Tesla (TSLA) certainly remains one of the most debated stocks on Wall Street, with investors frequently split over the company’s future value. While Tesla built its reputation as a pioneer in electric vehicles (EVs), CEO Elon Musk has increasingly been pitching a much bigger vision to investors. In Musk’s view, Tesla is evolving beyond a traditional automaker into an artificial intelligence (AI)-driven technology company focused on robotaxis, autonomy, and robotics.

As a result, many investors are beginning to value the company less as an EV manufacturer and more as a potential leader in the next wave of AI-powered mobility. And that shifting narrative is exactly why Bank of America has once again turned bullish on Tesla. The investment firm recently reinstated coverage of the stock with a “Buy” rating and a $460 price target, describing Tesla as the current leader in consumer autonomy.

According to analyst Alexander Perry, Tesla’s ability to scale its technology efficiently could allow it to dominate the emerging robotaxi market. The analyst noted that autonomous vehicles could spark the next major transformation in transportation, positioning Tesla as a key catalyst in what he calls the “Auto 2.0” era, offering consumers safer travel, time savings, and more accessible transportation. So, with that bullish outlook in mind, should investors scoop up TSLA stock now?

About Tesla Stock

Founded in 2003, Tesla has grown from a niche EV startup into one of the most closely watched companies in the global market. Headquartered in Austin, Texas, Tesla has built a reputation for disrupting the automotive industry with its lineup of EVs, battery technologies, and energy solutions. But Tesla’s story is no longer just about electric cars.

In recent years, the company has been positioning itself as a technology powerhouse, investing heavily in AI, autonomous driving, robotics, and robotaxi services. In essence, the company is attempting to shed its identity as merely a car manufacturer and reemerge as a dominant force in physical AI, robotics, and energy infrastructure. That shift is also reshaping the narrative surrounding Tesla.

In fact, the conversation is no longer centered solely on delivery targets for the Model 3 or Model Y. Instead, attention has moved toward the impending volume production of the Cybercab, the operational integration of the Optimus humanoid robot, and a rapidly expanding energy storage business that is beginning to rival the automotive segment in terms of margin profile.

With a market capitalization now hovering around $1.52 trillion, Tesla remains a key member of the “Magnificent Seven” group of technology giants. Still, the company has faced headwinds in early 2026, including a decline in annual revenue, intensifying competition in the EV market, and growing investor caution around Tesla’s evolving identity as it pivots its business focus.

So far in 2026, shares of Tesla are down about 11.34%, trailing the broader S&P 500 Index ($SPX) which has slipped only slightly over the same period. However, the longer-term picture still looks far more impressive. Over the past year, Tesla stock has surged 51.35%, comfortably outpacing the broader market’s 17.73% gain during the same stretch.

Inside Tesla’s Q4 Earnings Report

Tesla’s fiscal 2025 fourth-quarter earnings report, released in late January 2026, revealed an interesting story of a slowing car manufacturer and a surging energy and AI giant. For the quarter, total revenue slipped 3% year-over-year (YOY) to $24.90 billion, while adjusted EPS fell 17% annually to $0.50. It marked the third revenue decline in three quarters, and notably, full-year 2025 sales fell for the first time in Tesla’s history.

Even so, the results still managed to beat Wall Street expectations, which had called for $24.78 billion in revenue and $0.45 in earnings per share. The weakness largely stemmed from a cooling automotive market. Tesla’s auto sales have slowed in recent quarters as competition intensifies across global markets, particularly from Chinese EV makers. During the quarter, automotive revenue dropped 11% to $17.7 billion, while total vehicle deliveries declined 16% to 418,227 units.

Yet other parts of the business are moving in the opposite direction. Tesla’s energy generation and storage segment surged 25% YOY to $3.84 billion, up from $3.06 billion a year earlier. Meanwhile, the services and other segment grew 18% to $3.37 billion, compared with $2.85 billion last year. Even more striking, Tesla posted its highest gross margin in two years at 20.1%, up from 16.3% a year ago, highlighting improved operational efficiency despite challenges in its core automotive business.

With the EV segment under pressure, Musk has been steering the conversation toward Tesla’s next growth engines. During the earnings call, CFO Vaibhav Taneja said investors should expect roughly $20 billion in capital expenditures this year, aimed at building new factories and expanding investments in Optimus and artificial intelligence computing resources.

In addition, Tesla plans to continue evolving and expanding its product lineup with a focus on cost efficiency, scale, and future monetization opportunities through AI software. According to the company, Cybercab, Tesla Semi, and Megapack 3 remain on track for volume production starting in 2026, while first-generation production lines for Optimus are currently being installed in preparation for eventual mass production.

How Are Analysts Viewing Tesla Stock?

