Warren Buffett, known as the “Oracle of Omaha,” has built his fortune by identifying high-quality businesses and holding them for decades. When Buffett buys a stock, investors pay attention. And when he refuses to sell it for more than three decades, investors want to know why. One such long-standing investment in the Berkshire Hathaway (BRK.B) (BRK.A) portfolio is The Coca-Cola Company (KO), a stock he first bought in the late 1980s and has continued to hold for more than 30 years.

So, why has Buffet held KO stock for so long?

The Power of Compounding at Work

In the late 1980s, Buffett started building Coca-Cola position in Berkshire Hathaway's portfolio and continued purchasing shares thereafter. Meanwhile, the market was still engulfed in the shock of the 1987 stock market crash and investors were hesitant to buy consumer stocks. Today, Berkshire owns approximately 400 million Coca-Cola shares. Importantly, Buffett frequently says that his favorite holding period is "forever." And this investment philosophy works perfectly when you let compounding do its work.

In fact, the power of compounding works best when it is an exceptional business with a competitive edge, such as Coca-Cola. The company holds one of the world's most well-known brands, a global distribution network that is nearly impossible to replicate, and a product that consumers repeatedly purchase regardless of economic conditions.

Over the years, Coca-Cola’s core business model has remained unchanged. Since 1980, KO stock has appreciated enormously, returning over 28,000% if dividends were reinvested. While capital appreciation remains a sole reason for Buffet still holding the stock, Coca-Cola’s dividend streak remains another powerful reason. So, while the stock appreciated, so did the dividend income, as Coca-Cola has consistently raised its payout for 64 years in a row. The company has earned the title of both a Dividend Aristocrat and a Dividend King. Today, Berkshire Hathaway’s position in KO stock roughly generates $848 million yearly in cash dividends.

A Business that Continues to Grow Through Every Economic Cycle

Today, Coca-Cola has evolved into a much bigger and diverse global business. While it still holds its flagship cola business, it is now a global beverage powerhouse with 32 brands worth at least $1 billion each spanning water, sports drinks, tea, coffee, juice, and dairy products. Additionally, Coca-Cola's payouts are still intact and growing, highlighting the company's resilience in different economic cycles.

In its most recent first quarter, despite the persistent inflation, macroeconomic uncertainty, and volatility related to conflict in the Middle East, Coca-Cola still delivered 3% global volume growth. The company's flagship Coca-Cola brand continued to benefit from innovation during the quarter, including the Coca-Cola Cherry Float, Diet Coke Cherry, and Mr. Pibb extensions, which were meant to capitalize on increased customer interest in cherry-flavored beverages. The company’s pricing power is a key competitive advantage. Strong brand loyalty has enabled Coca-Cola to increase prices while maintaining steady consumer demand. Thus, adjusted organic revenue increased 10% in Q1, with a 12% increase in net revenue to $12.5 billion. Adjusted earnings also increased by 18% to $0.86 per share.

Coca-Cola's stability stems from its continued global expansion. Over the past year, it has added more than 600,000 outlets globally, increasing consumer access to its products. Buffett has always prioritized companies that generate significant cash flow, and Coca-Cola continues to showcase this strength. It generated $1.8 billion in free cash flow and plans to generate $12.2 billion for the full year. This will allow Coca-Cola to continue investing in the business, return capital to shareholders, and maintain its long history of dividend increases.

The beverage giant offers a forward dividend yield of 2.6%, higher than the S&P 500. The forward payout ratio of 65% also remains sustainable, given the company continues to generate stable earnings and robust cash flows. Looking ahead, for the full year, management expects organic revenue growth of 4% to 5%, while comparable EPS could grow by 8% to 9%. For a company of this scale, these growth numbers remain impressive.

