/AI%20(artificial%20intelligence)/AI%20by%20TierneyMJ%20via%20Shutterstock.jpg)

Leading data storage manufacturer Western Digital Corporation (WDC), now simply known as WD, has long functioned as the world’s digital warehouse, storing the enormous volumes of data generated by cloud platforms and artificial intelligence (AI) systems. Its core strength lies in high-capacity hard drives, particularly nearline drives that hyperscalers depend upon. Over the past year, that sweet spot translated into strong momentum, as soaring demand for memory and storage, driven by AI, powered the company’s growth.

However, that momentum hit a sharp break on March 25. The stock came under intense selling pressure after Alphabet’s Google (GOOG) (GOOGL) unveiled TurboQuant, a new compression technology designed to significantly reduce memory usage in large language models and vector search engines. The innovation tackles a major bottleneck known as the key-value cache, which stores frequently accessed information in AI systems.

What spooked the market was the scale of improvement. According to Google, TurboQuant can compress key-value cache down to just three bits, without any training or fine-tuning, while preserving model accuracy. Tests on open-source models like Gemma and Mistral showed a striking 6x reduction in memory size. On top of that, the technology delivered up to an 8x performance boost on Nvidia (NVDA) H100 GPU accelerators. And the market reaction was swift and sharp.

Memory and storage stocks, including WDC, saw a notable sell-off as investors reassessed future demand. The concern is that increasingly efficient AI systems may require significantly less memory and storage, potentially weakening one of the key growth drivers that has been powering WDC's recent performance. So, with this unexpected disruption now in play, does this dip present a buying opportunity, or is it a warning sign to stay on the sidelines for now?

About Western Digital Stock

California-based Western Digital is increasingly aligned with the data center ecosystem, with nearly 90% of its business now tied to AI and cloud-related demand. The company focuses on building large-scale storage infrastructure used by hyperscalers, cloud providers, and enterprises to handle rapidly growing data workloads. As data generation accelerates, WD’s role remains centered on supporting the storage, management, and accessibility of that data across high-demand environments.

