/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

Defense-focused stocks have been in the spotlight lately as geopolitical frictions and booming AI spending push government and enterprise buyers to upgrade systems. These names can swing sharply on contract news and guidance, rewarding winners that land mission-critical work.

Palantir (PLTR) is one of the highest-profile beneficiaries of that backdrop. The data-analytics firm with deep Pentagon ties reported Q4 2025 revenue of $1.41 billion, up about 70% year-over-year (YoY), helped by a roughly $10 billion U.S. Army AI award and other large defense deals. Plus, its Gotham and Foundry platforms are increasingly embedded in government workflows. Analysts note Palantir’s “entrenchment across critical defense infrastructure” is a key competitive edge.

Yet at the same time, co-founder and Director Peter Thiel filed to sell 2 million shares, about $280 million worth, a move that briefly raised concerns among investors.

For long-term investors weighing Palantir’s lofty multiples against its blowout results and guidance, the question now is whether Thiel’s sale is routine liquidity or a reason to rethink exposure. Let's find out the answer.

Palantir Global AI Integration

Cofounded by Peter Thiel and others in 2003, Palantir Technologies is a U.S. software company specializing in AI-driven data analytics. Today, Palantir sells two core platforms: Gotham for government/intelligence agencies and Foundry for commercial enterprises. Its customers include the Pentagon, the FBI, and big companies in finance and healthcare. Palantir’s government pipeline is robust; for example, the company is closely involved in integrating AI for intelligence on Iran, Ukraine, and other hot spots.

Palantir's stock was one of 2025’s big winners, up 73% over the last year, but 2026 has seen profit-taking. Despite a brief 15% rally over the past week, PLTR is down roughly 12% year-to-date (YTD), as traders pared back after the strong rally. The stock hit record highs in late 2025, fueled by ongoing contract wins, but the recent pullback and broader tech volatility have dragged returns lower.

The one main concern about this stock is its valuation, which could be the biggest reason for the recent selloff. PLTR's price-to-book is 45, much higher than the sector median of 4, indicating a very expensive stock. Similarly, its price-to-sales ratio is 73, compared to the sector median of 3, further highlighting the high valuation. However, bulls argue these multiples price in a continued AI boom and Palantir’s high margins. Bears point out that this pricing leaves little margin for error if growth slows.

Thiel’s Sale Shocks Traders

On March 3, SEC filings revealed Peter Thiel’s planned sale of 2 million shares. Traders noted that Thiel, a longtime chairman and large shareholder, initiated the sale via a trading plan. Many experts say this move is likely routine liquidity management rather than a vote of no-confidence. Historically, Thiel has sold into strength, and he still owns far more shares than he’s selling now. In short, the fundamentals of Palantir’s business remain unchanged; the sale may add short-term volatility and draw headlines, but analysts view it as Thiel unlocking value, not an omen of trouble.

Investors have been watching Palantir through a bigger lens. Notably, earlier this week, PLTR stock climbed on defense tailwinds; it surged on news of U.S.-Israeli strikes and war in Iran. Palantir’s AI is reportedly used for battlefield analytics and rapid decision-making. The Thiel filing interrupts this momentum briefly, but many strategists say the Pentagon’s demand for Palantir’s AI tools gives the company a solid growth runway.

Palantir Beats Q4 Earnings Estimate

Palantir Technologies delivered an exceptionally strong quarter when it reported results on Feb. 2, 2026, that showed rapidly expanding demand for its AI-driven software platforms. The company generated $1.407 billion in revenue in the fourth quarter of 2025, representing a 70% YoY increase and comfortably exceeding Wall Street expectations of roughly $1.33 billion.

Growth was particularly strong in the United States. U.S. commercial revenue more than doubled from the prior year, rising 137% to $507 million. Meanwhile, U.S. government revenue climbed 66% to $570 million. Altogether, about 77% of Palantir’s revenue now comes from U.S. customers, up from around 60% a year earlier, highlighting the company’s deep ties to domestic defense agencies and enterprise clients.