On Mar. 4, shares of TSLA jumped nearly 3.4% after Bank of America took a bullish stance on the company again. Much of BofA’s bullish view on Tesla hinges on the company’s rapidly scaling robotaxi ambitions. Tesla’s robotaxis already operate in San Francisco and Austin, Texas, with plans to expand to seven additional markets in the first half of the year.

Analyst Alexander Perry noted that Tesla’s camera-only autonomous approach is technically more complex but significantly cheaper, allowing the company to scale profitably while gaining a cost advantage over traditional rideshare players. Meanwhile, Tesla’s Optimus humanoid robot segment alone is estimated to be worth over $30 billion. While Bank of America may be firmly bullish, the broader view on Wall Street remains sharply divided when it comes to Tesla.

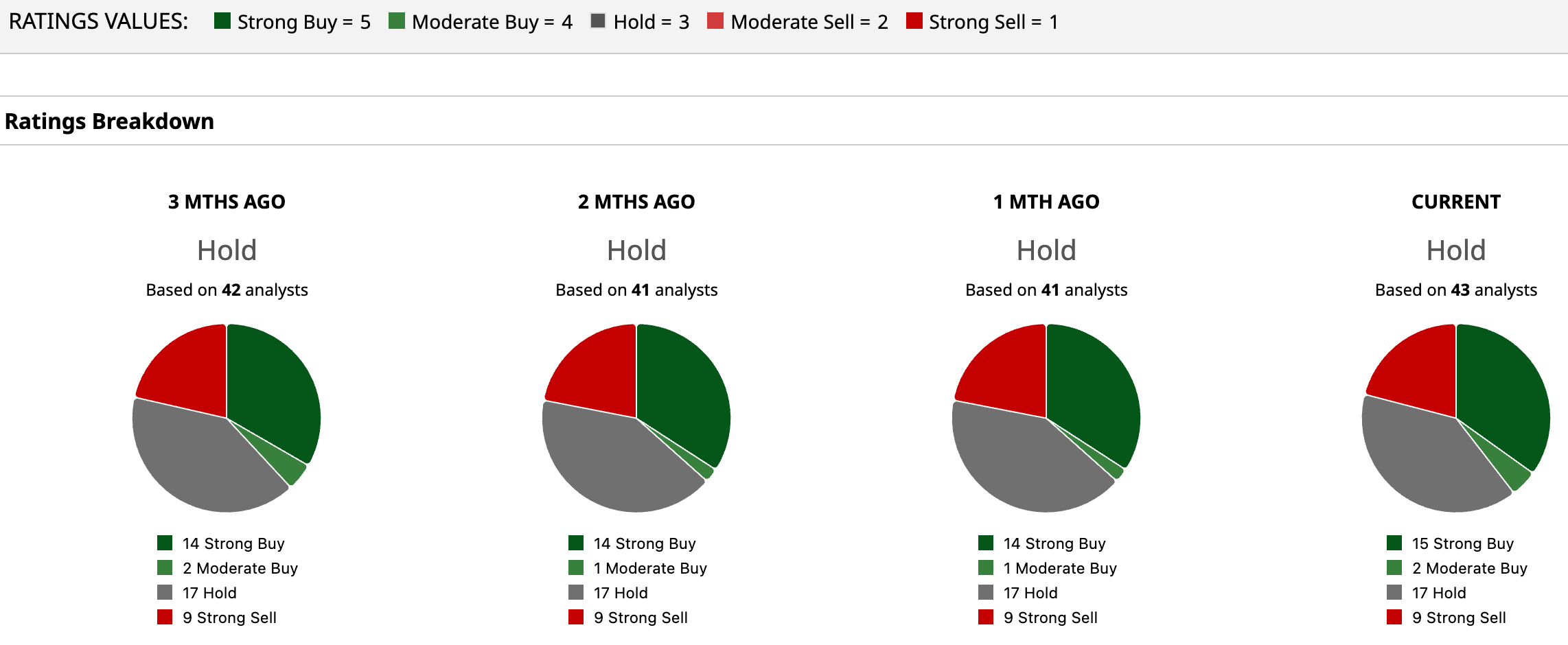

The stock currently carries a consensus “Hold” rating, reflecting the ongoing tug-of-war between Tesla’s long-term growth story and near-term uncertainties. Among the 43 analysts covering the stock, 15 rate it a “Strong Buy,” two recommend a “Moderate Buy,” and 17 prefer to stay on the sidelines with a “Hold.” On the other end of the spectrum, nine analysts maintain a “Strong Sell” rating, highlighting just how polarizing the EV giant remains among market watchers.

TSLA shares are trading only slightly below the average price target of $408.36, suggesting 2.4% upside based on the Street’s consensus view. However, the most optimistic forecasts paint a far more bullish picture. The Street-high price target of $600 implies that the stock could surge as much as 50.45% from current levels, should Tesla’s ambitious bets on AI, robotaxis, and robotics begin to pay off.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)