/Super%20Micro%20Computer%20Inc%20logo%20on%20building-by%20Poetra_RH%20via%20Shutterstock.jpg)

Super Micro Computer (SMCI) recently reported one of the biggest quarters in its 32-year history. Last week, the server maker launched a new product line that could positively impact its profit margins. The question investors are wrestling with now: Does any of this make SMCI stock worth owning?

Here are some numbers that deserve a closer look before you put money to work.

SMCI Doubles Its Top Line

In its fiscal second quarter ended Dec. 31, 2025, Supermicro reported revenue of $12.7 billion, up 123% year-over-year (YoY).

The company blew past its initial revenue forecast of between $10 billion and $11 billion. A significant portion of that upside came from $1.5 billion in shipments delayed from the prior quarter.

Supermicro President and CEO Charles Liang guided for at least $12.3 billion in revenue for the current quarter and raised the full-year outlook to at least $40 billion, a target described as "relatively conservative."

The key growth driver for SMCI stock is AI infrastructure spending. In fiscal Q2, AI-powered GPU platforms accounted for more than 90% of total sales. Notably, a single large data center customer accounted for 63% of total quarterly revenue.

However, Supermicro's non-GAAP gross margin came in at just 6.4% in Q2, down from 9.5% the prior quarter.

The company is shipping mostly to massive, price-sensitive data center customers.

Those customers have pricing leverage, while new platform ramp costs, supply chain shortages in memory and storage, and elevated freight costs all impacted the bottom line simultaneously.

Non-GAAP diluted earnings per share of $0.69 beat guidance of $0.46 to $0.54, driven by higher-than-expected sales. Liang was direct on the call: "Customer mix, we are improving quarter after quarter."

He expects gross margins to expand in the future, citing lower expedite costs as the new GB300 platform matures and a growing contribution from a higher-margin product line called Data Center Building Block Solutions, or DCBBS.

For Q3, Supermicro guided for gross margin to improve by 30 basis points compared to the last quarter.

The Gold Series Launch Targets a Higher-Margin Customer

On April 9, 2026, Supermicro launched its new Gold Series enterprise server solutions. The lineup includes over 25 pre-configured server systems, optimized across four categories: enterprise compute, enterprise AI, enterprise storage, and intelligent edge. Every system ships from U.S. warehouses, generally within three business days.

"By shipping our Gold Series offerings directly to our customers with everything they need to run their enterprise workloads, we make our industry-leading server portfolio available to our customers even faster," Liang said in the statement.

Large data center hyperscalers are the customers squeezing Supermicro's margins. Alternatively, enterprise customers, the mid-market businesses, edge deployments, and AI inference buyers that the Gold Series targets don't carry the same pricing leverage.

Liang confirmed on the Q2 call that diversifying into enterprise accounts is a deliberate strategy, saying, “Our customer diversification is a very important direction to us now.” If enterprise revenue starts climbing as a share of the total, gross margins should follow.

Is SMCI Stock a Buy, Sell, or Hold Right Now?

The bull case is straightforward: Supermicro is growing faster than almost any large-cap technology hardware company, it's investing aggressively in higher-margin products like DCBBS and the Gold Series, and management is guiding conservatively.

The bear case is just as real: gross margins remain under pressure, customer concentration risk is extreme, regulatory issues abound, and supply chain volatility isn't going away overnight. Between fiscal 2025 and 2028, analysts forecast SMCI's revenue to grow 29% annually. However, adjusted earnings are forecast to expand by less than 20% in this period.

