/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

Despite persistent fears that AI demand might be cooling, fresh earnings from Nvidia (NVDA) Broadcom (AVGO), and others underscore that the AI boom shows no signs of slowing.

Nvidia posted record fiscal fourth-quarter 2026 revenue of $68.1 billion, up 73% year-over-year (YOY). Powered by AI, its data-center segment surged 75% to $62.3 billion. Broadcom similarly delivered explosive AI growth, with AI revenue more than doubling to $8.4 billion and executives projecting over $100 billion in AI chip sales by 2027. These beats confirm hyperscalers and tech giants continue to pour billions into AI infrastructure.

In another powerful validation of sustained demand, Taiwan Semiconductor's (TSM) new Arizona Fab 4 facility is already fully booked through late 2027 — before construction has even started.

Unwavering AI Momentum

Taiwan Semiconductor itself delivered blockbuster results that mirror the broader AI surge. For full-year 2025, revenue climbed 36% to $122 billion while EPS soared 51% to $10.65, driven by 3-nanometer (3nm) and 5nm chips fueling AI servers and high-performance computing. Q4 2025 profit jumped 35% to a record, and the company is now guiding for nearly 30% revenue growth in 2026 — outpacing many analyst forecasts — while ramping capital spending to as much as $56 billion.

Early 2026 data reinforces the trend. January and February revenue rose nearly 30% YOY on relentless AI orders. Advanced nodes (7nm and below) already account for 77% of wafer revenue, positioning TSM as the indispensable foundry for the AI era.

Customers Willing to Pay a Premium for U.S. Capacity

Even more telling is the scramble among TSM’s biggest clients — Apple (AAPL), Advanced Micro Devices (AMD), Broadcom, Nvidia, and Qualcomm (QCOM) — for guaranteed U.S.-based supply. These companies have explicitly asked Taiwan Semiconductor to expand Arizona production despite quotes that run 25% to 30% higher than in Taiwan.

CEO C.C. Wei confirmed the requests, noting that U.S. customers are “providing strong signals” and willingly paying up to secure capacity amid geopolitical risks and potential tariffs on Taiwan-made chips. This willingness to absorb higher costs highlights how critical advanced semiconductors have become; supply security now trumps price for AI leaders and smartphone giants alike. TSM emerges as one of the clearest beneficiaries of AI’s continued expansion, with locked-in orders insulating future revenue streams.

Strong Gains and Attractive Valuations

Investors have taken notice. TSM stock is up approximately 12% year-to-date (YTD), trading around $344 despite periodic volatility tied to broader market swings. The forward price-to-earnings (P/E) ratio sits at roughly 22.9 times, the trailing P/E around 30.9 times, and EV/EBITDA near 16 times — premium multiples, but justified by 25% to 30% projected growth and 56% gross margins.

Compared with historical averages and peers, these metrics still offer compelling value for a company dominating the leading-edge foundry market. The dividend yield hovers near 1%, and robust free-cash-flow generation supports both expansion and shareholder returns, making TSM stock an attractive long-term holding even after recent gains.