Profitability improved dramatically as well. Net income reached $609 million compared with $79 million a year earlier. On an adjusted basis, earnings were about $0.24 per share, well above analyst expectations of $0.17.

Palantir’s cash generation was equally impressive. Operating cash flow totaled $777 million during the quarter, while adjusted free cash flow reached $791 million. The company ended the year with roughly $7.2 billion in cash and equivalents, up from $5.2 billion the previous year.

Contract activity also surged. Palantir secured $4.3 billion in total contract value during the quarter, marking a sharp increase from the prior year. More interestingly, while customer count grew about 34%, revenue per customer increased even faster as clients expanded their use of Palantir’s software to solve more complex problems.

Looking ahead, management issued very ambitious guidance. For the first quarter of 2026, Palantir expects revenue between $1.532 billion and $1.536 billion. For the full year, the company forecasts revenue between $7.182 billion and $7.198 billion, implying growth of roughly 61%. U.S. commercial revenue alone is projected to surpass $3.14 billion, more than doubling YoY.

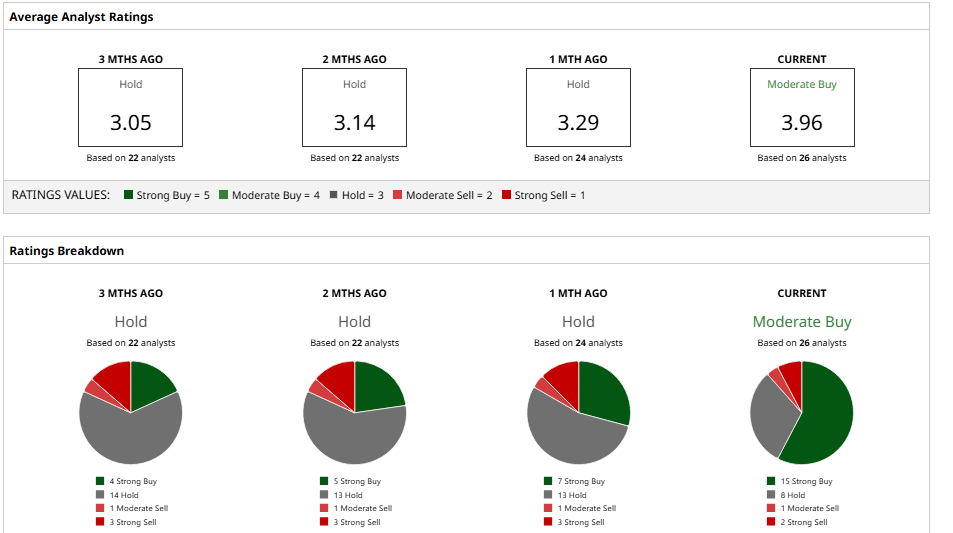

What Do Analysts Think About PLTR Stock

Wall Street's opinion on PLTR stock is mixed, as we have both bulls and bears on the paper. As of now, the average 12-month price target as per Barchart data is around $198, implying roughly 30% upside potential over the current levels.

Some bullish analysts have actually raised targets after Q4. For instance, Morgan Stanley lifted its 12-month target to $205 from $155, even while keeping an “Equal-Weight” rating, arguing Palantir’s bookings momentum justifies it.

UBS also recently upgraded PLTR to “Buy” with a $205 target, noting that the post-selloff level, roughly $140, is an “attractive entry point” given forecasts of 70% growth next year. Rosenblatt Securities initiated coverage with a “Buy” at a $150 target, calling Palantir a “market-disrupting AI software leader” with strong fundamentals, with 56% revenue growth and 82% gross margins recently.

On the bearish side, RBC Capital reiterated an “Underperform” rating with a $50 target. RBC’s bear case hinges on contract metrics: they observed that Palantir’s large deals are concentrated and saw “a decline in qualified contract value and net new annual contract value.”

So it seems like, while a few bulls remain confident, especially given Palantir’s new defense tailwinds, others warn the stock may be expensive without even stronger evidence of durable demand.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)