/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

Artificial intelligence (AI) is fast becoming an infrastructure race, and CoreWeave (CRWV) has found itself right in the middle of it. The company, which started out in crypto, now runs cloud systems built to handle heavy AI workloads, helping businesses scale quickly as demand for computing power surges.

That rising demand is now showing up in big deals. CoreWeave recently signed a multi-year data center agreement with Anthropic to support its Claude AI models. The plan is to roll out additional compute capacity over time, using advanced chips from Nvidia (NVDA) across U.S. facilities. The news gave the stock a lift, as investors took it as another sign that CoreWeave is becoming a key player in the AI buildout.

The backdrop makes it even more interesting. Anthropic, backed by giants like Amazon (AMZN) and Alphabet (GOOG) (GOOGL), is scaling aggressively, and its partnership adds credibility to CoreWeave’s platform. Plus, timing is adding to the momentum. On Apr. 9, Meta Platforms (META) expanded its own AI deal with the company, pointing to strong demand from big tech clients.

With deals stacking up and AI spending still on the rise, CoreWeave seems to be in a sweet spot. But after the recent run-up, does this Anthropic deal still make the stock worth buying now?

About CoreWeave Stock

CoreWeave, founded in 2017 and headquartered in Livingston, New Jersey, has rapidly established itself as a leader in GPU-optimized cloud infrastructure. With a market capitalization of $46.2 billion, the company supports the accelerating AI revolution through systems designed for generative AI and large-scale compute workloads. Its mission is to streamline modern AI complexity and empower enterprises to deploy intelligence at scale, positioning CoreWeave as a foundational pillar of next-generation technology.

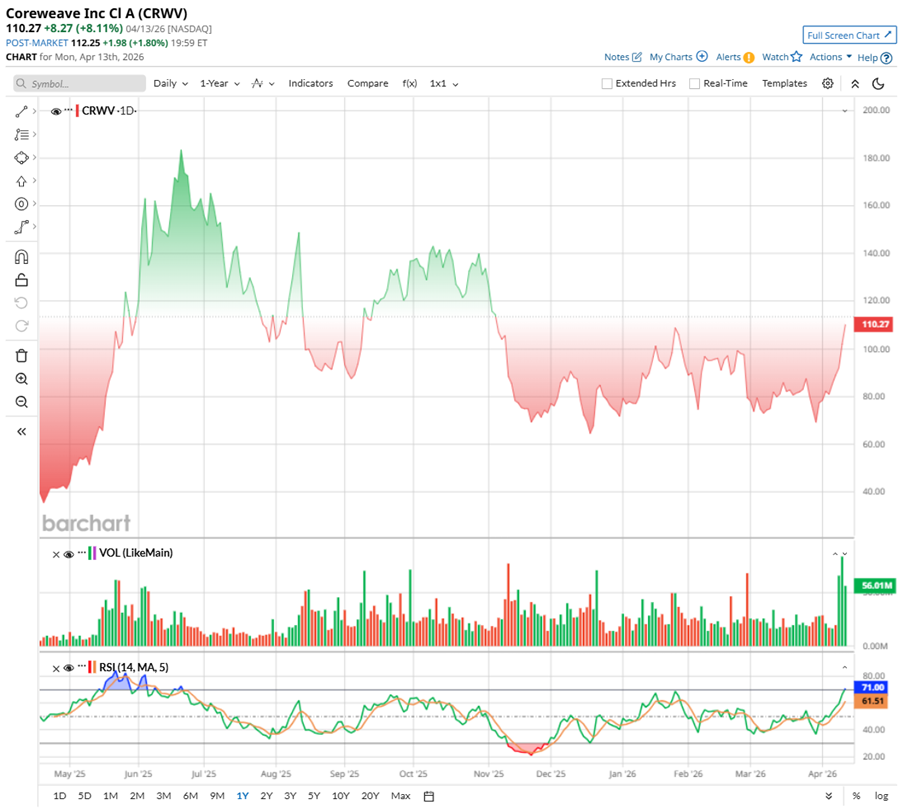

CRWV stock has been riding the same wave as the broader AI trade – fast up, sharp down, and never boring. The company went public in March 2025 at $40 and quickly caught fire, rallying to a high of $187 by June 20. That surge was fueled by a string of AI cloud deals, partnerships, acquisitions, and even a push into federal contracts, putting CoreWeave firmly on investors’ radar.