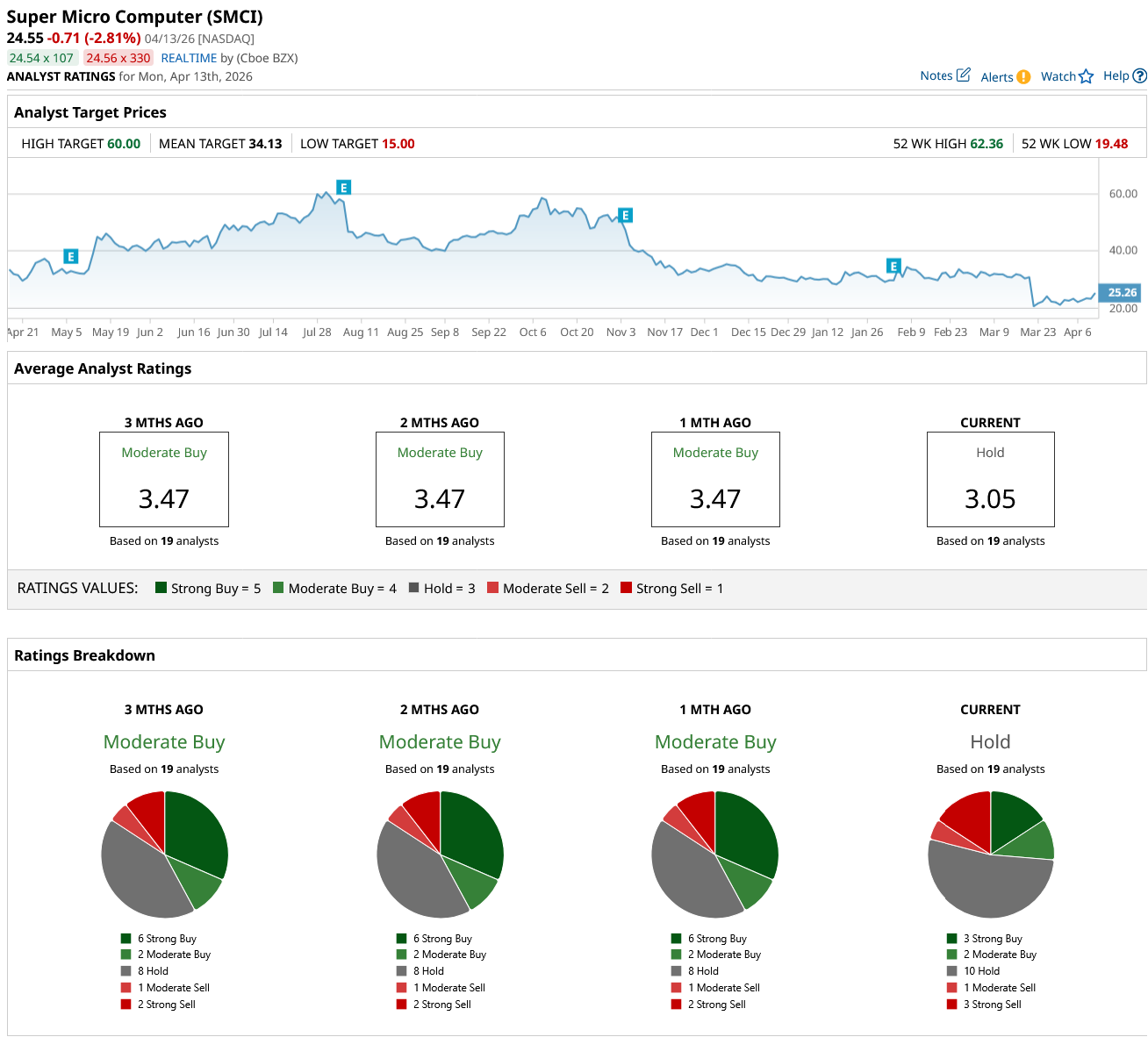

Out of the 19 analysts covering SMCI stock, three recommend “Strong Buy,” two recommend “Moderate Buy,” 10 recommend “Hold,” one recommends “Moderate Sell,” and three recommend “Strong Sell.” The average SMCI stock price target is $34.13, above the current price of $24.55.

For investors with a longer time horizon who believe AI infrastructure spending continues to surge, SMCI at current levels could represent an attractive entry point, especially if the margin recovery story gains traction over the next two quarters.

For investors who need cleaner, more predictable earnings, investing in SMCI stock may require more patience.

The honest answer: SMCI looks like a hold with upside potential, contingent on whether enterprise diversification and DCBBS growth actually show up in the margin line by the end of calendar year 2026.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)