/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)

Chip and AI supply chain stocks have grabbed investor attention this year as demand for data center gear and networking kits ramps up with the AI boom. Not every supplier will benefit equally, but when a major platform player signals a large strategic tie-up, traders tend to listen.

That’s precisely why Lumentum (LITE) looks interesting now. Optical-networking giant surged after Nvidia (NVDA) disclosed expanded partnerships and investment commitments. Nvidia’s roughly $2 billion backing acts as a visible demand signal for Lumentum’s lasers and photonics components, which power high-speed links inside AI servers and hyperscale networks.

For investors hunting a play on AI infrastructure beyond the usual chip names, Lumentum offers a direct way to ride the optics tailwind, with near-term revenue catalysts and a powerful strategic partner in Nvidia.

About Lumentum Holdings Stock

Lumentum Holdings is a Silicon Valley designer and manufacturer of optical and photonic products enabling optical networking and laser applications worldwide. It serves telecom and cloud data center markets, the “Cloud & Networking” segment with transceivers, modulators, and switches, and provides solid-state and fiber lasers for industrial uses. In short, Lumentum builds many of the lasers and modules that carry data through fiber networks.

Recently, Lumentum secured a seven-year supply agreement for key indium-phosphide wafers, insulating it from Chinese export curbs. Management also revealed the optical-circuit-switch/co-packaged-optics backlog has swelled past $400 million. There have been no material setbacks; if anything, Lumentum is ramping up capacity and locking up components to meet demand. Overall, these updates bolster the bull case that Lumentum can keep accelerating in the AI-optics boom

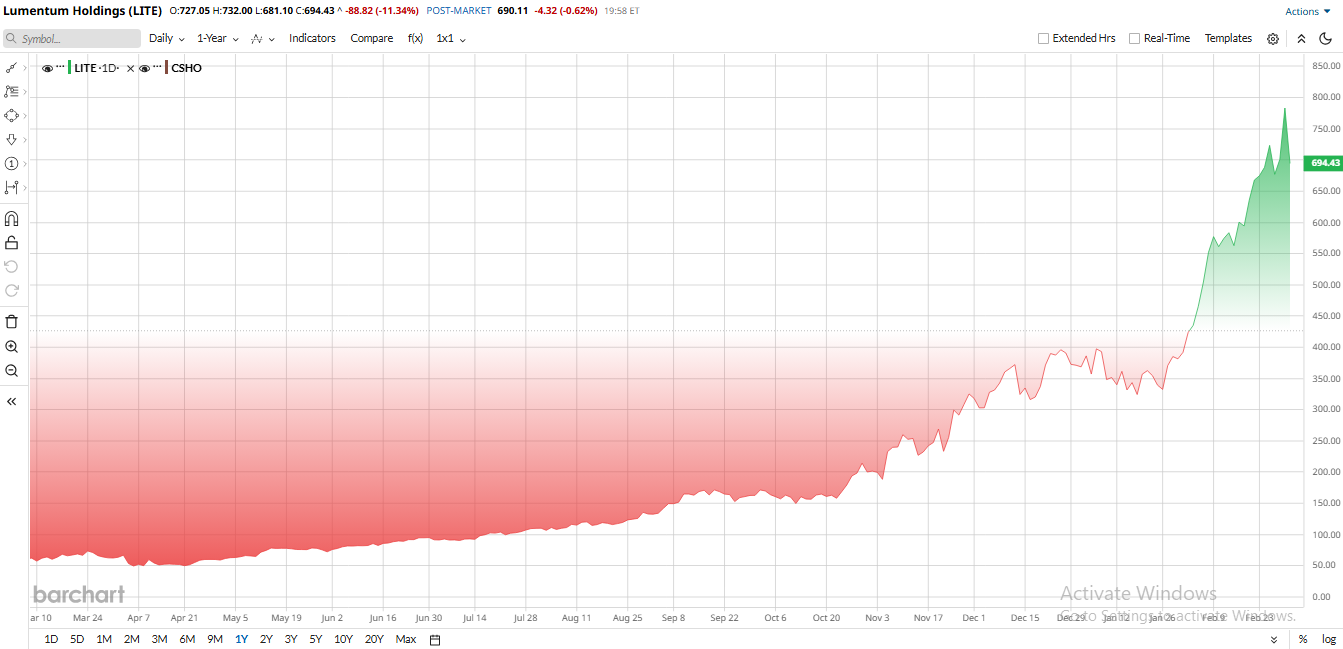

LITE stock has been on a tear lately. It roughly doubled year-to-date (YTD) and is up more than 940% over the past year, smashing the broader market. The rally follows consecutive beat-and-raise quarters and booming AI/datacenter demand. Lumentum’s backlog of optical-switch and co-packaged optics orders is now massive. Traders also cheered Nvidia’s $2 billion pact, betting Lumentum will continue feeding hyperscale growth.

However, this sharp rally brings the company's valuation to the next level. LITE's forward price-to-earnings (P/E) is in the triple digits, and EV/EBITDA is on the order of 30x, well above telecom-equipment industry norms. In other words, the stock is richly priced as far as future growth goes. Bulls argue that sky-high multiples are justified by the generational ramp in AI optics demand, but on any metric, Lumentum is at a premium versus most hardware benchmarks.