This Is Why KO Is Buffett's Forever Stock

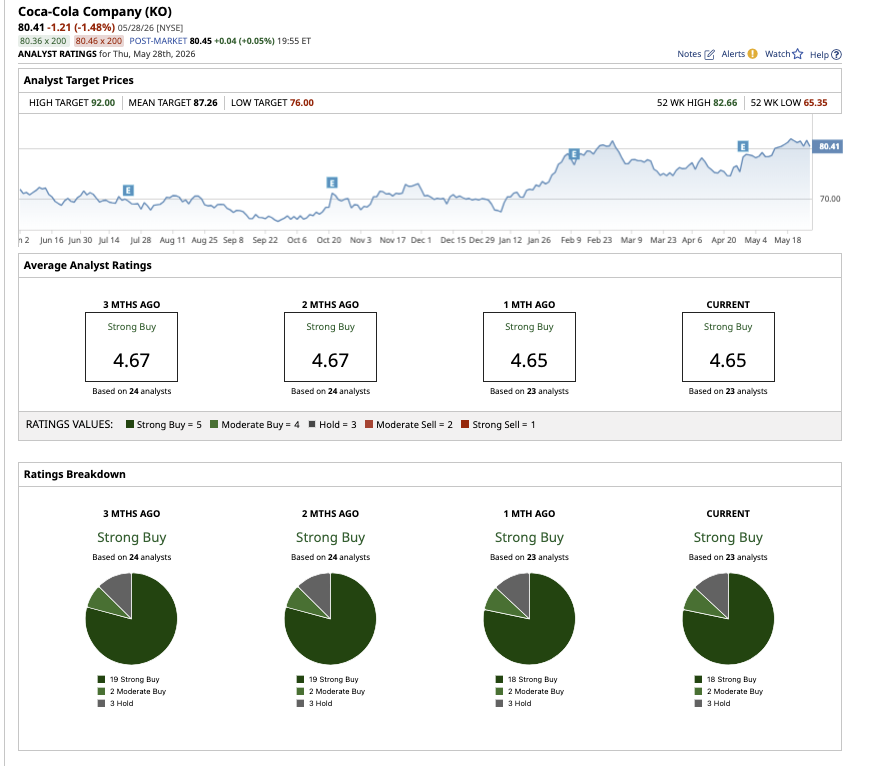

Ultimately, it has been nearly 40 years that Buffet first invested in KO stock. But the company still retains the same qualities that appealed to Buffett in the first place. Powerful brands, global reach, pricing power, strong cash generation, and durable competitive advantages are all the qualities that exceptional businesses carry. This explains why Buffett has never felt compelled to sell KO stock and also why analysts rate the stock a consensus “Strong Buy.”

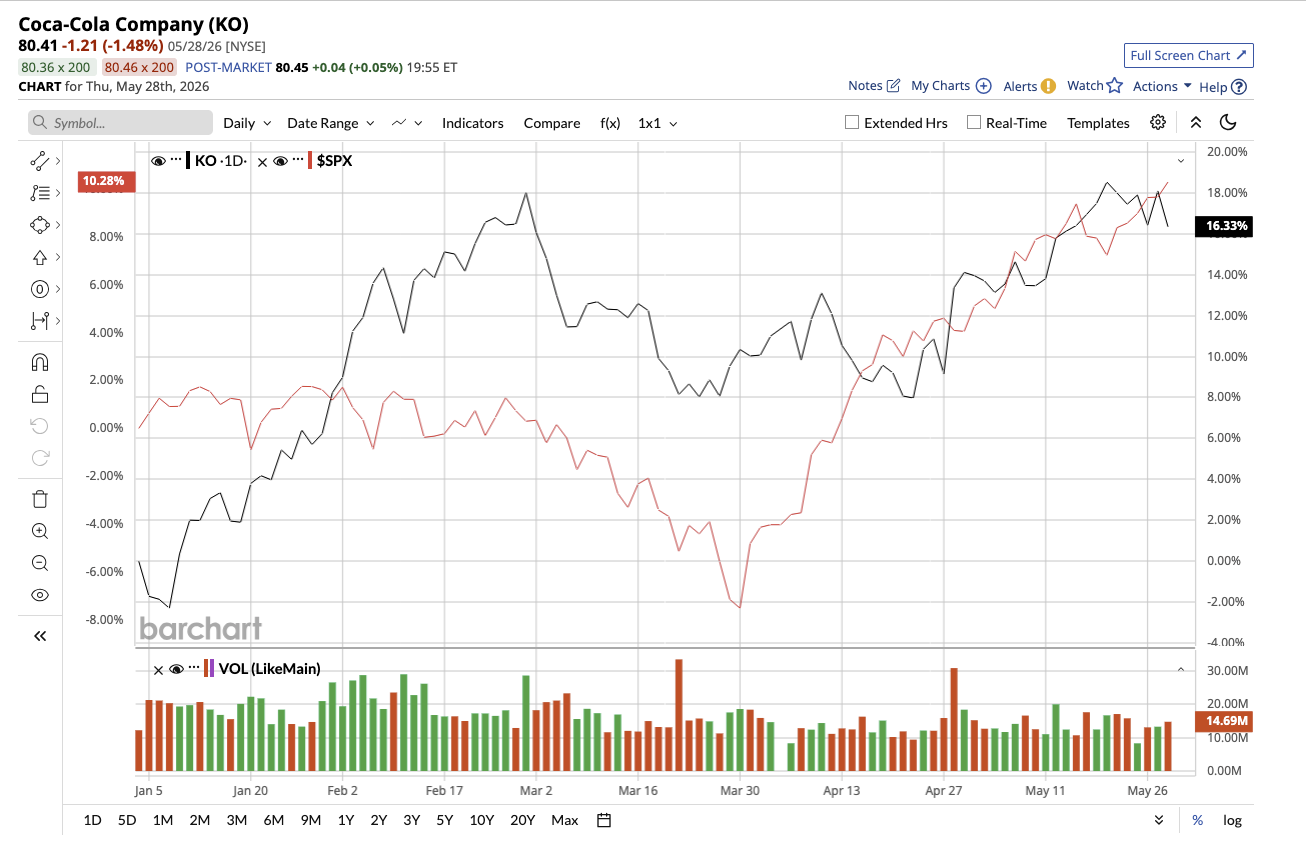

Out of the 23 analysts covering KO, 18 rate it as a "Strong Buy," two as a “Moderate Buy,” and three as a “Hold.” KO stock has climbed 13.7% year-to-date, outpacing the broader market. The mean target price for KO is $87.26, which is 10.4% above current levels. Its high target price of $92 implies potential upside of 16.4% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)