/Broadcom%20Inc%20logo%20on%20building-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

Broadcom (AVGO) will report its fiscal first-quarter 2026 financial results on March 4, 2026, after the market close. Ahead of the announcement, two key factors support a constructive view on the stock, including the sustained momentum in the artificial intelligence (AI) semiconductor business and continued strength in infrastructure software, particularly VMware Cloud Foundation (VCF).

Furthermore, Broadcom’s risk-reward profile looks compelling following the recent pullback. Let’s take a closer look.

AI and VCF Demand to Lift AVGO Stock

The solid momentum in its AI-focused semiconductor business and its infrastructure software segment strengthens its growth outlook for fiscal 2026 and beyond, supporting its share price.

Demand for Broadcom’s AI semiconductor solutions remains strong. Hyperscale and enterprise customers continue investing in custom accelerators (XPUs) and high-performance networking components for large-scale data centers. This demand environment is expected to meaningfully support first-quarter results and accelerate revenue growth as the year progresses.

Notably, the AI semiconductor revenue was $6.5 billion in the fourth quarter, up 74% from the prior year. The company’s custom accelerator business more than doubled year-over-year (YoY) as XPU adoption expanded.

Order activity remained solid, strengthening the outlook for future growth. Broadcom secured a $10 billion order in the third quarter of fiscal 2025 to supply TPU Ironwood racks to Anthropic, followed by an additional $11 billion order from the same customer in the fourth quarter for delivery in late 2026. The company also added a fifth XPU customer through a $1 billion order scheduled for delivery in late 2026.

AI networking demand has been even stronger, as customers build out data center infrastructure in advance of accelerator deployments. Broadcom’s backlog for AI switches exceeds $10 billion, driven by record bookings for its Tomahawk 6 switch. The company has also secured record orders for digital signal processors, optical components such as lasers, and PCI Express switches destined for AI data centers.

Including XPUs and related components, Broadcom’s total AI order backlog now exceeds $73 billion, nearly half of its consolidated backlog of $162 billion. Management expects to deliver this AI backlog over the next 18 months and projects AI revenue to double YoY to $8.2 billion in the first quarter of fiscal 2026.

Beyond AI semiconductors, Broadcom’s infrastructure software segment is another growth driver. Adoption of VCF continues to expand, supporting recurring revenue growth and deeper enterprise integration as organizations modernize IT environments and pursue hybrid and private cloud strategies.

Overall, AI is expected to remain the primary growth engine. While infrastructure software could see seasonal renewals in Q1, the segment is expected to grow at a low double-digit rate in fiscal 2026.

For the first quarter of fiscal 2026, consolidated revenue is projected at approximately $19.1 billion, up 28% YoY. Further, analysts expect Broadcom to deliver earnings of $1.67 per share, up 19.4% YoY.

Broadcom’s Valuation Looks Attractive Ahead of Q1

While Broadcom is set to deliver double-digit revenue and earnings growth, the recent share price consolidation has reduced valuation pressures following prior highs. The pullback has brought AVGO stock to more moderate valuation levels heading into earnings, improving the risk-reward profile.

Broadcom is trading at a forward price-to-earnings multiple of 37.4. This valuation multiple looks compelling in light of projected earnings growth of 54.7% in fiscal 2026, followed by a 40.4% jump in 2027. Ongoing momentum in its semiconductor and infrastructure software and a reasonable valuation support AVGO’s investment case.

From a technical perspective, the stock’s 14-period Relative Strength Index (RSI) on the weekly chart stands at 47.8, comfortably below the 70 threshold typically associated with overbought conditions. This suggests the shares have room for additional upside in the near term.

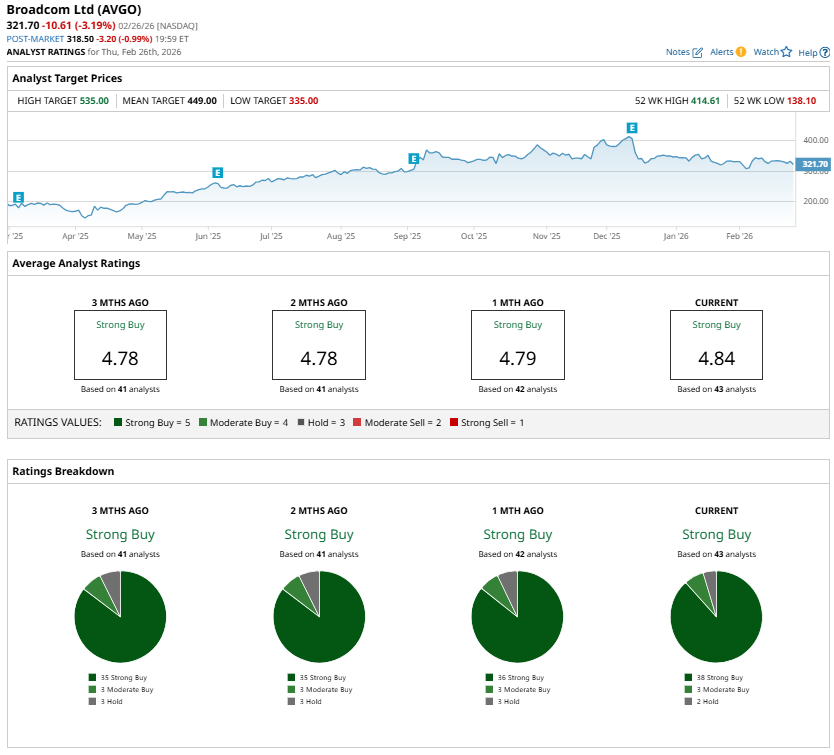

Wall Street analysts remain bullish about AVGO stock ahead of earnings and maintain a “Strong Buy” consensus rating. The average price target of $449 suggests about 40% upside from its Feb. 26 closing price of $321.70.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/Friends%20choosing%20a%20movie%20on%20a%20streaming%20service%20by%20Stock-Asso%20via%20Shutterstock.jpg)