/Dominos%20Pizza%20Inc%20storefront%20by-KathyDewar%20via%20iStock.jpg)

Domino's Pizza (DPZ) still looks cheap here, as I wrote two weeks ago. As a result, shorting out-of-the-money (OTM) DPZ puts in one-month expiry periods works well here, given Domino's Pizza's cheap valuation.

Also, buying in-the-money (ITM) calls 6 months or longer away, financed with OTM put income, is another great play for less risk-averse investors. I discussed both plays in a Feb. 17 Barchart article, and this article will look into their performance.

DPZ is at $397.00 today, higher than where it was almost a month ago when I wrote the Feb. 17 article ahead of earnings ($374.48).

However, when earnings were released pre-market open on Feb. 23, DPZ shot up to $400.36 and closed the next day at a $414.20 peak close. So, since then, DPZ has retraced this higher move. It might make sense to do another short-put play.

But first, what is DPZ stock worth, and how did our last recommendation work out?

DPZ Stock Still Looks Cheap

I wrote in a Feb. 23 Barchart article, after the Domino's Pizza earnings release and its huge dividend hike, that DPZ was worth between $425 and $475 per share ("Domino's Pizza Hikes Its Dividend By 14.3% After Free Cash Flow Rises 29% - Value Buyers Love DPZ Stock.")

The $475 price target was based on its average dividend yield in 2025 (1.67%):

$7.96 dividend per share (DPS) / 0.0167 = $476.67 (i.e., 20% upside)

The $425 price target was based on its free cash flow margin (13.6% in 2025, according to Stock Analysis) and analysts' revenue forecasts: $5.39 billion over the next 12 months (NTM):

$5.39b x 0.136 = $733 million NTM FCF

So, using a 5.0% FCF yield, its value is $14.66 billion (i.e., $733m/0.05), which is $1.31 billion more than its market cap today of $13.35 billion, i.e., +10% higher:

$397 x 1.10 = $436.70 price target (PT)

So, the updated PT range is now between $437 and $477 per share, i.e, +10% to 20% higher.

Analysts also have similar upside. For example, Yahoo! Finance reports that the average of 34 analysts' PTs is $478.58, and AnaChart's survey of 24 analysts' PTs is $463.60.

Shorting OTM DPZ Puts Works

On Feb. 17, I discussed shorting the March 20 DPZ put option at the $350.00 put option strike price, which was 6% lower than the DPZ stock price then ($374.48). The premium received then was $7.70, or a 2.20% yield ($7.70/$2.20) for 31 days to expiry (DTE).

Today, the price is down to $1.23, so it's been a very successful short-put play. Investors should either let it expire worthless, or roll it over (i.e., “Buy to Close”) and do a new short-put play.

