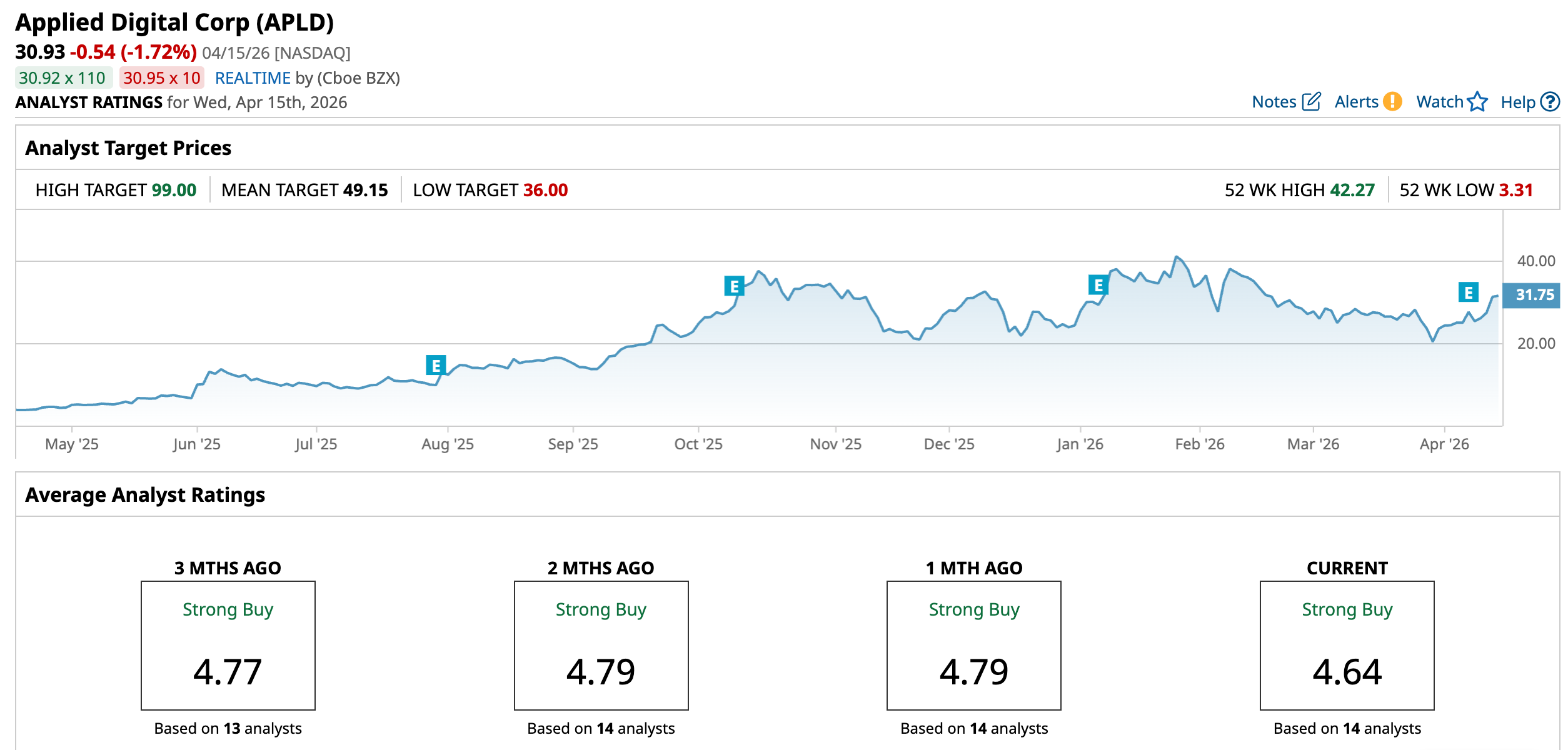

Wall Street’s conviction around Applied Digital Corporation (APLD) remains strikingly bullish, even after the stock’s massive run over the past year. Despite near-term volatility tied to execution risks and capital intensity, analysts continue to view the company as a prominent artificial intelligence (AI) infrastructure play with upside, driven by surging demand for hyperscale data center capacity.

Notably, the Street-high price target stands at $99, issued by Arete Research, implying well over 200% upside from recent trading levels. This bullish target reflects expectations that Applied Digital can rapidly scale its high-performance computing (HPC) hosting platform and secure long-term hyperscaler contracts, positioning it as a critical enabler of the AI buildout cycle.

About Applied Digital Stock

Applied Digital is a provider of next-generation digital infrastructure, specializing in the design, development, and operation of high-performance data centers and cloud services tailored to the AI and HPC markets. Headquartered in Dallas, Texas, it serves clients with large-scale data-center hosting, GPU-computing and HPC solutions. The company’s market cap stands at $9 billion, signaling its growing role in the booming AI infrastructure ecosystem.

Applied Digital’s stock has delivered extraordinary but highly volatile returns, reinforcing its positioning as a high-beta AI infrastructure play. The stock is up around 27.8% year-to-date (YTD), reflecting a recovery from its pullback earlier in the year and renewed investor appetite for AI-linked infrastructure names.

Over a longer horizon, the magnitude of gains is even more striking. Applied Digital has generated 486% returns over the past 52 weeks, driven by the company’s pivot toward HPC and AI data center hosting. The stock is currently down 25.7% from its 52-week high of $42.27, reached on Jan. 28.

