/CPU%20Chip.jpg)

Just like Nvidia (NVDA), in terms of AI chips, hogged most of the limelight, leaving the likes of AMD (AMD) in its shadows, the domain of memory chips has seen a similar story play out. With Micron (MU) being the undisputed star, Sandisk's (SNDK) rise has been relatively less celebrated. It should not be.

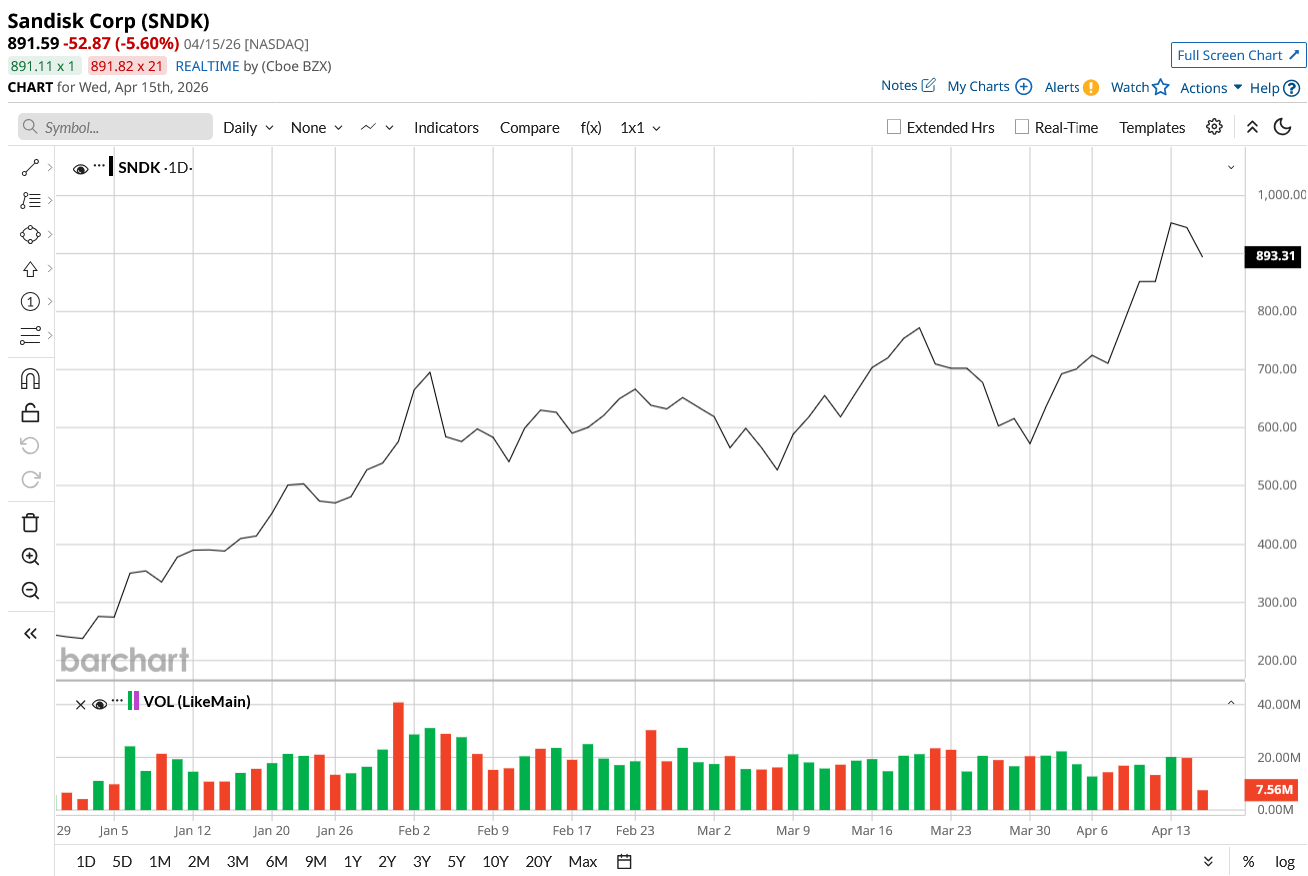

Shares of the memory chip maker are up a whopping 300% this year, with its market cap now at $140.6 billion. Now, reputed broker Evercore is joining the Sandisk bandwagon as well. The firm, initiating coverage on the stock with an “Overweight” rating, has a price target of $1,200 but has a bull case target of $2,600. That'd be 191% higher than its current price.

