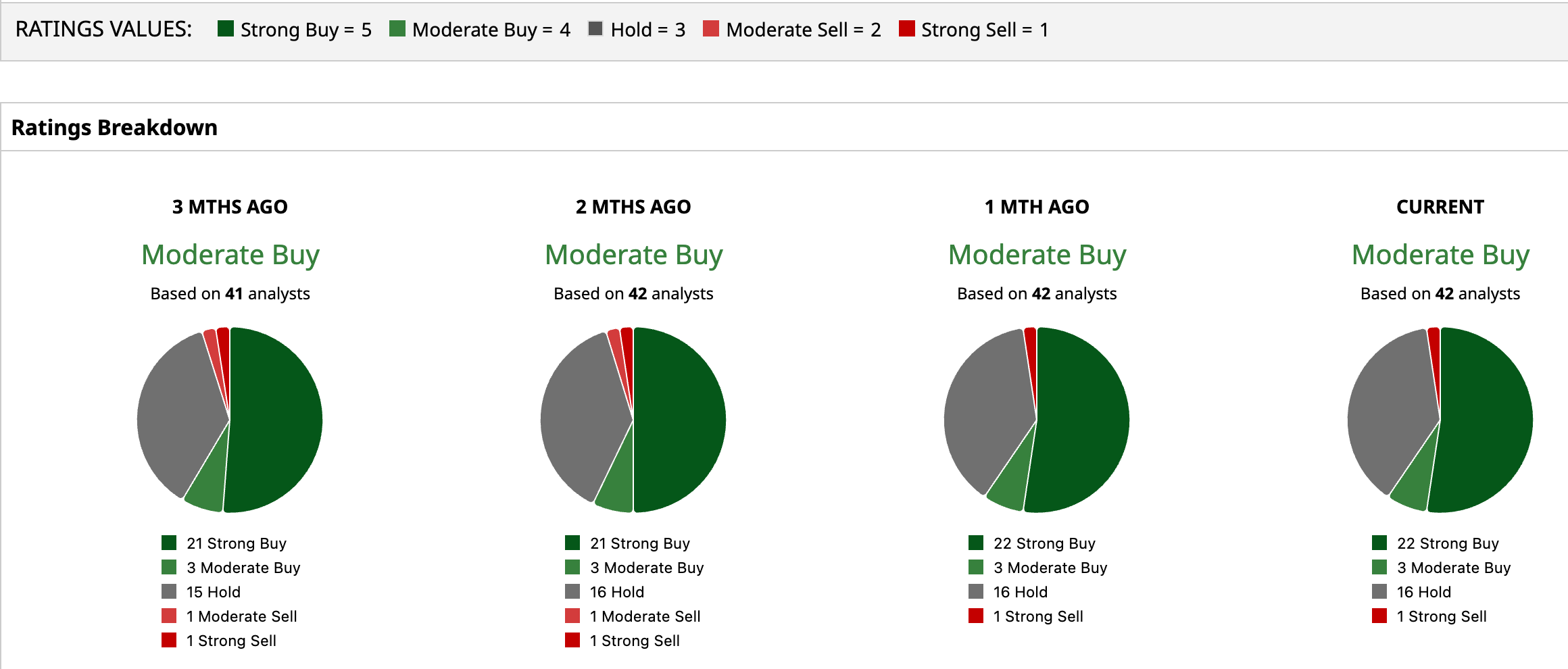

Despite recent volatility in its shares, Wall Street continues to maintain a positive stance on Apple, with the stock earning a consensus “Moderate Buy” rating overall. Of the 42 analysts covering the stock, 22 have issued “Strong Buy” ratings, three recommend “Moderate Buy,” 16 suggest “Hold,” and only one has a “Strong Sell” call, highlighting a broadly favorable outlook.

Looking ahead, the upside potential remains notable. The average price target of $295.76 implies a 19.5% gain from current levels, while the Street-high target of $350 points to potential upside of 41.4%, suggesting that many analysts still see room for further growth despite near-term headwinds.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)