Nvidia’s $2 Billion Partnership

On March 2, Nvidia announced it will invest $2 billion in Lumentum and another $2 billion in Coherent to secure high-performance laser components for its AI data center chips. Lumentum's stock immediately jumped about 5% on the news, underscoring the sector-wide enthusiasm. The deal locks in multi-year purchase commitments and provides capital for U.S. manufacturing expansion. Investors hailed it as de-risking Lumentum’s pipeline.

Nvidia's backing validates Lumentum’s tech and frees up cash to scale capacity. Management points out Lumentum’s optical backlog already tops $400 million, so the extra funding should help ramp production even faster. In the opinion of analysts, the partnership is viewed as unambiguously positive, a powerful catalyst for sales and profits ahead.

Strong Q2 Earnings and Cash Position

Lumentum just delivered a blowout quarter, which topped analysts' estimates on both top and bottom lines. In fiscal Q2, revenue surged to $665.5 million, up 65.5% year-over-year (YoY). That wasn’t driven by one small pocket of strength either. Components revenue climbed 68% to $443.7 million, while Systems revenue jumped 60% to $221.8 million. Growth was broad-based and powerful.

Profitability flipped in a big way. Net income came in at $78.2 million, or $0.89 per share, compared to a loss of $60.9 million a year ago. On an adjusted basis, earnings soared to $1.67 per share from just $0.42 last year. Gross margin expanded to about 42.5%, up from 32.3%, helping push operating margin to 25.2%. The company also exited the quarter with a strong $1.155 billion in cash and investments.

CEO Michael Hurlston hailed it as “a standout quarter” with revenue and EPS far above targets. He added that “the vast majority of this growth is still ahead of us,” underscoring management’s view that Lumentum remains early in its AI-driven expansion.

Overall, LITE demonstrates outstanding growth metrics, with forward revenue growth at 50% and forward EPS growth at 141%. This exceptional growth underscores LITE's robust expansion and strong financial performance.

In the future, the momentum may be accelerating. For fiscal Q3, management expects revenue between $780 million and $830 million, with adjusted earnings of $2.15 to $2.35 per share, well above prior expectations. Analysts now see fiscal 2026 revenue around $2.6 billion, with earnings potentially landing in the $5 to $6 range if AI optics demand stays strong.

What Do Analysts Say About LITE Stock

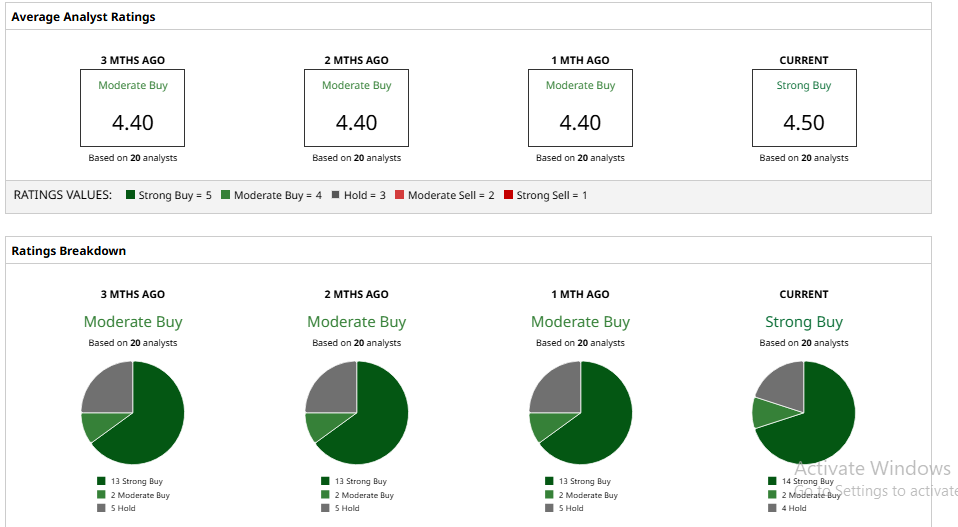

Wall Street is growing more constructive on Lumentum, even as views differ on just how much upside remains.

Morgan Stanley, which holds the stock on an “Equal-Weight” basis, has just increased its target for 12 months to $520. The firm attributes a significant increase in data center and AI-led optics spending to the primary cause, stating that the demand picture has become clear.

BofA has also increased its target to $520 and remains “Neutral.” Analysts say that AI optics are performing well, but they are weighing up the optimism on the price position coming out of the recent run.

The greatest optimist in Citi is Papa Sylla. He has increased his target to $560 and maintained a purchase call that the consensus figures continue to underestimate the magnitude and breadth of Lumentum AI development prospects.

Other firms are even more aggressive. Barclays set a $750 target, while Susquehanna and Needham each sit at $550. Overall, 20 analysts gave a consensus “Moderate Buy” rating. However, the stock is currently trading much above its mean price target of $573 and steadily climbing towards its street high target of $900.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)