Dividend stocks offer investors something that growth stocks don’t. While most growth stocks may appreciate your capital, they are equally risky during market downturns. The market has been volatile since the U.S.-Iran war began, with the S&P 500 Index ($SPX) down by 4% year-to-date (YTD). In such times, dividend stocks offer some respite by paying consistent passive income. And what's better than Dividend Kings, companies that have a track record of not only paying dividends but also increasing the payouts for 50 years in a row?

Two standout Dividend Kings are Procter & Gamble (PG) and Johnson & Johnson (JNJ). Both are global leaders in defensive industries and have rewarded shareholders with steady and growing income for generations.

Dividend Stock #1: Procter & Gamble (PG)

Procter & Gamble is a symbol of reliability and consistency when it comes to dividend payments. Since 1890, it has paid dividends for 135 years in a row, including 69 consecutive years of increases. It pays a quarterly dividend of $1.05 per share. Its forward dividend yield of 2.9% is higher than the S&P 500 average of 1.2% and the consumer sector average of 1.9%.

P&G stock has gained 1.2% so far this year, outperforming the broader market.

What makes P&G especially attractive is the predictability of its business. Its portfolio includes everyday essential products such as Tide, Pampers, Head & Shoulders, and Gillette, among others. No matter the economic scenario, customers don’t just stop buying toothpaste, detergent, or diapers. The company’s earnings get a boost from this steady demand.

In the second quarter of fiscal 2026, adjusted free cash flow productivity stood at 88%. This means the company converted 88% of its profits into real cash, highlighting strong earnings quality and dividend sustainability. This usable free cash balance allowed it to pay $2.5 billion in dividends and $2.3 billion in share repurchases in the quarter. Even more impressive is P&G’s intention to pay out $10 billion in dividends along with $5 billion in share repurchases for the fiscal year. Additionally, P&G maintains a reasonable payout ratio of 58%, leaving room for continued dividend growth and reinvestment in the business. In short, P&G is a cash-rich business that rewards shareholders both with steady income and potential capital appreciation.

For long-term investors, P&G provides stable earnings, moderate but consistent growth, and decades of dividend increases.