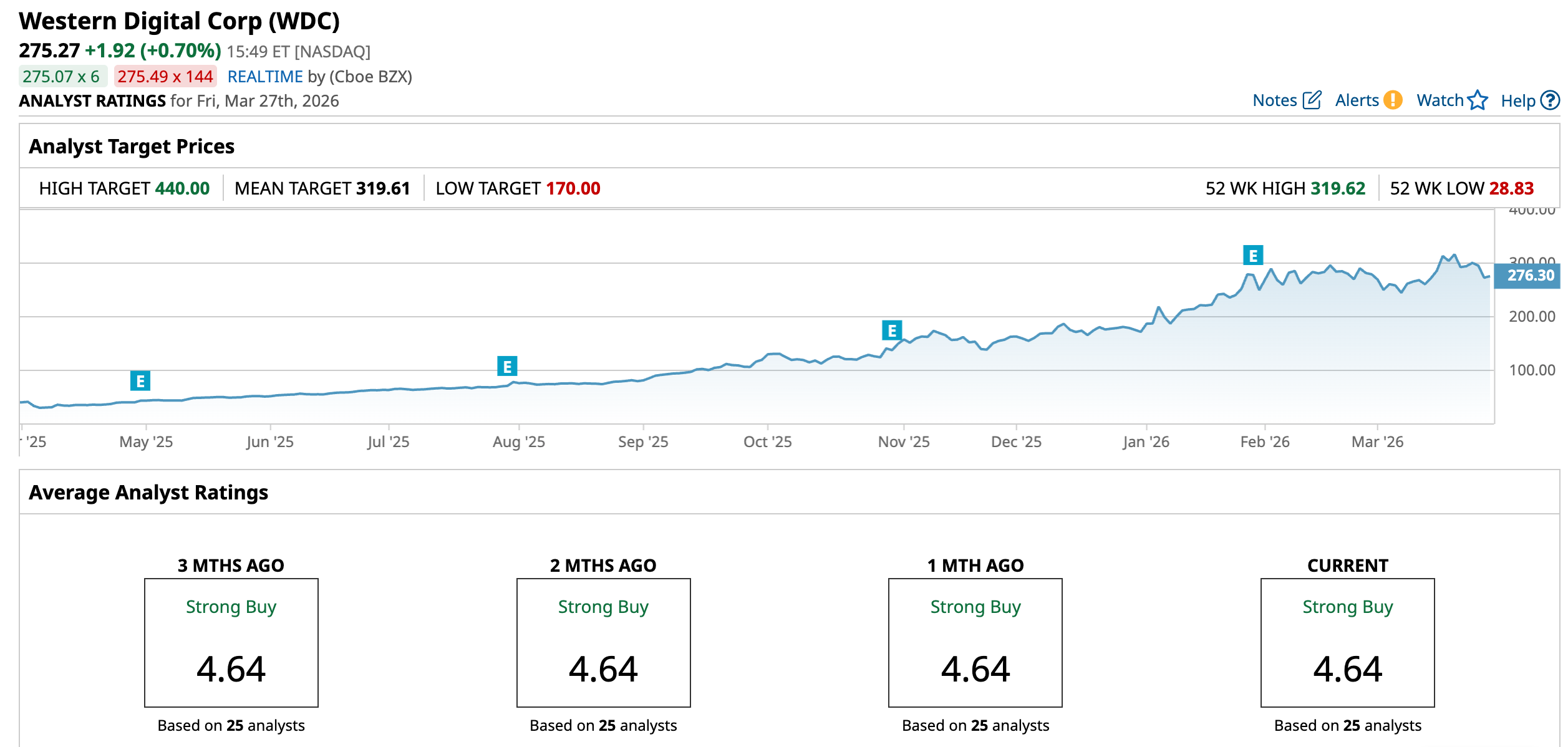

With a market capitalization of roughly $92.7 billion, Western Digital has recently come under pressure following Google’s latest breakthrough. The stock has dropped nearly 5.95% in just the past five trading sessions, reflecting quick sentiment reaction. But zoom out, and the bigger picture tells a very different story.

WDC has been one of the standout performers of the AI trade, delivering a staggering 557.8% rally over the past year as demand for memory and storage solutions surged. In comparison, the broader S&P 500 Index ($SPX) has gained just 11.9% over the same period, a gap that highlights how aggressively investors have bet on the data infrastructure theme.

Even in 2026, despite the recent pullback, the stock remains firmly ahead of the market. WDC is still up an impressive 60% year-to-date (YTD), while the broader index has slipped almost 7%.

Inside Western Digital’s Q2 Earnings Report

In late January, WDC delivered a powerful set of results for its fiscal 2026 second quarter, underscoring strong demand in the AI-driven data landscape. The company reported revenue of $3.02 billion, up 25% year-over-year (YOY), comfortably beating Wall Street’s $2.94 billion estimate. Profit growth was even more striking. Adjusted EPS surged 78% to $2.13, well ahead of expectations of $1.93 per share.

Margins expanded sharply, with non-GAAP gross margin reaching 46.1%, a significant 770-basis-point improvement from a year ago. Notably, both revenue and adjusted EPS landed above the high end of management’s guidance, signaling strong execution. The defining story of the quarter was the overwhelming strength of the Cloud segment. Cloud revenue jumped 28% YOY and now accounts for a remarkable 89% of total revenue, or roughly $2.7 billion.

This surge reflects aggressive spending by hyperscalers, which are rapidly scaling data center capacity to support generative and agentic AI workloads. WDC shipped an impressive 215 exabytes during the quarter, and demand for its high-capacity nearline drives, which are critical for large-scale data storage, has been so strong that the company’s production capacity is effectively sold out through the end of calendar 2026.

CEO Irving Tan underscored this momentum, stating that the company’s strong performance reflects disciplined execution in meeting demand from the AI-driven data economy, along with customer confidence in WDC’s ability to deliver reliable, high-capacity storage at scale. The quarter also showcased strong cash generation and shareholder returns.

WDC produced $653 million in free cash flow and returned more than 100% of it to shareholders, including $615 million in stock buybacks, alongside a quarterly dividend. Looking ahead, management struck a confident tone, guiding for $3.2 billion in revenue in fiscal Q3 2026, with margins expected to expand further to 47%–48%. Adjusted EPS is projected in the range of $2.15 to $2.45, indicating that momentum is expected to carry forward.

