GameStop (GME) is once again at the center of Wall Street conversation, but this time the focus is squarely on its balance sheet. The company recently reported a cash and marketable securities position of about $9 billion, a figure that sits remarkably close to its $10.34 billion market value. This gives it far more financial flexibility than a typical specialty retailer, however, raising an obvious question about what management plans to do, especially as talk of mergers and acquisitions continues to build around the name.

Michael Burry, who once exited GME before the 2021 surge, is now revisiting the stock as the company shifts toward a leaner model under Ryan Cohen’s leadership. That combination of a fortified balance sheet, a more disciplined business, and a still-elevated short interest has set the stage for a new chapter in the GME saga.

The real puzzle now is straightforward. Does nearly $9 billion in cash become the launchpad for a transformative deal and a higher long-term valuation, or does it simply cap the upside if execution falls short? Let’s dive in.

GameStop's Financial Performance

GameStop is a U.S.-based specialty retailer focused on video games, consumer electronics, and collectibles. The stock is up 15.54% year-to-date (YTD) but down 20.15% over the past 52 weeks.

This valuation translates into a price-earnings of 24.04 times and a price-to-sales of 2.85 times, versus sector medians of 14.98 times and 0.90 times, respectively, suggesting investors are paying a premium multiple.

Their fourth-quarter results, released in late March, showed net sales of $1.104 billion, down from $1.283 billion in the prior-year quarter. This period still delivered operating income of $135.2 million, a sharp improvement over $79.8 million a year earlier, which indicates tighter cost control and better operational efficiency despite lower revenue.

Also, it reported quarterly net income of $127.9 million versus $131.3 million in the previous year’s fourth quarter. The slight decline in bottom line profit alongside higher operating income reflects the impact of non-operating items.

GME’s balance sheet stands out most in its latest release. The company closed the quarter with $9.0 billion in cash, cash equivalents, and marketable securities, nearly doubling from $4.8 billion a year earlier, which is an extraordinary cash position relative to its equity value. That figure includes $368.4 million in Bitcoin and related receivables, adding a differentiated, higher-risk component to its asset mix.

GME’s High-Stakes Megadeal Gamble

GameStop CEO Ryan Cohen’s incentives and strategy are tightly wired to how far GameStop can push its valuation if it executes on a bold acquisition plan. The board has approved a performance-based compensation package that gives Cohen no guaranteed salary or stock, yet still positions him to earn billions if strict hurdles are met.

This plan pays out in full only if GameStop’s market cap increases roughly tenfold and cumulative performance EBITDA reaches about $10 billion by 2035. That structure effectively ties his personal upside to turning today’s roughly $10 billion-$11 billion equity value into a $100 billion company.

Cohen has been explicit about his hopes to bridge that gap. He recently said the company is working on a “very, very, very big” purchase of a larger consumer business, calling the prospective deal “transformational” not just for GameStop but for capital markets more broadly.

He suggested that, if successful, the transaction could ultimately make GameStop worth several hundred billion dollars, a striking claim given the stock’s current market capitalization of $10.34 billion. Cohen himself acknowledged the binary nature of the bet, “if it works, it will look like genius; if it fails, it will look totally, totally foolish.”

Meanwhile, GameStop director Lawrence Cheng recently bought 5,000 GME shares at an average price of $22.87, bringing his total stake to 88,000 shares. This insider purchase came during a pickup in volume and a rising share price, which again drew in a large crowd of retail traders around the stock.

What the Market is (Not) Saying

GameStop’s earnings visibility is unusually opaque right now, with zero formal projections on the board. This lack of numbers is important because it means there is no real consensus anchor for how the market should be valuing that nearly $9 billion cash position.

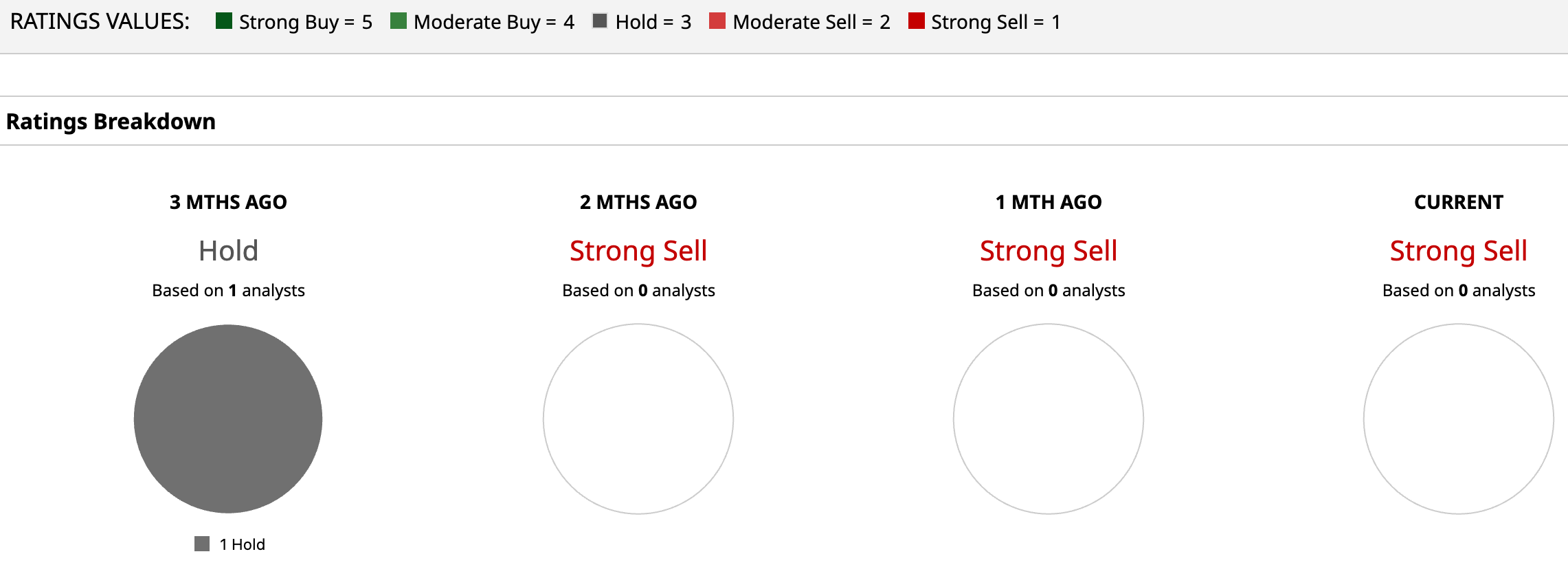

Analyst coverage of GME stock is severely lacking, and no major firms currently maintain an active rating. Consensus pricing still exists on paper, as the average 12-month price target sits around $13.50, which implies roughly a 40% downside. That gap shows how far sentiment in published models lags the current narrative.

Conclusion

GameStop’s nearly $9 billion cash pile, Cohen’s high-stakes pay plan, and the “very, very, very big” deal chatter all point to one thing. This story now hinges on execution, not survival. If management lands a smart, accretive acquisition and turns that cash into real earnings power, GME could justify a higher valuation over time. If the megadeal stumbles or never materializes, the premium multiple likely fades, and the stock drifts lower toward its cash and core retail value.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)