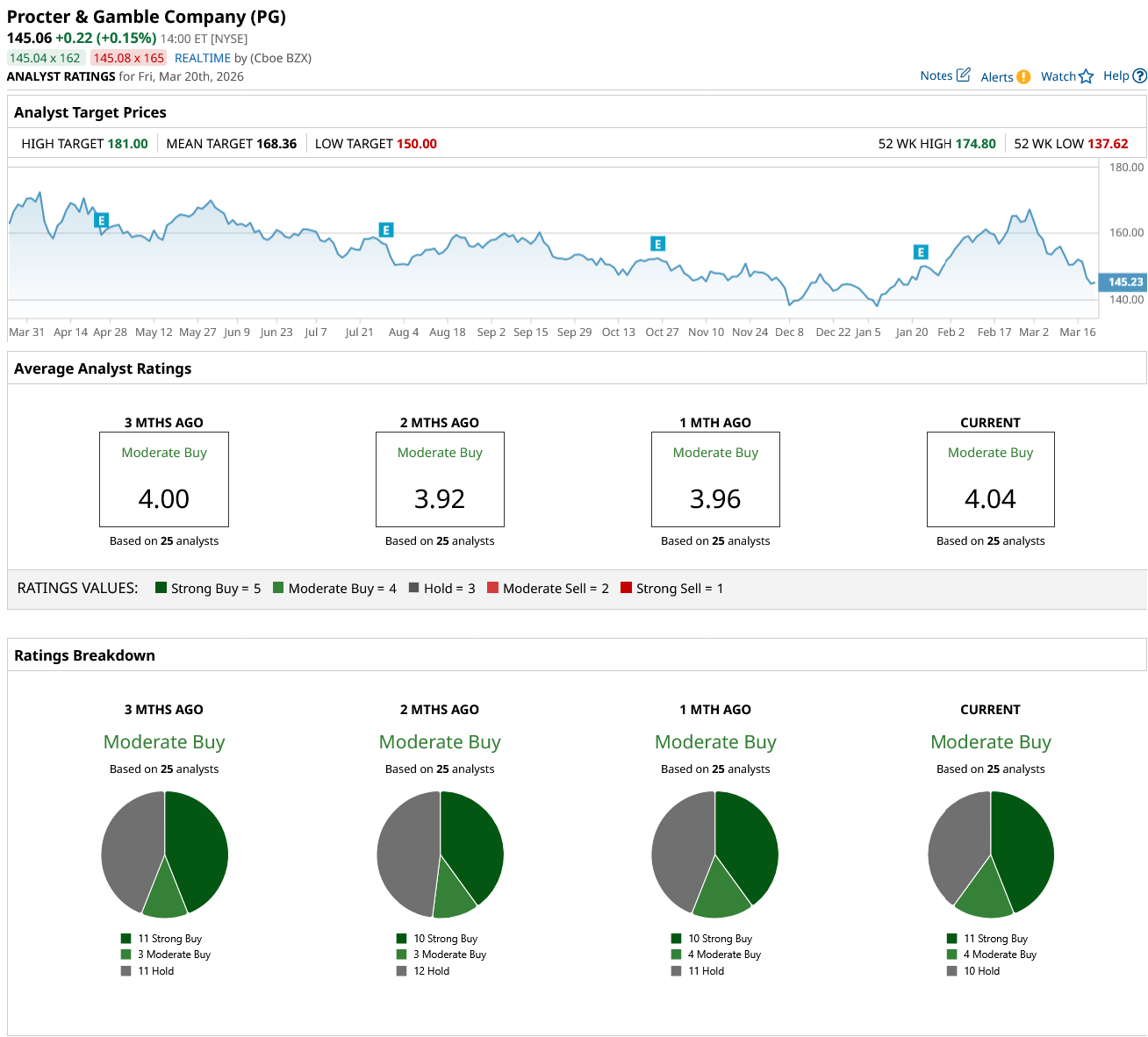

While P&G is not a high-flying growth stock, Wall Street still rates the stock a “Moderate Buy” due to its strong dividend profile. Of the 25 analysts who cover the stock, 11 rate it as a "Strong Buy," four as a "Moderate Buy," and 10 as a "Hold." The average target price for PG stock is $168.36, or 16% higher than current levels. Furthermore, its high target price of $181 suggests a potential 25% increase over the next 12 months.

Dividend Stock #2: Johnson & Johnson (JNJ)

Johnson & Johnson is another defensive stock for long-term passive income investors. It offers the same stability as P&G, but in healthcare. J&J has a dividend growth streak of over 64 consecutive years.

While most high-flying tech stocks have fallen this year, JNJ stock has gained 1.4% YTD.

Like consumer products, healthcare products remain constantly in demand, regardless of the economic scenario. With its core business now entirely focused on pharmaceuticals and medical technology, J&J benefits from long-term demand generated by aging populations and global healthcare needs.

What sets J&J apart is its diversified revenue base. Its MedTech segment offers stable, recurring revenue. Meanwhile, the Innovative Medicines segment is a high-margin growth driver. This diversification provides a cushion from sector-specific risks while still allowing it to grow earnings over time. Its forward dividend yield of 2.19% is higher than the healthcare average of 1.6%. It pays a quarterly dividend of $1.30 per share.

J&J’s robust balance sheet and consistent cash generation have enabled it to raise dividends through multiple economic cycles, including recessions and healthcare disruptions. The company generated $19.7 billion in free cash flow in 2025, allowing it to retain a 51% dividend payout ratio. In 2026, the company expects to generate $21 billion in free cash flow, which will let it pay and increase dividends.

