/NVIDIA%20Corp%20logo%20on%20phone%20and%20AI%20chip-by%20Below%20the%20Sky%20via%20Shutterstock.jpg)

Nvidia (NVDA) turned plenty of heads last year when the company and OpenAI announced the framework of a multiyear deal worth potentially $100 billion. The deal would have seen OpenAI build up to 10 gigawatts of AI data centers using Nvidia technology, including its vaunted graphics processing units (GPUs).

The deal, when announced, drew attention not only for its scope but also because it was seen as an example of Nvidia bolstering its own sales—essentially, providing OpenAI the funding it would need to turn around to buy Nvidia GPUs.

But that deal is off the table. Instead, Nvidia is making a $30 billion equity investment in OpenAI as part of the company’s latest funding round, which values the maker of ChatGPT at about $830 billion.

OpenAI is still expected to use the funds to buy Nvidia’s chips. But should investors view Nvidia differently now, considering its much smaller deal and the shift from an infrastructure tie-in to a straight equity stake?

About Nvidia Stock

Nvidia is the world’s leading maker of high-performance semiconductor chips that are used for high-level processing of complex computing tasks, including machine learning and artificial intelligence. Nvidia, which is based in Santa Clara, California, is the largest publicly traded company in the world by market capitalization, currently at $4.6 trillion.

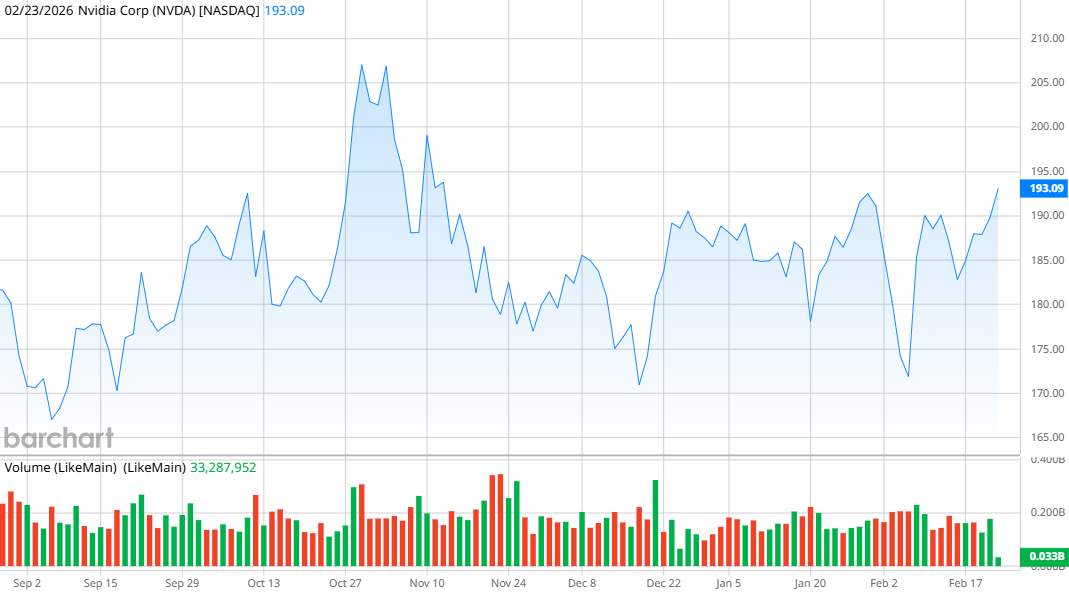

Shares are up 44% in the last year but have shown some volatility in recent months as investors have largely pulled back on AI stocks. However, a series of announcements from Nvidia’s major customers that pledge several hundred billion in new AI investments this year has restored investor confidence ahead of Nvidia’s upcoming earnings on Feb. 25, pushing the stock 10% higher over the last three weeks.

So far in 2026, Nvidia is up 1.4%, beating the S&P 500’s ($SPX) 0.1% gain in the same period.

Despite its solid performance, Nvidia stock is surprisingly affordable. Its forward price-to-earnings ratio of 24.9 is better than either of its primary competitors—Advanced Micro Devices (AMD) is at 30, and Intel (INTC) is an eye-watering 91.8.

Nvidia Looks Solid Heading Into Earnings

Nvidia is scheduled to report its earnings for its fiscal fourth quarter of 2026 after the closing bell on Feb. 25. If they’re anything like the fiscal Q3 earnings, investors should be pretty happy.