In a note to clients, analyst Amit Daryanani of the firm said, “We believe SNDK is levered to one of the most attractive areas of the AI infrastructure stack—data storage, where demand is accelerating and supply remains constrained at minimum through CY28 if not beyond. While concerns around peak NAND pricing and cyclicality persist, we think the current cycle is structurally tighter and more durable, underpinned by AI-driven demand and sustained supply discipline that is creating SCAs, providing memory providers with pricing floors and upfront cash payments (Strategic Contractual Agreements between cloud companies and NAND/DRAM providers).”

About Sandisk

Founded in 1988, Sandisk is a semiconductor storage company focused on NAND flash memory. Its core product categories include consumer storage (USB drives, memory cards), client SSDs (laptops, PCs), enterprise/data center SSDs (hyperscale and AI workloads), and embedded storage (smartphones, etc.).

Strategically, Sandisk is shifting its focus from consumer to high-margin enterprise and AI-driven storage demand, a key reason for the recent rally seen in its share price.

So, should investors follow Evercore's suit and make SNDK a place in their portfolios? Let's find out.

Memorable Q2

Since forging its own path after separating from Western Digital, Sandisk's quarterly results have been consistently outperforming Wall Street expectations. Q2 2026 was no different, with the company reporting a beat on both the revenue and earnings front.

Revenues were up 61% from the previous year to $3 billion. The data center and edge segments, servicing the AI sector, saw an annual jump of 64% and 21% to $440 million and $1.7 billion, respectively, as gross margins improved to 51.1% from 32.5% in the year-ago period. Meanwhile, earnings jumped by a fantastic 404% in the same period to $6.20 per share, comfortably outpacing the consensus estimate of $3.62 per share. Notably, this was the fourth consecutive quarter of bottom-line beat from Sandisk.

Net cash from operating activities for the quarter grew to more than a billion dollars from a mere $95 million in the prior year as the company closed the quarter with a cash balance of $1.54 billion. This was considerably higher than the short-term debt of just $20 million on its books.

For Q3 2026, Sandisk expects revenue to be in the range of $4.4 to $4.8 billion, with Street expectations pegged at $4.66 billion for the same metric. In terms of earnings, the same is expected to be in the range of $12 to $14 per share. The Street's EPS expectations are around $14.

Coming to valuations, Sandisk's are not out of whack even after such a strong rally. Its forward P/E of 22.52 is similar to the sector median of 22.46, while its forward P/S and P/CF of 8.82 and 27.14 are just above the sector medians of 3 and 17.38, respectively. Encouragingly, its forward PEG ratio of 0.10 is actually lower than the sector median of 1.39.

Stay Sanguine About Sandisk

Unlike other players in the memory market, like Micron, SK Hynix, and Samsung, Sandisk is solely focused on the NAND market. NAND's nature is more permanent. It is non-volatile and retains information without a power source. It is the fundamental technology behind flash storage. And with a 13% share, Sandisk is currently the third-largest player in this market, which is projected to exceed $75 billion by 2031. Moreover, with its sole focus on NAND, Sandisk is uniquely positioned to be nimble and rapidly gain further market share.

To that end, a major growth driver for Sandisk continues to be the rapid expansion of AI data centers and the related supply agreements it has secured. Notably, the company has locked in several long-term contracts with leading cloud providers. These deals are specifically structured to reduce Sandisk’s exposure to short-term price fluctuations in the memory market. Meanwhile, on the product development side, Sandisk is already shipping its latest high-capacity SSDs and actively working on the next generation of chips, with hyperscalers having recently completed qualification of the new 128 TB Stargate QLC SSD. In parallel, the company is collaborating with SK Hynix on a high-bandwidth flash cell designed specifically for AI inference applications, aiming for up to a 10x improvement in density.