But the ride has not been smooth. The stock has since pulled back and now trades $117, still well above its 52-week low of $33.51, but about 37% below its peak. Volatility showed up again when the company issued weaker-than-expected Q1 2026 guidance on Feb. 27, triggering an 18.5% single-day drop, reminding investors how sensitive high-growth AI names can be to outlook changes.

Even then, the bigger trend remains strong. CRWV is still up 170.65% over the past 52 weeks and 64.82% year-to-date (YTD). Momentum has picked up sharply in recent weeks, with the stock rising 45.52% in a month and over 38.47% in just the past five days, largely driven by the Anthropic deal news.

Technically, trading volumes are rising, signaling strong buying interest, while the 14-day RSI has moved into overbought territory at 74.52, suggesting the rally may be running a bit hot in the near term.

Even after the pullback, CoreWeave isn’t cheap, priced at 4.66 times forward sales. The market is clearly pricing in aggressive AI-driven growth and a long runway ahead, leaving little room for execution missteps.

CoreWeave Stock Gets a Broader Backing with Anthropic Deal

CoreWeave was growing fast, but much of that growth leaned heavily on a few large customers. The agreement with Anthropic begins to ease that dependence and signals a more diversified growth path.

This partnership shows that demand for CoreWeave’s infrastructure is widening. By bringing in another major AI player, the company is steadily building a more balanced and resilient business model. It is no longer just about landing big deals – it’s about who those deals are coming from.

Plus, the move reinforces CoreWeave’s credibility in a highly competitive space. Winning over advanced AI labs signals that its platform can meet the growing needs of cutting-edge model development. For investors, that shifts the view from customer concentration risk to a wider growth opportunity.

CoreWeave Reports Mixed 2025 Results

CoreWeave’s latest results show a company scaling rapidly with the AI boom. In the fourth quarter of 2025, the company delivered a top-line beat, with revenue hitting $1.57 billion, up 110% year-over-year (YOY), driven by surging GPU demand from hyperscalers like Microsoft (MSFT) and OpenAI. For fiscal 2025, revenue reached $5.1 billion, marking an impressive 168% annual growth.

But this is a growth-at-all-costs phase. CoreWeave reported an adjusted net loss of $606 million for the year, as it continues to invest heavily to scale. Still, profitability at the operating level showed strength, with adjusted EBITDA more than doubling to $3.1 billion and margins touching 60%. Even more striking, its backlog surged to $66.8 billion – over four times higher than last year – offering strong visibility into future revenue.

The company is clearly building ahead of demand. In Q4 alone, capital expenditures hit $8.2 billion, taking the full-year total to $14.9 billion. That’s higher than expected, but reflects its ability to bring infrastructure online faster. It added 260 megawatts of active power in Q4 across 43 data centers, with active power capacity totaling 850 megawatts. However, this rapid expansion is also pushing up costs, with operating expenses rising to $1.66 billion and interest expenses climbing to $388 million due to higher debt.

To support this scale-up, CoreWeave has been actively strengthening its balance sheet. It ended 2025 with $4.2 billion in cash, cash equivalents, restricted cash and marketable securities, and raised $2.6 billion through convertible notes, while expanding its credit facility to $2.5 billion. Overall, it secured more than $18 billion in capital during the year, backed by over 200 investment partners and financial institutions.

Looking ahead, the management has set a cautious tone for the near term, even as the long-term story remains strong. For Q1, revenue is expected to be between $1.9 billion and $2 billion, slightly below market expectations. Margins are also expected to be under pressure, with adjusted operating income projected in the range of $0 to $40 million. Management has made it clear that Q1 will likely be the lowest point for margins this year.

The reason is simple – CoreWeave is still in heavy build-out mode. It plans to deploy $6 billion to $7 billion in infrastructure in just Q1, continuing to bring large amounts of new capacity online. As CFO Nitin Agrawal explained, margins should gradually improve through the year, returning to low double-digit levels by Q4 as new capacity starts generating revenue.

For the full year 2026, the company expects revenue to reach between $12 billion and $13 billion. At the same time, it plans a massive $30 billion to $35 billion in capital spending, more than double last year’s levels. Importantly, management noted that almost all of this spending is backed by already signed customer contracts, giving strong visibility into future growth. Adjusted operating income for the year is expected to come in between $900 million and $1.1 billion, reflecting both scale and improving efficiency over time.