In the most recent trading session, momentum accelerated sharply. The stock surged roughly 14% intraday, closing the last session at $31.42, amid positive analyst ratings following the earnings release and high demand for AI infrastructure.

The stock is currently trading at a premium to its industry peers at 21.46 times forward price-to-sales.

Mixed Financial Performance

Applied Digital Corporation reported its fiscal Q3 2026 results on Apr. 8, delivering a strong top line beat but highlighting the trade-off between rapid growth and profitability.

The company generated revenue of $126.6 million, up 139% year-over-year (YOY), driven primarily by the ramp-up of its HPC data center business. At the profitability level, adjusted EBITDA surged to $44.1 million from $6.3 million a year ago, while adjusted net income reached $33.2 million (or $0.09 per share), compared to an adjusted loss of $2.6 million last year, reflecting improving operating leverage in its core hosting business.

However, GAAP metrics remained under pressure, with the company reporting a net loss of $100.9 million versus a $36.1 million loss in the prior-year quarter and loss per share of $0.36 versus $0.16 last year.

Applied Digital aims to achieve a $1 billion net operating income (NOI) run rate within five years, supported by an active development pipeline.

Analysts predict loss per share to improve 35% YOY to $0.52 for fiscal 2026, and another 69.2% annually to -0.16 in fiscal 2027.

Wall Street is Majorly Bullish on Applied Digital

Most recently, H.C. Wainwright reiterated a “Buy” rating and $40 price target on Applied Digital Corporation after its Q3 results, highlighting strong growth despite profitability concerns. While the company is still expected to post losses this year, analysts remain optimistic given its expanding pipeline and hyperscaler-driven AI infrastructure demand.

Applied Digital also received a reiterated “Buy” rating and $45 price target from Compass Point, while Needham maintained a “Buy” rating and $41 price target, following its Q3 results, implying meaningful upside from current levels.

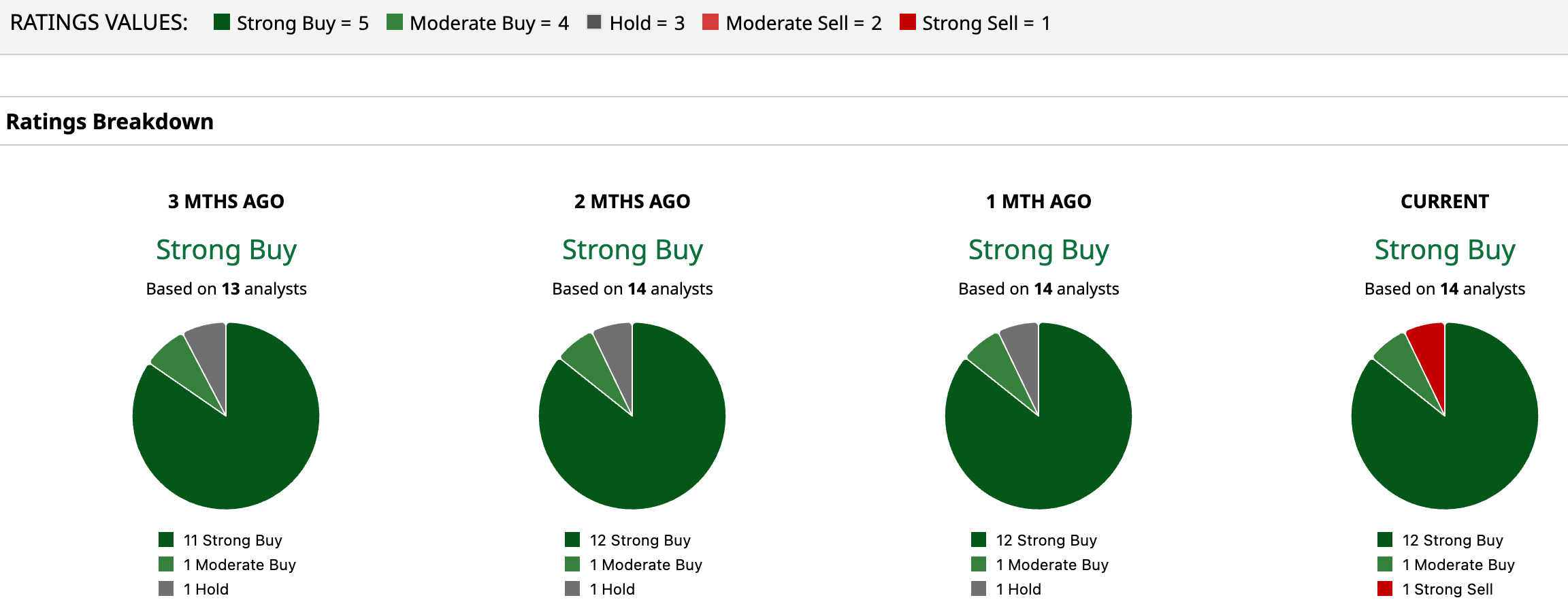

Overall, APLD has a consensus “Strong Buy” rating. Of the 14 analysts covering the stock, 12 advise a “Strong Buy,” one suggests a “Moderate Buy,” and one gives it a “Strong Sell” rating.

The average analyst price target for APLD is $49.15, indicating a potential upside of 59%. The Street-high target price of $99 suggests that the stock could rally as much as 220%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)