/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

The growth trajectory in the AI hardware sector goes well beyond graphics cards, with memory suppliers fast becoming Wall Street’s preferred way to play the next leg of buildouts. This was again evident earlier this week when Barclays upgraded Sandisk (SNDK) to "Overweight" and hiked its target price to $2,300, noting that the company's business models could be game changers in the world of memory manufacturing.

In its note on the stock, Barclays analyst Tom O'Malley called memory and storage "the most attractive vertical below accelerators." According to the analyst, the memory industry will continue generating pricing upside due to the supply and demand imbalance that could last until the end of calendar 2027. In reaction, SNDK shares climbed amid the day's premarket session as investors began taking a closer look at both the company's pricing trends and its uniquely structured business model.

About Sandisk Stock

Sandisk Corporation develops flash storage and memory technologies utilized in hyperscale data centers, AI infrastructure, enterprise systems, and consumer products. Headquartered in Milpitas, California, SNDK boasts a market cap of $243 billion as investors rapidly pivot their portfolios toward non-semiconductor AI infrastructure beneficiaries.

SNDK has been a star performer in the market since its breakout began. SNDK shares were last trading at about $1,590, up by a whopping 4,293% from its 52-week low of $36.21. The stock has gained nearly 10% in the last five trading days as the AI hype continues pushing shares of AI-infrastructure linked memory stocks to new heights.

While traditional valuations look rather aggressive, the market seems to justify the premium attached to SNDK due to the rapid earnings growth and AI infrastructure-linked demand prospects. SNDK shares trade at approximately 23.3x forward earnings and 32x sales. These multiples are high relative to the storage sector, but investors now see SNDK as a provider of an AI infrastructure platform.

However, the bigger story might be the company's new approach to its customers via its business models. Barclays emphasized that Sandisk has emerged as the "most aggressive and structurally innovative" company in the space via its New Business Model contracts. The company guarantees customers its supply while, at the same time, creating demand visibility for itself.

Sandisk Reports Strong Results, Announces Major Contracts

On April 30, Sandisk announced exceptional earnings for its third quarter of fiscal 2026. Revenue skyrocketed 97% from the previous quarter, totaling $5.95 billion and beating consensus by a wide margin. GAAP earnings came in at $23.03 per share, while non-GAAP earnings rose to $23.41 per share.

Sandisk's data center division turned out to be the largest contributor. Quarterly revenues for the division grew by 233%, fueled by strong demand for AI-related capacity. The company highlighted that the results were driven by pricing strength and a mix shift in favor of higher-end customers, as it prioritized AI-infrastructure deployments.

Guidance also came much better than anticipated. For the fourth quarter of fiscal 2026, the company projects revenues of between $7.75 billion and $8.25 billion. Additionally, Sandisk sees quarterly EPS rising between $30 and $33 per share.

However, the biggest news came not from quarterly results but rather from the company's contracts. Sandisk reportedly entered into five agreements worth a combined $42 billion in minimum revenues. Furthermore, these contracts last until 2031 and include quarterly purchase commitments that grow with time.

The contracts also featured more than $11 billion in financial assurances, including upfront payments and third-party-backed financial instruments. Barclays argues that these contracts represent some of the most favorable contract structures within the entire AI ecosystem thanks to their reduced risk and improved visibility.

The management team stated that the current quarter represents a "fundamental inflection point" for the company, as the new structure provides SNDK with more structurally higher and resilient earnings supported by multi-year AI infrastructure demand.