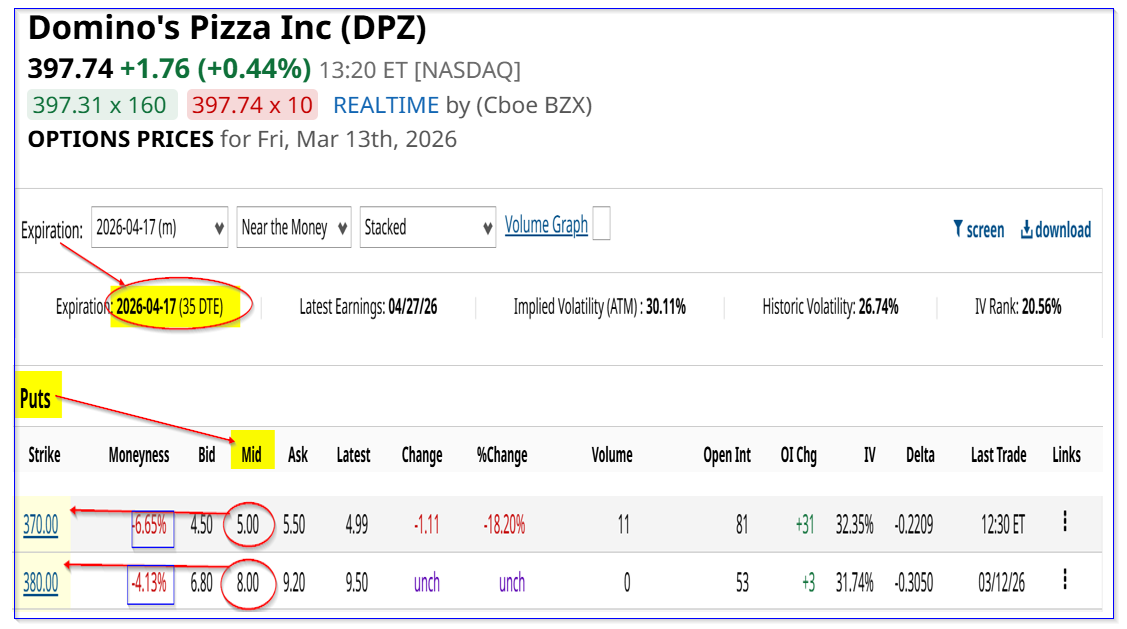

For example, the April 17, 2026, put option at the $370.00 strike price is $5.00, and the $380.00 premium is $8.00, i.e., distances between 4% and 6% away (i.e., below) today's price:

That means an investor who enters an order to “Sell to Open” these put contracts will make a yield of between 1.43% (i.e., $5.00/$350.00) and 2.10% (i.e., $8.00/$380.00). That works out to an average yield of 1.765% (i.e., for 2 put contracts shorted this way), at an average out-of-the-money (OTM) distance of 5.39% lower.

Similarly, buying in-the-money (ITM) calls in longer-dated periods has worked out.

Buying Long-Dated ITM Calls

On Feb. 17, I recommended buying in-the-money calls at $350.00 expiring Sept. 18, and using short-put premiums to help pay for that investment.

At the time, the call price was $51.10. Today, that premium has risen to $68.40, a 33.9% gain over the last month. That significantly outperformed the 6% gain in DPZ stock over the same period (i.e., $397/$374.48-1).

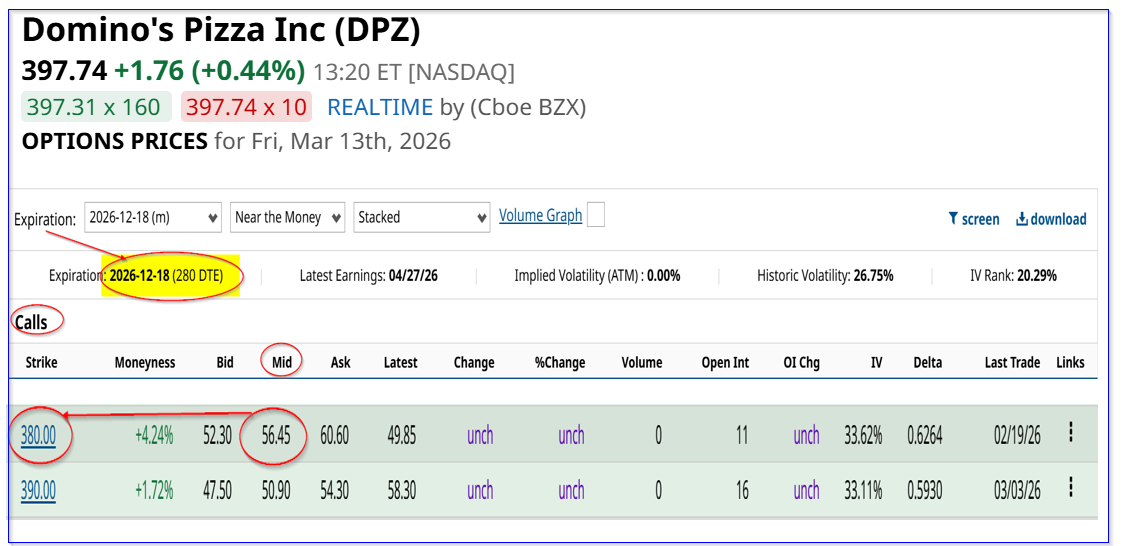

So, doing this again might make sense for less risk-averse investors. For example, the 12/18/26 expiry period (280 days to expiry or 9 months away) call option for the $380 call has a midpoint premium of $56.45.

The idea here is that if an investor can continue to collect between $5.00 and $8.00 each month for 9 months (i.e., $6.50 x 9 = $58.50), the cost of the call option can more or less be covered:

$58.50 cumulative put income for 9 months vs. $56.45 call option cost

Obviously, there is no guarantee that an investor can continue to collect these put premiums. But, the idea is that much of the call option cost for this in-the-money call purchase (which has some downside protection) can be paid for by cumulative short-put play income.

As a result, this is a leveraged way to play the upside in DPZ stock.

The bottom line is DPZ stock looks very cheap here, and these two plays are worth considering by value investors.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)