/D_R_%20Horton%20Inc_%20billboard%20by-%20monticello%20via%20Shutterstock(1).jpg)

Arlington, Texas-based D.R. Horton, Inc. (DHI) operates as a homebuilding company in the East, North, Southeast, South Central, Southwest, and Northwest regions in the United States. The company has a market capitalization of $39.4 billion and is expected to release its Q2 2026 earnings on Tuesday, Apr. 21, before the market opens.

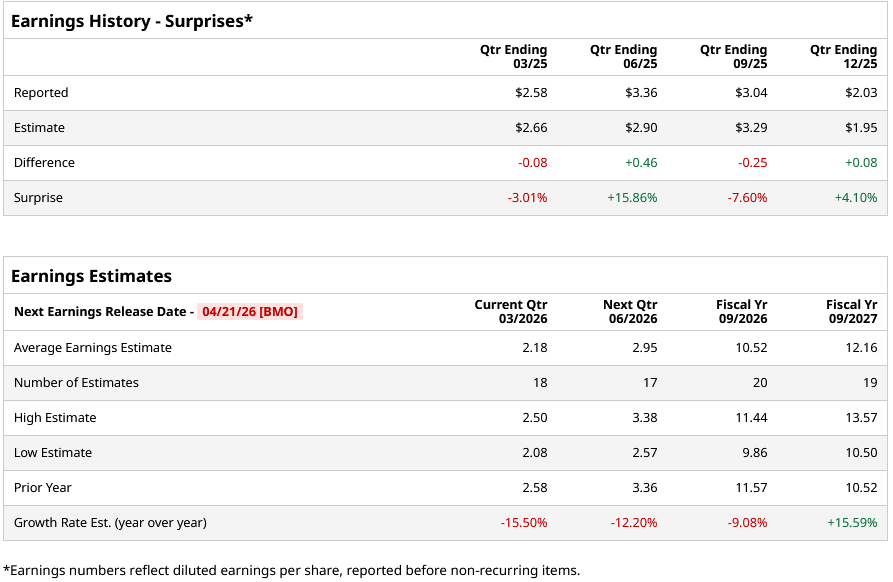

Ahead of the event, analysts expect the company’s EPS to be $2.18 on a diluted basis, down 15.5% from $2.58 in the year-ago quarter. The company has exceeded Wall Street’s EPS estimates in two of its last four quarters, while missing them in two others.

For fiscal 2026, analysts project the company’s EPS to be $10.52, down 9.1% from $11.57 in fiscal 2025. However, its EPS is expected to rise by roughly 15.6% year over year (YoY) to $12.16 in fiscal 2027.

DHI stock has surged 5.1% over the past 52 weeks, underperforming the S&P 500 Index’s ($SPX) 13.4% rise and the State Street Consumer Cyclical Select Sector SPDR ETF’s (XLY) 7.1% return during the same time frame.

On Mar. 23, DHI stock closed up more than 3% after the 10-year T-note yield declined 5 basis points. The 10-year Treasury note yield directly affects housing demand by changing borrower affordability and is considered the primary benchmark for 30-year fixed mortgage rates. As the T-note yield declines, mortgage rates decrease, increasing buyer purchasing power and, in turn, housing demand.

Analysts are neutral on DHI, with the stock currently rated “Hold.” Among the 21 analysts covering the stock, five are recommending a “Strong Buy,” 13 suggest a “Hold,” and three recommend “Strong Sell” for the stock. DHI’s average analyst price target is $160.93, indicating an upside of 18.4% from the current levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)