The firm is simultaneously penetrating the automotive storage sector with the iNAND AT EU752 UFS4.1 embedded drive, providing one-terabyte capacities tailored for vehicles enabled with software. Furthermore, the company is capturing demand for mobile processing by shipping UFS 5.0 evaluation samples capable of 10.8 gigabytes-per-second transfer rates for mobile edge computing. Also, strategically, the organization is positioned for a potential merger of equals with Kioxia following the recent public offering of the latter. Such consolidation would combine fabrication facilities and research capital, potentially establishing the combined entity as the market leader in total bit-volume production among established competitors.

Overall, these initiatives should allow Sandisk to strengthen its position in the high-performance storage segment that is being fueled by the ongoing AI infrastructure buildout.

Analyst Opinion on SNDK Stock

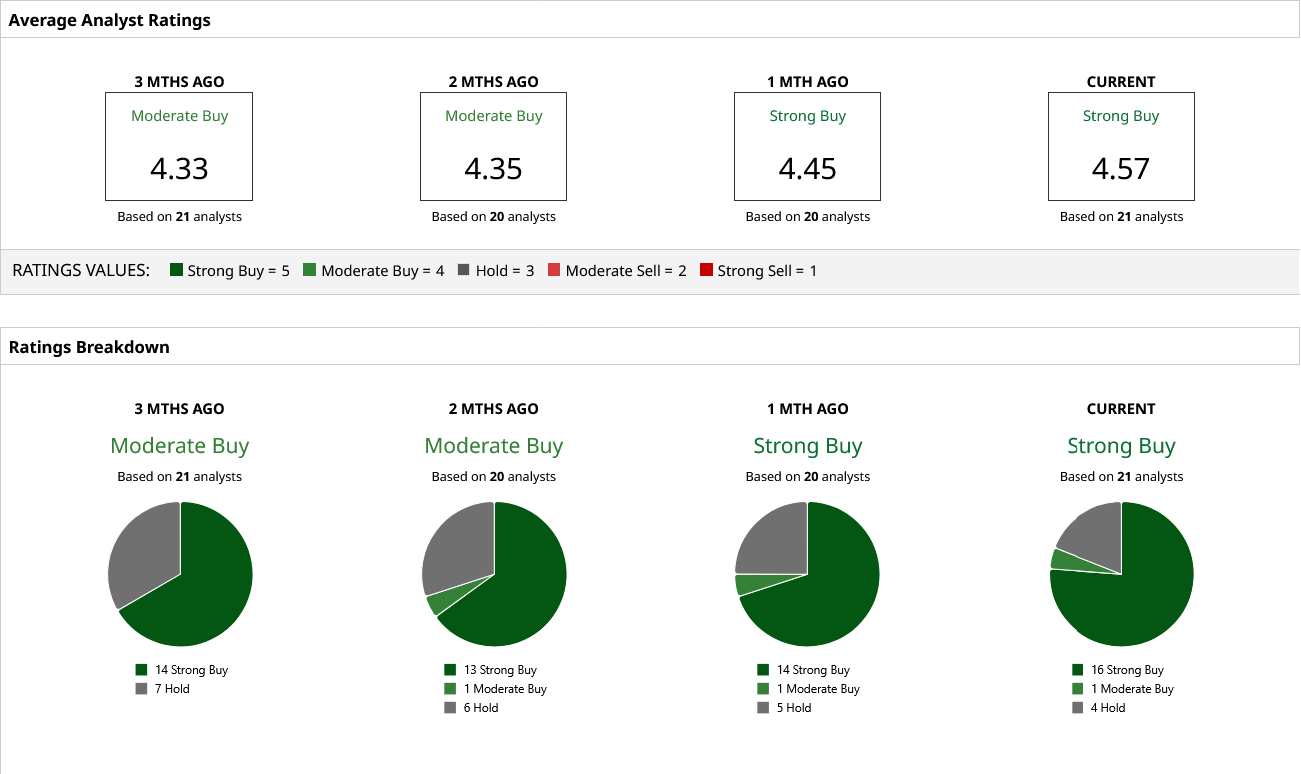

Thus, analysts have earmarked an overall rating of “Strong Buy” for SNDK stock with a mean target price that has already been surpassed. The high target price of $1,800 (not including Evercore's bull case target) indicates an upside potential of about 102% from current levels. Out of 21 analysts covering the stock, 16 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and four have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)