What Do Analysts Expect for Western Digital Stock?

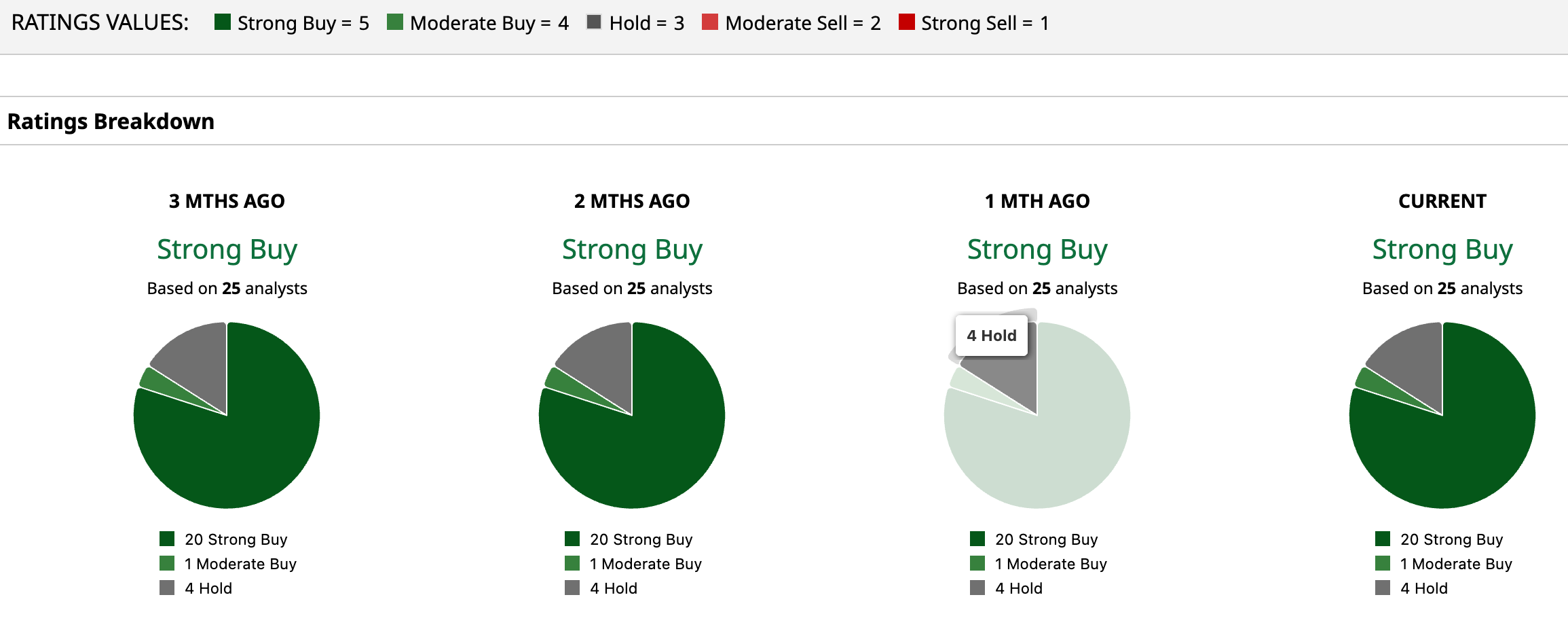

Even after the recent volatility, Wall Street’s conviction in WDC remains firmly intact. The stock continues to command a “Strong Buy” consensus rating, underscoring how analysts are largely looking past near-term disruptions. Out of 25 analysts covering WDC, a striking 20 have issued “Strong Buy” calls, with just one “Moderate Buy”, while only four remain on the sidelines with a “Hold.”

The overwhelming tilt toward bullish ratings highlights confidence that the company’s core growth drivers are still very much in play. That optimism is also reflected in price targets. The average target of $319.61 suggests 16% upside from current levels. At the upper end, the Street-high target of $440 points to a potential 60% upside, signaling expectations of continued strength as demand for data infrastructure evolves.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)