CEO Mike Intrator didn’t sugarcoat the situation, making it clear on the earnings call that “Our margins reflect the cost of building tomorrow’s revenues.”

Analysts tracking CoreWeave anticipate fiscal 2026 revenue to be around $12.4 billion, while losses are expected to continue, pegged at -$4.16 per share, widening by 54.7% YOY. The turnaround might start showing in fiscal 2027, when losses are expected to shrink by 8.9% annually and come down to -$3.79 per share.

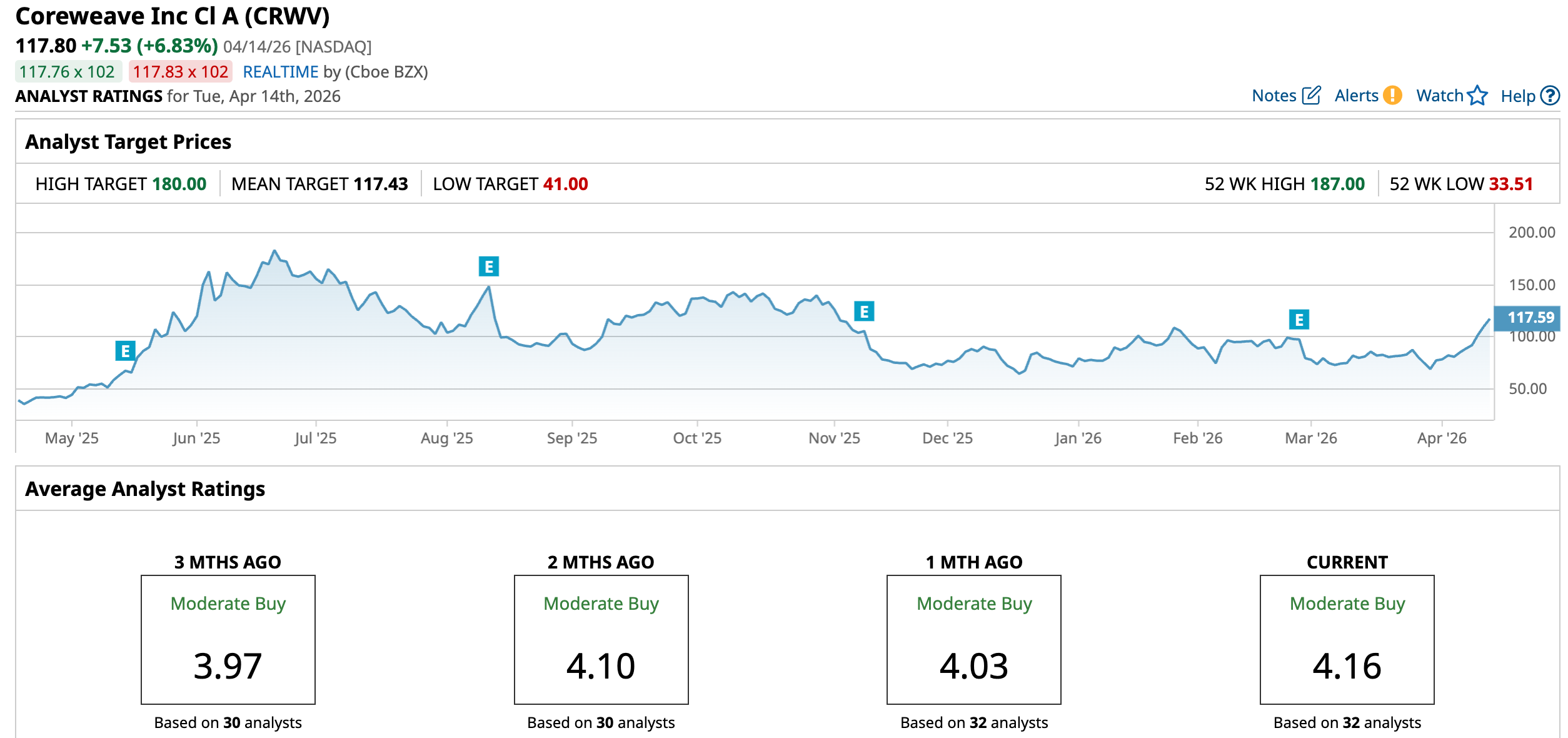

What Do Analysts Expect for CoreWeave Stock?

