For traders and hedgers alike, the Chicago Board of Trade (CBOT) wheat futures market remains one of the most closely watched benchmarks for global grain pricing. Contracts traded on the CBOT, particularly the May wheat futures, serve as price discovery engines for soft red winter wheat, influencing cash markets from Kansas City to Cairo. Yet over the past couple of years, wheat prices have seemed stuck in a sideways range, confounding some market participants and delighting others.

From 2024 into early 2026, wheat futures have broadly oscillated within a range rather than trending sharply higher or lower, between approximately $7.20 and $4.92. After a significant rally in early 2024 driven by weather-related supply concerns, futures softened as massive global harvests kept inventories ample. Even as traders saw sporadic upticks, the overall pattern has been one of consolidation rather than decisive breakouts. This sideways action reflects a backdrop of ample global supply, shifting demand, and geopolitical uncertainty rather than a clean bull or bear trend.

Part of the reason prices have lacked a strong, sustained move is the abundance of wheat in world markets. The USDA has consistently projected high global wheat production and increased ending stocks for the 2025/26 season (projected at 274.9 MMT, up 14.8 MMT year over year). These stocks have provided a comfortable buffer for buyers, reducing the urgency that would otherwise drive a strong, sustained price rally.

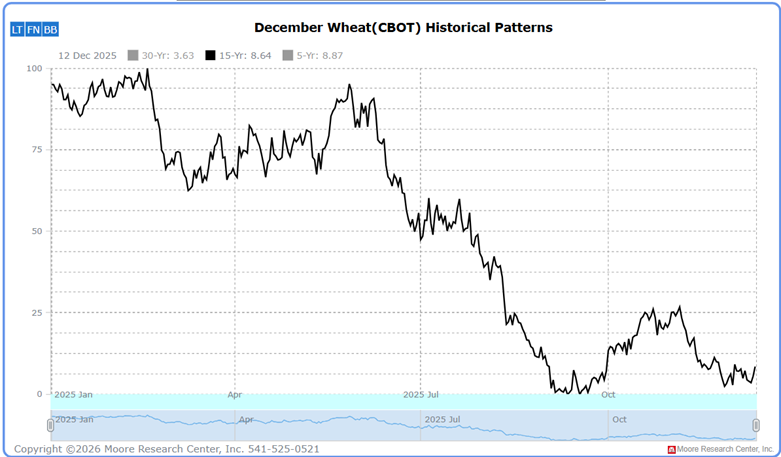

Seasonal Patterns

So the question becomes: Can wheat prices find a solid reason to rally in this environment? While supply is generally ample (cautious), weather risks in the U.S. Plains or Black Sea region frequently create "weather markets" in spring/early summer that can drive sudden rallies. While often described as a "downward slide" as harvests begin, many analysts actually point to April/May as a peak period due to "weather markets" (concerns about the new crop). However, once harvest begins in earnest (early summer), prices frequently drift lower under the pressure of new supply.

Yet seasonality isn't destiny. Counter-seasonal moves happen when underlying fundamentals change. In the 2024–26 period, weather volatility, shifting planting intentions, and geopolitical shocks have repeatedly caused technical reversals within a broader range. When weather in the U.S. Plains or Black Sea deteriorates, or when export disruptions loom, prices have temporarily broken the expected seasonal slide — suggesting that the market is responsive to fundamental developments when they carry real economic risk. Has the current Middle East war changed the seasonal pattern?

Source: Moore Research Center, Inc. (MRCI)

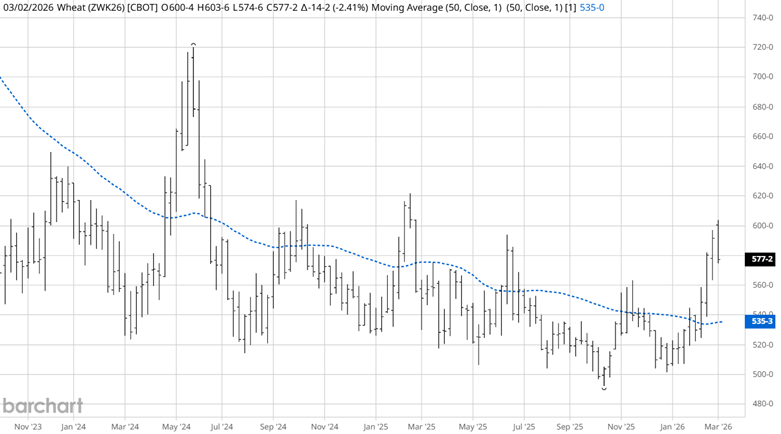

Technical Picture: Wheat Futures

Source: Barchart

Turning to the technicals of the weekly nearby chart of the CBOT wheat contract, recent price behavior has shown a series of higher highs and higher lows, a classic definition of an uptrend. In simple terms, when each successive peak and trough in a price chart is above the prior one, buyers are in control. This pattern has emerged sporadically even amid sideways conditions, suggesting the market may be bottoming and ready for a broader advance. While futures aren't blasting off to multi-year highs, the structure of upward swings suggests growing conviction among trend-following managed money traders.

Technical uptrends are important because they represent price behavior, not just analyst forecasts. They often reflect shifting psychology among traders — from pessimism about oversupply to cautious optimism about tightening demand or supply risks. Such trends can self-reinforce as momentum players add to positions, thereby strengthening the rally.

Beyond Chicago: Other Markets to Trade Wheat

While CBOT futures are the most direct vehicle for wheat exposure, several related markets provide alternative or complementary trading avenues:

- Futures: Standard-size contracts (ZW), the mini contract (XW), or the new micro contract (WT).

- Wheat ETFs: WEAT (fund that tracks CBOT wheat futures) enables portfolio investors to express long or short views without futures margins.

- Options on wheat futures offer a way to hedge or express directional bias with defined risk.

- Spread trades between wheat and other grains, such as corn or soybeans, can capture relative value shifts when supply/demand dynamics differ (intermarket spreads). Traders can also trade different calendar months of wheat futures, referred to as intramarket spreads.

In Closing: Could Geopolitics Spark a Rally?

Geopolitical events often play out in commodity markets because they sharpen risk perception, disrupt logistics, or inflate input costs. The 2026 conflict involving the U.S., Israel, and Iran — and particularly disruptions around the Strait of Hormuz — has roiled oil and gas markets, driving energy price volatility and raising fears of broader trade bottlenecks.

Although wheat isn't shipped in oil tankers, maritime chokepoints can disrupt fertilizer shipments, raise freight costs, and erode global trade confidence. Plus, higher energy costs translate into higher production and transport expenses for farmers, which can elevate the floor under crop prices. Previous research has shown that energy and grain markets often move in tandem during periods of systemic stress.

While wheat prices have been weighed down by abundant supply and seasonal patterns, the combination of technical strength, latent supply risks, and geopolitical instability opens the door to a surprising and sustained rally — one that breaks the sideways narrative and gives bulls something to cheer.

On the date of publication, Don Dawson did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)