Valued at a market cap of $7.4 billion, Conagra Brands, Inc. (CAG) is a prominent packaged food company with a diversified portfolio of well-known brands across frozen meals, snacks, and pantry staples. Based in Chicago, Illinois, its core business is split between Grocery & Snacks and Refrigerated & Frozen segments, which together drive the majority of sales. The company focuses on brand innovation, cost efficiency, and expanding in higher-growth categories like frozen convenience foods and snacks.

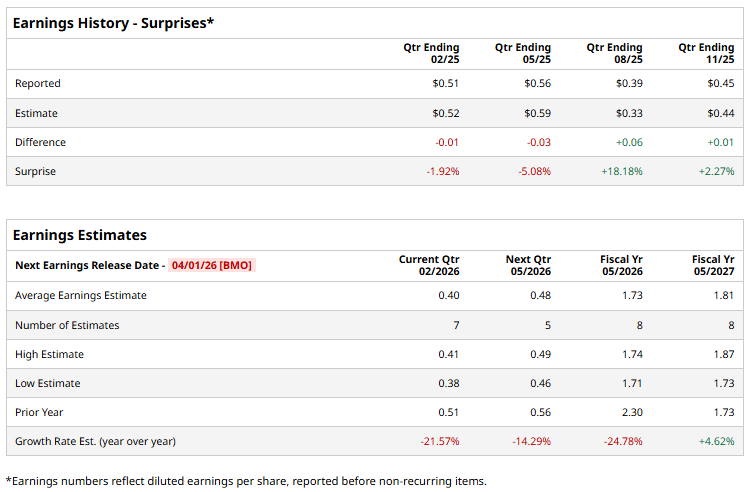

It is scheduled to announce its fiscal Q3 earnings for 2026 before the market opens on Wednesday, April 1. Ahead of this event, analysts expect this packaged foods company to report a profit of $0.40 per share, down 21.6% from $0.51 per share in the year-ago quarter. The company has surpassed Wall Street’s bottom-line estimates in two of the last four quarters, while missing on two other occasions. In Q1, CAG’s EPS of $0.45 exceeded the forecasted figure by 2.3%, thanks to solid demand and macroeconomic tailwinds.

For the current fiscal year, ending in May 2026, analysts expect CAG to report a profit of $1.73 per share, down 24.8% from $2.30 per share in fiscal 2025. Nonetheless, its EPS is expected to rebound and grow 4.6% year over year to $1.81 in fiscal 2027.

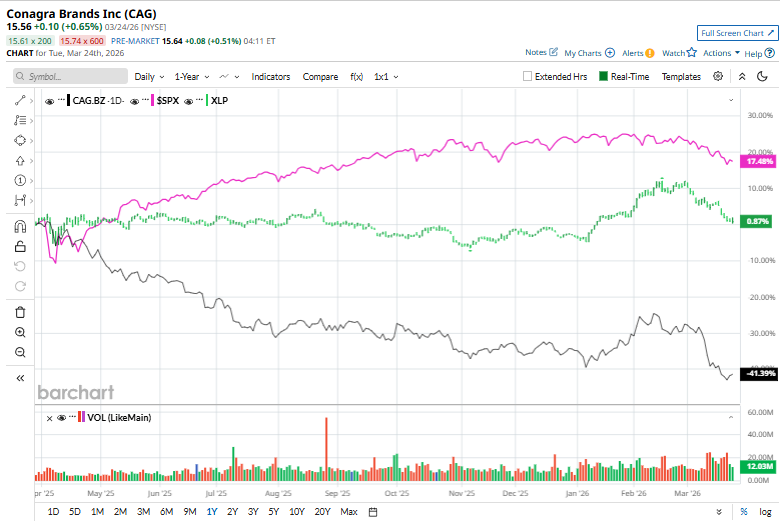

CAG has declined 39.5% over the past 52 weeks, considerably lagging behind both the S&P 500 Index's ($SPX) 13.7% return and the State Street Consumer Staples Select Sector SPDR ETF’s (XLP) 2.2% uptick over the same time period.

Conagra Brands has underperformed the broader market over the past year due to a combination of weak sales volumes, margin pressures, and a cautious growth outlook. The company has struggled with declining demand as consumers shift toward cheaper private-label alternatives, while persistent input cost inflation and supply chain challenges have weighed on profitability. Additionally, muted revenue guidance and mixed earnings results have dampened investor sentiment, reinforcing its positioning as a slow-growth consumer staples player in a market that has favored higher-growth sectors.

Wall Street analysts are cautious about CAG’s stock, with an overall "Hold" rating. Among 16 analysts covering the stock, two recommend "Strong Buy," 11 suggest "Hold,” one indicates a “Moderate Sell,” and two advise a "Strong Sell” rating. The mean price target for CAG is $18.73, indicating a 20.4% potential upside from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)