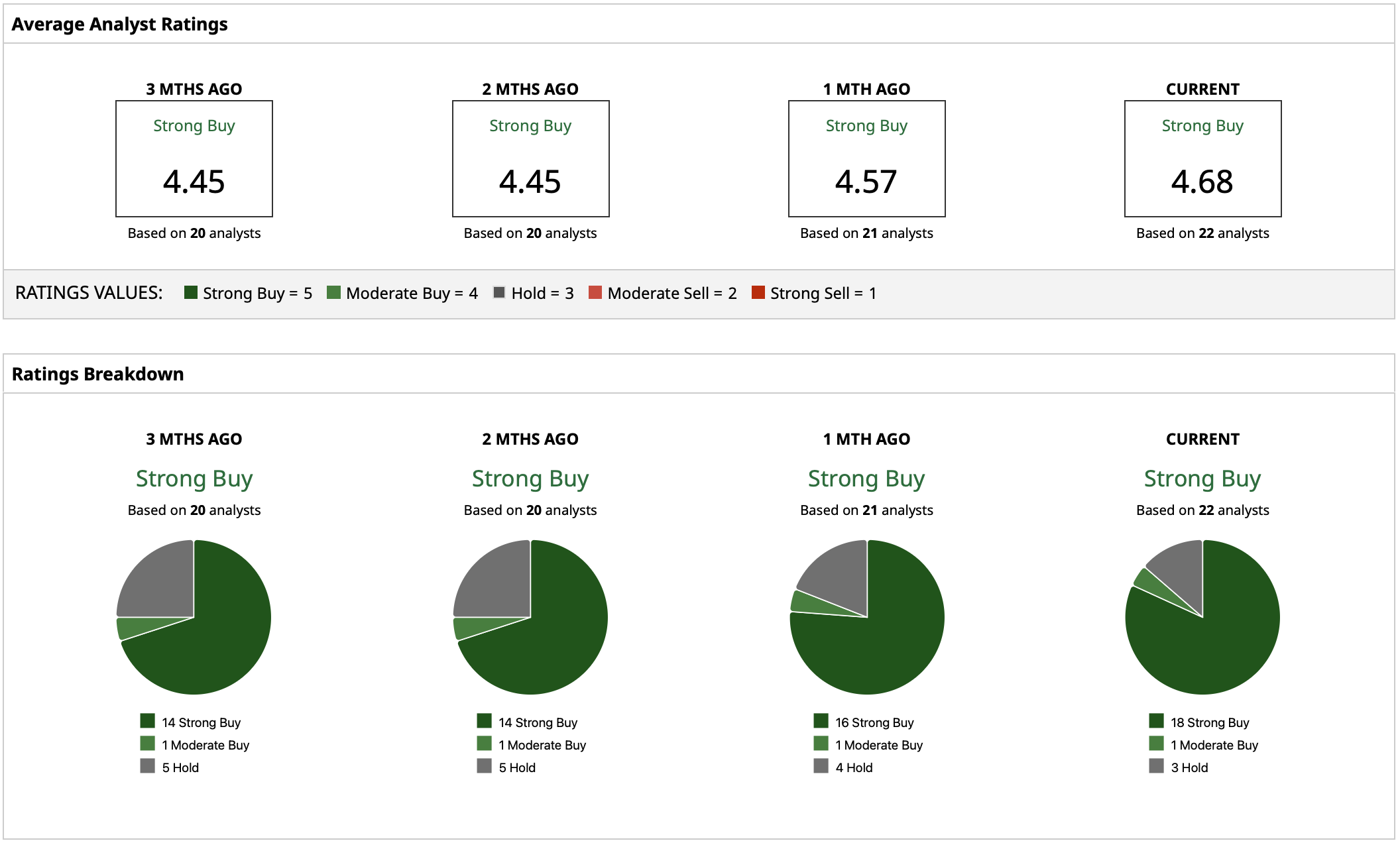

Analyst Ratings and Price Targets for SANDK Stock

The sentiment toward SNDK remains very strong as AI-infrastructure demand expands into memory/storage with a “Strong Buy” rating consensus. The latest boost to the stock comes from Barclays, which increased its price target on the company's stock to $2,300 and upgraded it to "Overweight." Analysts maintain an average price target for SNDK of just under $1,634. Meanwhile, the street-high target stands at $2,590. Even following its massive run, Wall Street still considers SANDK as one of the best leverage opportunities on the AI data center and memory demand.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)