/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Shares of Dell Technologies (DELL) have staged an impressive rally, climbing almost 30% over the past month and emerging as one of the top performers in the S&P 500 ($SPX) during this period. The surge was driven by a robust fourth-quarter earnings report and an optimistic outlook, which have strengthened investor confidence in the company’s growth trajectory.

For fiscal 2026, Dell delivered strong financial performance, with revenue reaching $113.5 billion, marking a 19% year-over-year (YOY) increase. Profitability also improved meaningfully, as EPS rose 27% to $10.30.

A key growth driver for Dell is the accelerating demand for its artificial intelligence (AI) optimized servers. Dell is benefiting from enterprises investing heavily in AI infrastructure, particularly in modernizing data centers and scaling high-performance computing workloads. This structural shift in technology spending is positioning the company to capitalize on the rapidly growing market.

For fiscal 2027, Dell estimates $50 billion in AI revenue, representing more than 100% YOY growth. The outlook is supported by Dell's strong backlog and solid delivery schedules.

Despite the recent rally, Dell’s valuation does not appear overstretched relative to its growth prospects. This suggests that, if execution remains strong and AI-driven demand continues to accelerate, there could still be meaningful upside potential for DELL stock in 2026.

AI Demand Accelerates for Dell, Supporting Further Upside

AI-driven demand continues to accelerate for Dell, supporting its investment case as the company expands its presence in high-performance computing infrastructure. The company is experiencing strong customer traction, reflected in record order volumes and increasingly broad-based demand across its AI solutions portfolio.

In Q4, Dell reported $34.1 billion in AI-related orders, reflecting the rapid pace at which customers are scaling AI deployments. This surge in demand translated into $9.5 billion in AI server shipments during the same period. The company ended the quarter with a record AI backlog of $43 billion, which will support future growth. Notably, Dell’s backlog continued to grow sequentially even after fulfilling a substantial volume of orders, highlighting sustained momentum in customer demand.

For fiscal 2026, total AI-related orders reached $64.1 billion. Dell’s customer base has grown to over 4,000 organizations, including neocloud providers, enterprises, and government-backed entities. This broad mix suggests that AI adoption is expanding across multiple segments.

Looking ahead, Dell expects annual revenue from AI-optimized servers to reach around $50 billion in fiscal 2027, representing a 103% YOY increase. This highlights the company’s strong position to benefit from continued investment in AI infrastructure.

Dell Stock Has Multiple Catalysts

Beyond AI, Dell's diversified portfolio will likely support its growth. The company’s traditional servers, storage, and PC business is witnessing growth. During the last reported quarter, management highlighted that it is gaining market share in the PC business. At the same time, improving margins in traditional servers and storage are cushioning its bottom line.

In the fourth quarter, traditional server demand exceeded supply, driving double-digit growth across regions. Growth was supported by higher unit shipments, an expanding customer base, and increased adoption of high-performance configurations.

Looking ahead, Dell has a solid long-term growth opportunity, as much of its installed base is still on older servers, positioning the company to benefit from enterprises’ spending on IT modernization.

Dell Stock Is Still Undervalued, Signals Growth Ahead

DELL stock appears undervalued, with the company positioned to benefit from strong demand driven by AI. Currently trading at about 13.2 times forward earnings, its valuation looks attractive when compared to analysts’ growth expectations.

Dell’s EPS is projected to rise by 28% in fiscal 2027, followed by another 12% increase in fiscal 2028. This combination of solid growth and a reasonable valuation suggests there could be further upside for Dell stock through 2026.

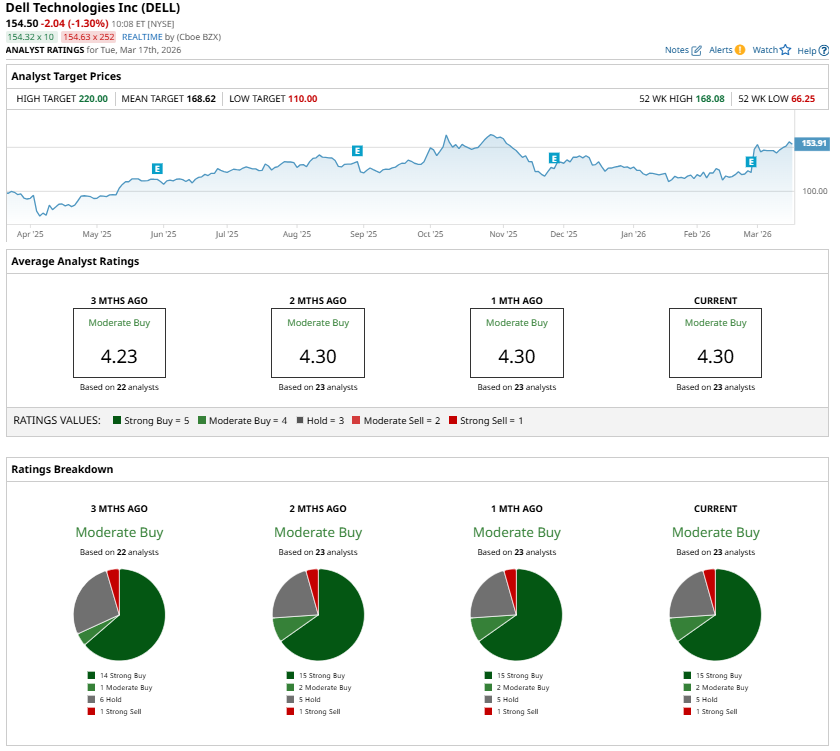

Analysts rate DELL stock as a consensus “Moderate Buy." The highest price target of $220 points to a potential 47% gain from current levels.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Broadcom%20Inc%20HQ%20photo-by%20Sundry%20Photogrpahy%20via%20iStock.jpg)