/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

Artificial intelligence (AI) has dominated headlines in recent years, with tech giants and startups alike racing to embed AI into their products and services. And investors have eagerly chased the next big AI winner. Amid all the noise, Dell Technologies (DELL) is a name that often flies under the radar in AI infrastructure conversations. Yet, the company is seeing a powerful surge in demand for its AI-optimized servers as enterprises ramp up spending to support generative AI workloads and data center upgrades.

While Dell’s stock has faced some pressure in 2026, a major catalyst is just days away. The company is set to report its fiscal fourth-quarter 2026 results on Feb. 26, and one analyst is growing increasingly optimistic ahead of the release. Evercore ISI recently upgraded Dell to “Tactical Outperform,” signaling confidence going into earnings. Although the investment firm trimmed its price target to $160 from $180, it expects Dell to beat consensus estimates of $31.4 billion in revenue and $3.52 in EPS, driven by solid near-term demand across traditional hardware such as PCs and servers, along with continued strength in AI compute.

The firm highlighted that rising memory prices, which might sound like a concern at first glance, are creating a short-term tailwind. In fact, fears of further memory inflation are pushing customers to accelerate purchases of PCs and traditional servers, creating a near-term demand boost. According to Evercore, this pull-forward effect has strengthened Dell’s recent order environment. So, given this optimism, here’s a closer look at DELL stock.

About Dell Stock

Dell Technologies provides a wide range of technology solutions designed to help organizations modernize their IT environments and adapt to an increasingly digital economy. Its portfolio spans infrastructure, devices, and services, positioning the company across multiple layers of the AI ecosystem. The Infrastructure Solutions Group (ISG) plays a particularly important role, supplying the servers, storage, and networking systems that underpin AI and data-intensive workloads.

As enterprises expand their computing capacity to support generative AI and advanced analytics, this segment has seen solid demand trends. At the same time, Dell’s Client Solutions Group (CSG) offers PCs, laptops, workstations, and related peripherals, maintaining the company’s presence in both enterprise and consumer markets.

With a market capitalization of roughly $81 billion, Dell has encountered some turbulence in early 2026. The stock has come under pressure amid broader hardware sector softness, a few analyst downgrades, intensifying competition in the AI server market, and slower-than-expected AI adoption in personal computers. As a result, Dell shares have gained just 1.34% over the past year and are down 5.33% so far in 2026.

In contrast, the broader S&P 500 Index ($SPX) surged 13.48% in 2025 and has dipped marginally this year, highlighting Dell’s relative underperformance against the wider market. Nevertheless, momentum has started to shift. Dell is up roughly 1.43% over the past five days, well ahead of the broader market’s 0.18% loss over the same period, as Evercore’s bullish call appears to have sparked more constructive investor positioning ahead of earnings.

Valuation is another area where Dell stands out. The stock currently trades at about 11.31 times forward earnings and just 0.72 times sales, a notable discount to the sector medians of 22.65x and 3.13x, respectively. In a market where many AI-related stocks carry elevated multiples, Dell’s comparatively restrained pricing may draw attention from investors seeking AI exposure at a more measured valuation.

A Closer Look Inside Dell’s Q3 Performance

Dell’s fiscal third-quarter 2026 results, announced on Nov. 25, underscored the centrality of AI to its growth story. The company posted record revenue of $27 billion, up 11% year-over-year (YOY) and roughly in line with Wall Street expectations. While performance was solid across the board, the real standout was its AI-driven infrastructure business.

The Infrastructure Solutions Group (ISG), home to Dell’s data center and AI server business, stood out. Revenue in the segment climbed 24% YOY to $14.1 billion. Even more striking, servers and networking revenue surged 37% to $10.1 billion, reflecting strong demand for AI servers and high-performance compute systems.

The picture was more mixed on the client side. The Client Solutions Group (CSG), which includes laptops and PCs, generated $12.5 billion in revenue, up 3% from a year ago. However, within that segment, laptop and PC revenue declined 7% annually, reflecting continued softness in parts of the traditional PC market. Nevertheless, executives pointed to AI as the key growth engine.

While reflecting on the quarterly performance, Jeff Clarke, vice chairman and chief operating officer of Dell, said AI momentum accelerated in the second half of the year, driving record AI server orders of $12.3 billion and lifting year-to-date (YTD) AI orders to $30 billion. Clarke noted that Dell’s five-quarter pipeline now stands at multiples of its $18.4 billion backlog, supported by demand from neocloud, sovereign, and enterprise customers.