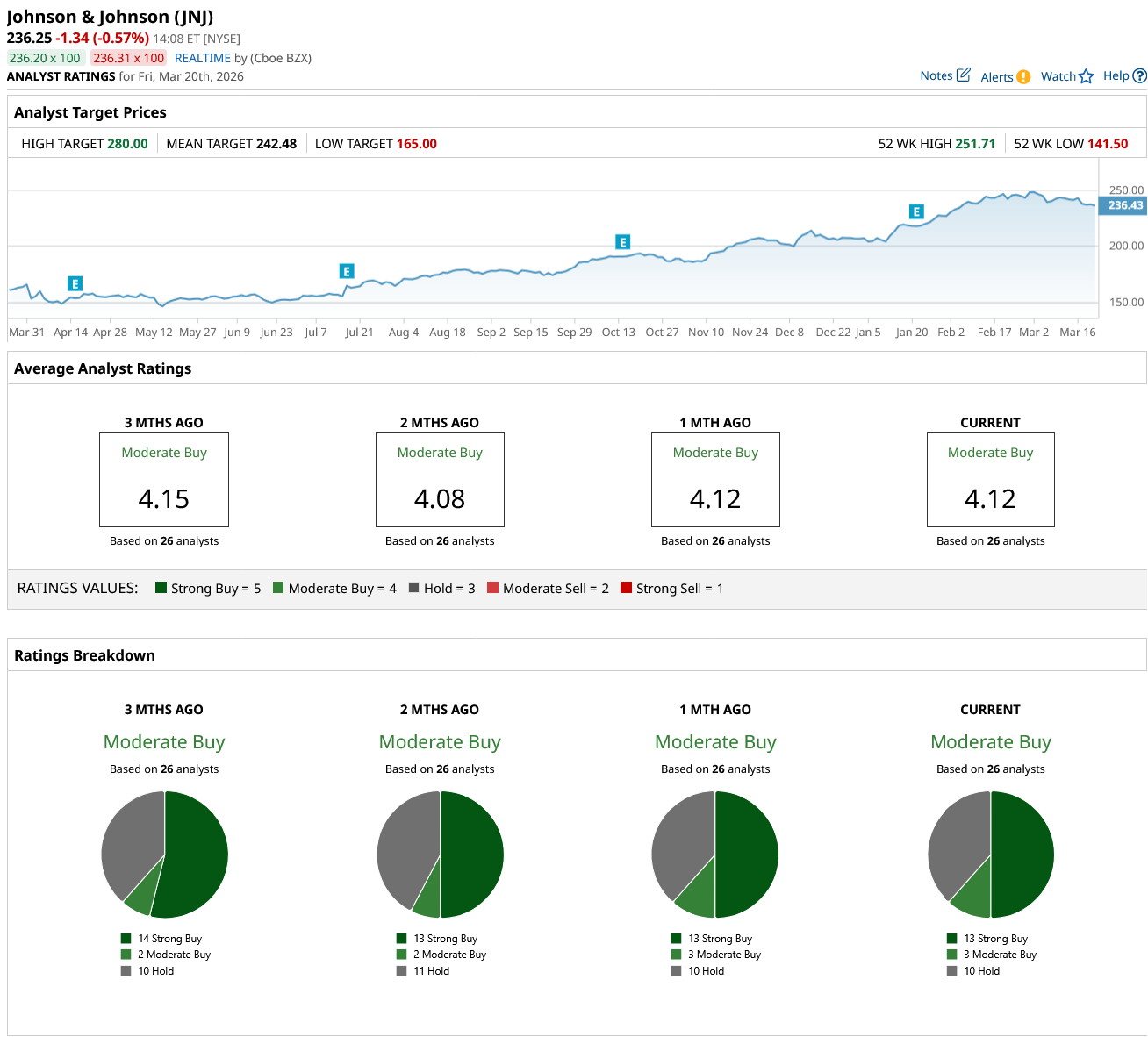

The consensus rating on JNJ stock is a “Moderate Buy.” Out of the 26 analysts covering the stock, 13 rate it a “Strong Buy,” three rate it a “Moderate Buy,” and 10 rate it a “Hold.” JNJ’s mean target price of $242.48 suggests the stock can go up by 3% from current levels. However, its high target price of $280 implies potential upside of 19% in the next 12 months.

If you’re looking for stocks you can confidently buy, hold, and forget about for decades, Procter & Gamble and Johnson & Johnson are among the best options available.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)