Q3 earnings (ending Oct. 26, 2025) showed revenue of $57 billion, up 62% from a year ago. Net income was $31.7 billion, up 59% from last year, and earnings came in at $1.30 per share, beating analyst expectations of $1.18.

Looking forward to the fourth quarter, analysts are expecting bottom-line growth to accelerate to 70% from a year ago, with a consensus earnings estimate of $1.45 per share. Nvidia reported that its data center revenue was $51.2 billion, up 66% from last year. And that growth story is bolstered by announcements from Alphabet (GOOG) (GOOGL), Amazon (AMZN), Meta Platforms (META), and Microsoft (MSFT) that they plan to spend $625 billion this year alone on data centers and AI infrastructure. While there’s no indication exactly how much money will come flowing into Nvidia’s coffers, you can assume that it will get a lot—especially as its Blackwell GPUs continue to be in high demand and the next-generation Vera Rubin processors are now in full production.

What Do Analysts Expect for NVDA Stock?

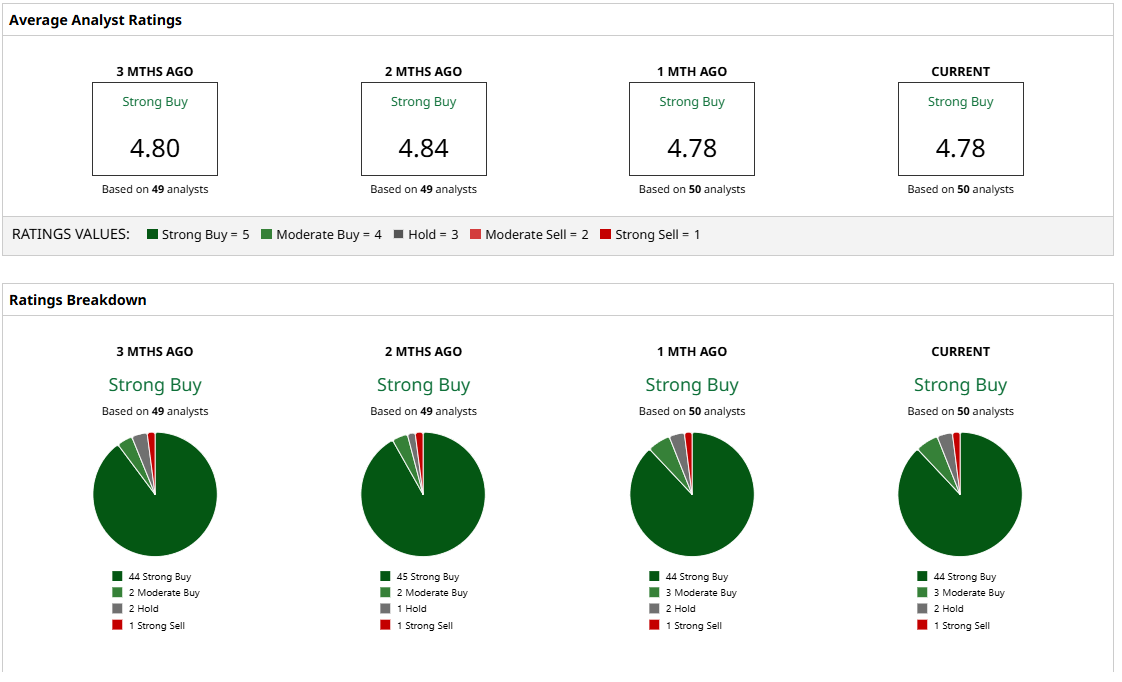

Nvidia is massively popular with analysts, who collectively have a strong sentiment that the stock will be moving higher. Of 50 analysts who cover the stock, 47 have “Buy” ratings and two recommend holding. Only one analyst has a “Sell” rating. It’s unusual to see a stock with such powerfully unified sentiment.

The mean price target of $255.55 indicates potentially a 33% growth window, with the most bullish target of $352 hinting toward an 84% gain. The lone dissenting target of $140 warns that NVDA stock could decline by 27%—but personally, I don’t see that happening at all.

Nvidia seems poised for a monster earnings report. I don’t see the shift in its commitment to OpenAI being a roadblock at all—Nvidia has plenty of business coming its way, including previously announced deals with Anthropic, Intel, Oracle (ORCL), and Palantir Technologies (PLTR).

Nvidia is a strong buy right now, and I’m expecting it to hit new highs in the coming weeks.

On the date of publication, Patrick Sanders had a position in: NVDA , PLTR . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)