On the bottom line, Dell reported record adjusted EPS of $2.59, up 17% YOY and comfortably ahead of the $2.48 consensus estimate. The company also returned $1.6 billion to shareholders through dividends and share repurchases during the quarter. Looking ahead to the fiscal fourth quarter, with results due Feb. 26, Dell expects revenue of about $31.5 billion, up 32% YOY, and non-GAAP EPS of $3.50 at the midpoint, up 31%.

For the full fiscal year 2026, the company projects AI server shipments of roughly $25 billion, a jump of more than 150%, and total revenue between $111.2 billion and $112.2 billion, representing 17% growth at the midpoint of $111.7 billion. If those targets are met, it would mark another year of AI remaining central to Dell’s growth story.

How Are Analysts Viewing Dell Stock?

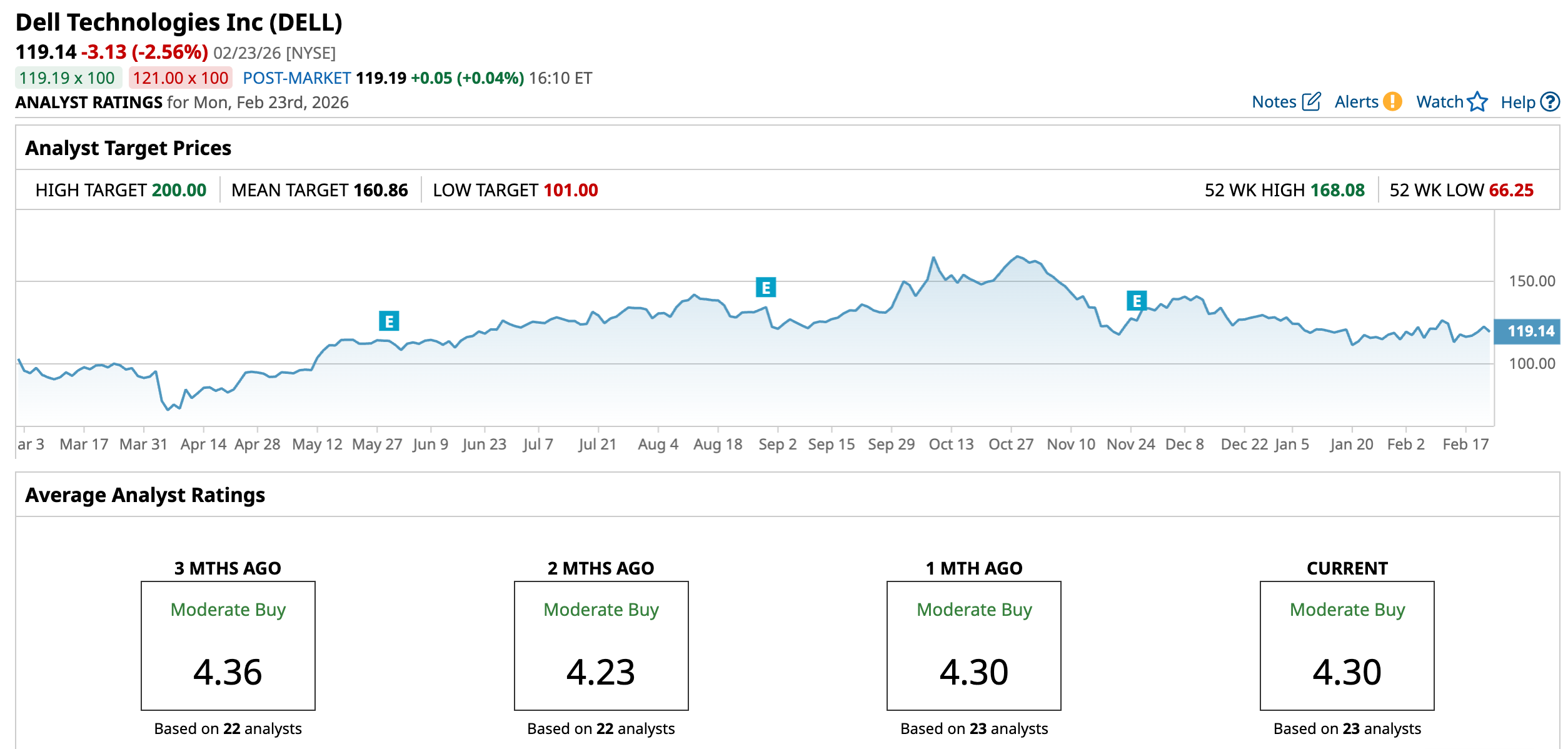

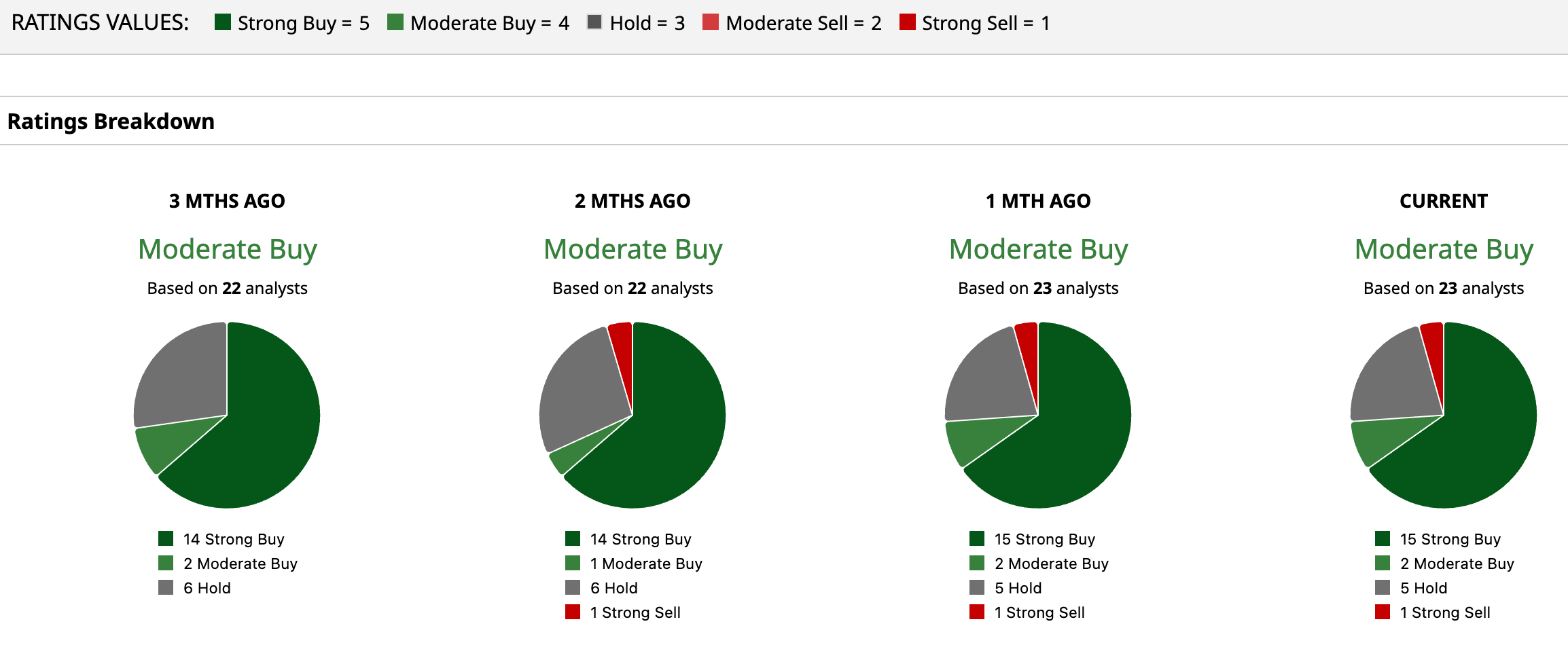

As Dell gears up to report its fourth-quarter results, Wall Street’s tone remains broadly constructive. The stock currently carries a consensus “Moderate Buy” rating, reflecting a generally upbeat outlook from analysts. Of the 23 analysts covering the name, 15 rate it a “Strong Buy,” two call it a “Moderate Buy,” five recommend “Hold,” and just one has a “Strong Sell” rating.

The average price target of $160.86 suggests roughly 35% upside from current levels. Meanwhile, the highest target on the Street stands at $200, implying potential gains of up to 68% if bullish expectations materialize.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)