DA Davidson remains positive on CoreWeave, raising its price target to $175 from $125 while keeping a “Buy” rating. The brokerage firm points to the recent Anthropic deal and expanded Meta Platforms partnership as signs that CoreWeave is becoming a preferred cloud provider for leading AI labs driving future compute demand.

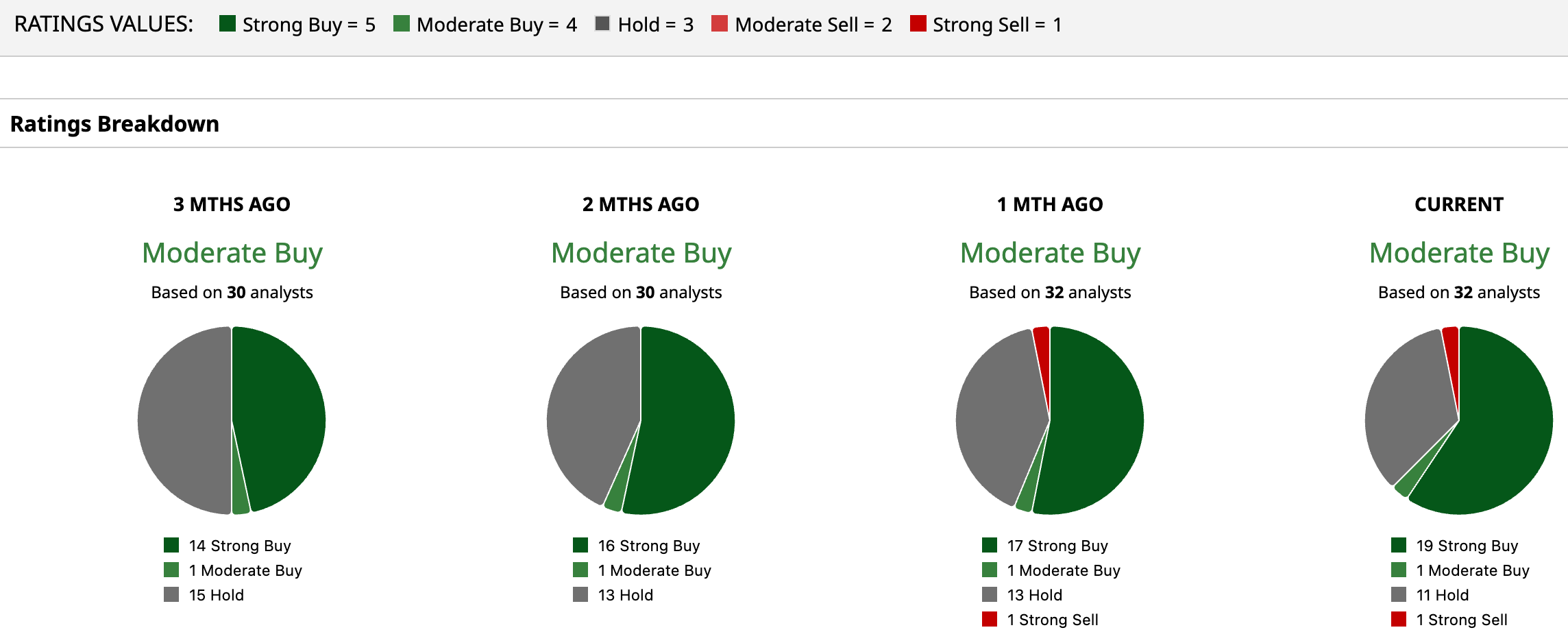

The consensus rating on CRWV stock remains at “Moderate Buy.” Among 32 analysts covering the stock now, 19 advise a “Strong Buy,” one suggests a “Moderate Buy,” 11 analysts are playing it safe with a “Hold” rating, and the remaining one analyst remains skeptical with a “Strong Sell.”

Even with the stock sliding, analysts are bullish. The stock has already surpassed the average price target of $117.43, and the Street-high target of $180 suggests that the stock could rise as much as 52.8%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)