/Honeywell%20International%20Inc%20operations%20facility%20by-JHVEPhoto%20via%20iStock.jpg)

Charlotte, North Carolina-based Honeywell International Inc. (HON) is an industrial technology leader that provides building automation, industrial automation, and process automation & technology services. It is valued at a market cap of $154 billion.

Companies valued at $10 billion or more are typically classified as “large-cap stocks,” and HON fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the conglomerates industry. Known for its strong engineering capabilities and recurring revenue from long-term service contracts, HON is well positioned as a leader in automation, digitalization, and energy efficiency solutions.

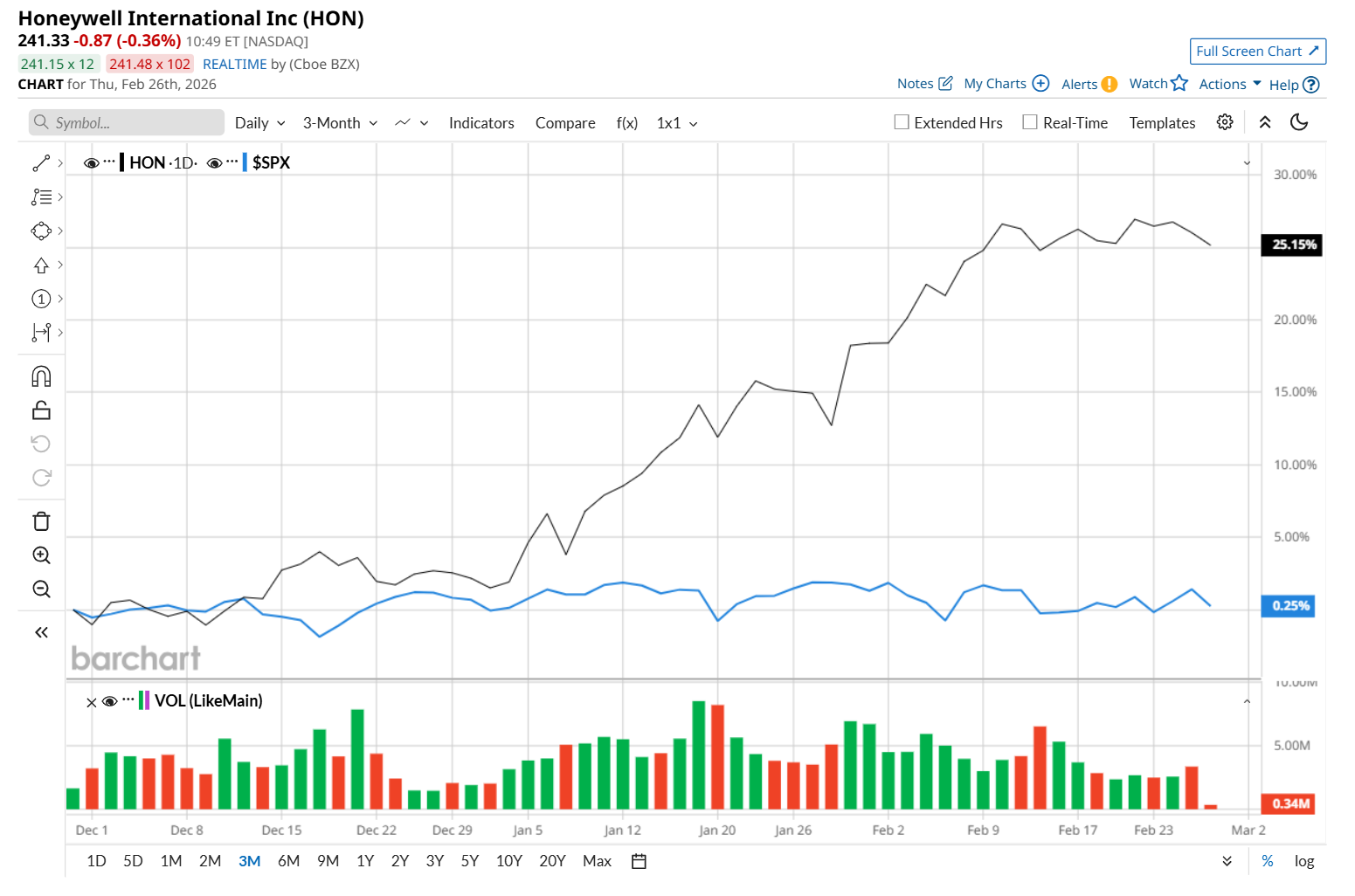

This industrial giant is currently trading 2.4% below its 52-week high of $246, reached on Feb. 23. Shares of HON have rallied 27% over the past three months, considerably outperforming the S&P 500 Index’s ($SPX) 1.6% rise during the same time frame.

Moreover, on a YTD basis, shares of HON are up 23.7%, compared to SPX’s 1.1% gain. In the longer term, HON has surged 21% over the past 52 weeks, outpacing SPX’s 16.2% uptick over the same time frame.

To confirm its bullish trend, HON has been trading above its 200-day moving average since early January and has remained above its 50-day moving average since mid-December, with slight fluctuations.

On Jan. 29, shares of HON surged 4.9% after delivering mixed Q4 results. The company's overall revenue increased 6.4% year-over-year to $9.8 billion, but missed analyst estimates by 1.5%. However, HON’s strong organic revenue growth of 11% might have impressed investors. Moreover, its adjusted EPS of $2.59 grew 17% from the same period last year and came in 2.1% ahead of Wall Street estimates, further bolstering confidence.

HON has outpaced its rival, 3M Company (MMM), which gained 11.9% over the past 52 weeks and 3.1% on a YTD basis.

Given HON’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 23 analysts covering it, and the mean price target of $249.27 suggests a 3% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)