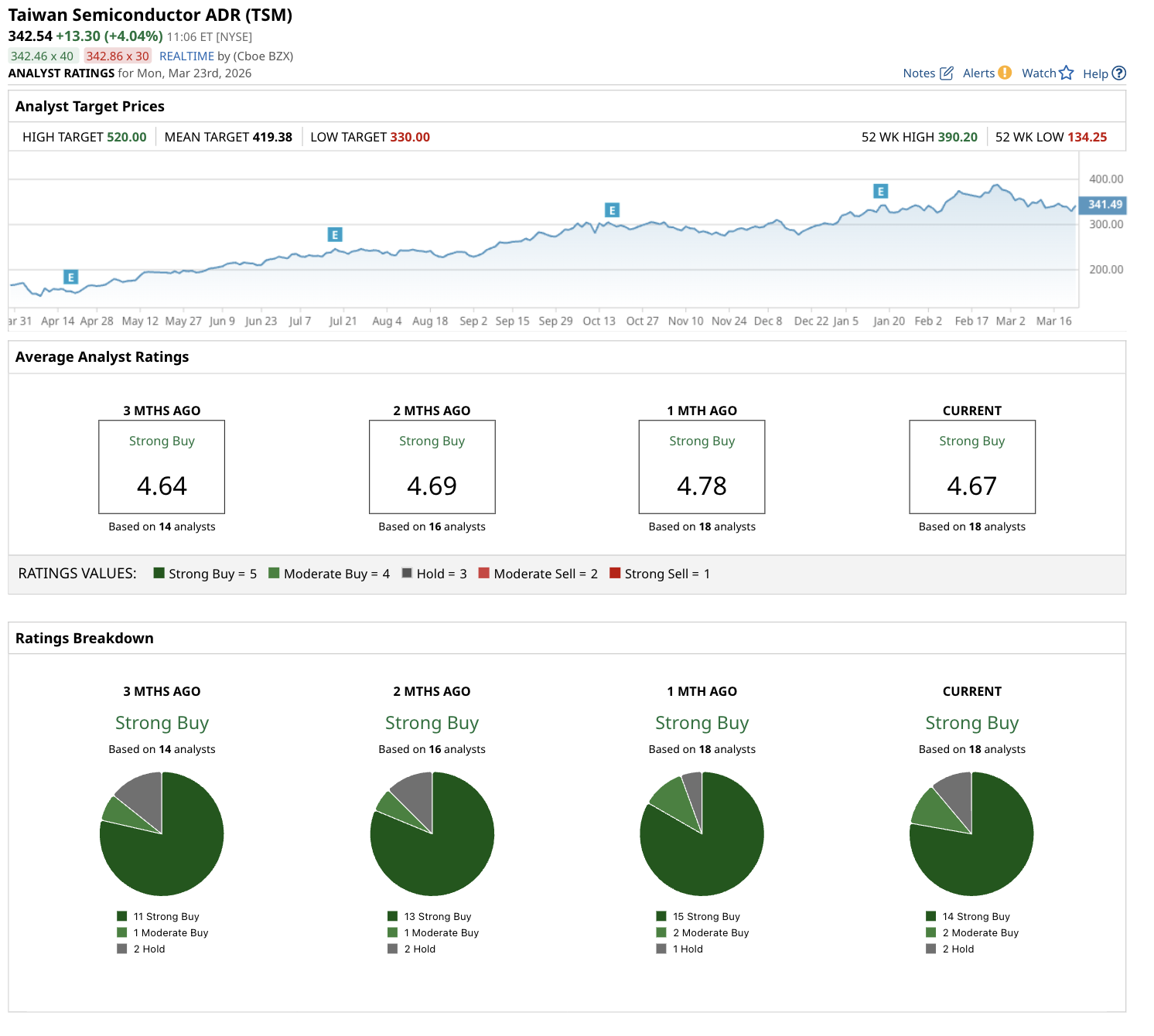

Wall Street’s Bullish Outlook on TSM Stock

Analysts overwhelmingly agree. Barchart data shows a consensus “Strong Buy” rating from 18 analysts. The mean price target stands at $419.38, implying potential upside of roughly 22% from current levels, while the highest price forecast is $520 per share.

Firms cite TSM’s AI exposure, capacity discipline, and geopolitical diversification as reasons for sustained optimism. Only two analysts rate the stock as a "Hold" and none say "Sell," reflecting broad confidence that the company’s 2026 growth targets remain achievable.

The Bottom Line

The fact that TSMC’s newest Arizona Fab 4 is sold out through late 2027 — before breaking ground — speaks volumes about the intensity of current and future demand. It locks in premium-priced U.S. production years ahead, reduces geopolitical risk for key customers, and guarantees revenue visibility for TSM well into the decade. Capacity constraints that once worried investors now look like a feature, not a bug, as the foundry leader converts insatiable AI appetite into durable earnings power.

For investors, this pre-sold status cements TSM’s role as the ultimate AI infrastructure play, with implications for sustained margin expansion, market share gains, and continued stock-price appreciation as the semiconductor supercycle rolls on.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)